The Pound to Indian Rupee is showing technical signs of strength as the new trading week begins.

On the daily chart, the pair has broken above a key trendline formed by joining the tops of the December 2016 and January 2017 highs.

The break, which appears conclusive, represents a key turning point for the pair and suggests the balance of probabilities favours a continuation higher.

A break above the post-break highs at 84.49 would probably lead to an extension up to a target at 85.00.

The pair may even extend higher according to one method for forecasting the move after a trendline break which takes the move prior to the break as a guide (a) and extrapolates the same distance higher from the break (b); this method sets a target probably even slightly above 85.00.

Data for the Rupee

The main data releases are bunched together on Friday, July 21, and include Bank Loan Growth, FX Reserves and Deposit Growth – all released at 12.30 BST.

The overall outlook for INR from a general fundamental perspective remains positive, according to analysts at Morgan Stanley.

They suggest there are several good reasons for buying the currency.

The fall in inflation means investors are not cheated out of profits by inflation.

“India's CPI inflation surprising to the downside keeps the currency attractive from a real rate perspective,” said Morgan Stanley.

The reform-minded government is attractive to outside investors.

“Reform momentum remains strong with GST tax reforms kicking in this week without disruptions. We think FDI investment and carry demand continue to support INR,” added the investment bank.

HSBC's Paul Mackel, however, is less bullish, arguing portfolio flows - which had peaked - are now rolling over.

He also suggests the Reserve Bank of India (RBI) is at the opposite end of the monetary policy cycle to western central banks and RBI could start cutting interets rates at a time when the 'G3' are preparing to raise them.

Writing at the end of June, Mackel said the Indian June inflation print could be important in deciding whether the RBI cut interets rates or not, and the print ended up showing a slow-down to a new annual low of 1.54%, increasing the probabilities of a rate cut at the next RBI policy meeting.

Mackel's more bearish fundamental reading of the currency fits better with the bearish technicals.

Data for the Pound

The standout release for Sterling in the week ahead is June Inflation data which is out at 9.30 BST on Tuesday July 18.

The release is important because it impacts on the decision making of the Bank of England (BOE), which in turn is a major driver of the Pound.

Inflation has risen steeply after the Pound weakened following the referendum, which had the consequence of pushing up the prices of imports.

Inflation in May stood at 2.9% year-on-year (yoy: ie compared to May 2016), and 0.3% month-on-month (mom).

The consensus amongst analysts is that it will remain at 2.9% in June yoy but rise at a lesser 0.2% mom.

However, Canadian Investment Bank TD Securities think the market is being too dovish and forecast a higher 3.0% rise in inflation.

TD expect Core inflation to come out at 2.6% which is the same as the market.

A rise in the cost of utilities is likely to be the driving force behind higher broad inflation and stable core.

“Inflation is likely to have continued its march upward in June, in part due to utility price increases. Core inflation, meanwhile, is likely to have remained stable.”

Nor do TD see this as the “peak for inflation” as core could rise 1 or 2 basis points and headline could rise to the “min-3% range”, which would, “head up the debate about a (single) rate hike later this year.

