India’s positive economic outlook will probably support the Indian Rupee (INR) over time, but there is a notable risk of a near-term pullback.

These are the findings of the latest research into the Rupee by Nordea Bank’s Amy Yuan Zhuang.

“The INR rally is overdone so a correction is expected. But it will likely continue outperforming peers,” said