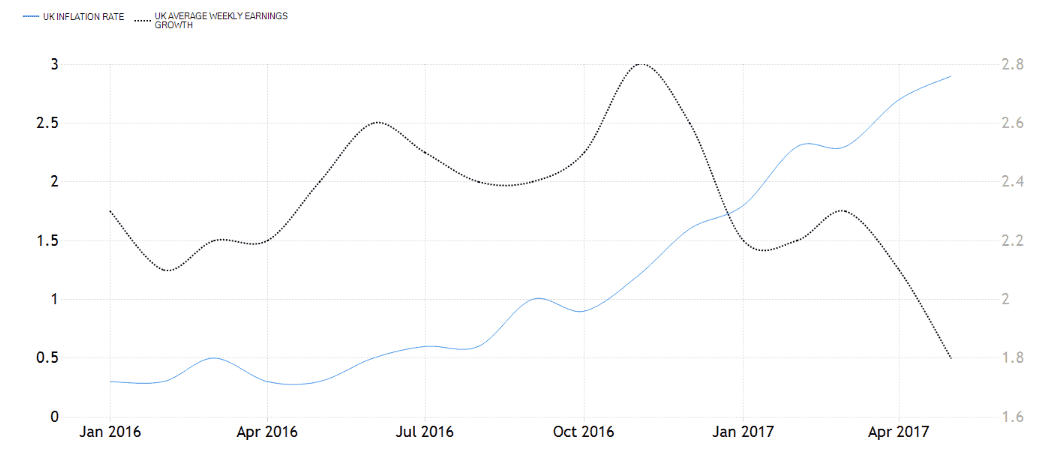

Incidentally the divergence between slowing average earnings in the UK and rising inflation is probably the root cause of the slowdown in the high street or “consumption” as economists like to call it.

The drag on growth from people spending less money is likely to keep the hawks at the BOE in check and limit any possibility of a rate hike.

We know Carney for one won’t change his view until the “trade-off” facing the MPC “continues to lessen” by which he means the trade-off between slowing growth and rising inflation.

Which brings us on to the other major release of the week for Sterling – Retail Sales on Thursday, July 20 at 9.30.

The market is currently being very optimistic about the gains expected in June.

They see headline Sales rising 2.6% yoy – which is a big jump from the previous 0.9% print; and Core increasing 2.4% from May’s very much lower 0.6% rise.

The market also expects a monthly rise of 0.4% for headline and 0.5% for core from -1.2% and -1.6% respectively in May.

This turnaround appears hugely optimistic from both our and TD Securities perspective, and seems to have little logic backing it up.

TD are of the opinion that Sales will not rise by anything (0.0%) mom in June rather than the 0.4% suggested by the market – we agree.

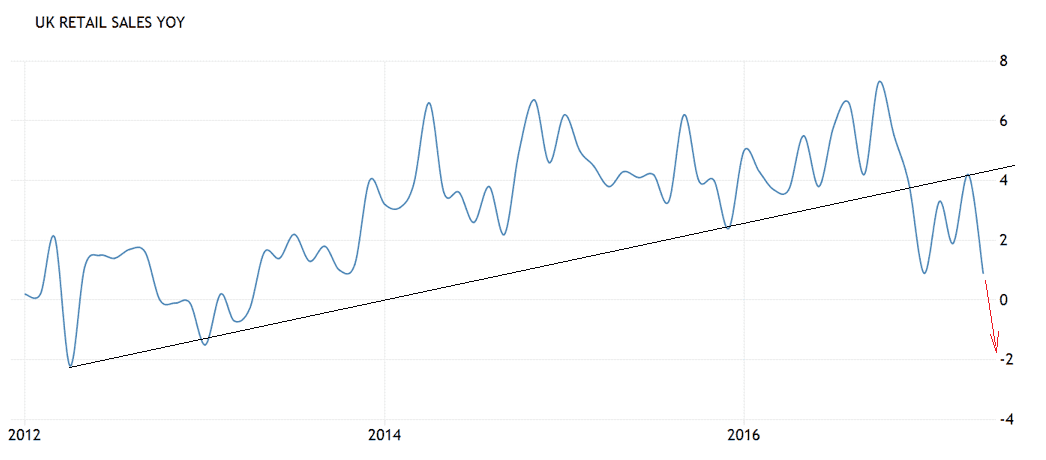

The picture below showing historical Retail Sales data shows a breakdown in the prior up-trend which gives the outlook a definite bearish hue.

The look and feel of the chart betokens a more negative print next Thursday than a more positive, which would also make more sense given the fall in real earnings.

BK Asset Management’s Kathy Lien, however, thinks there is a chance of a better-than-expected print:

“The smaller decline in shop pricesand the uptick in BRC retail sales monitor points to stronger numbers that should help rather than hurt the GBP/USD rally,”

Whilst this fits with the bullish technical outlook we, nevertheless, retain a negative bias.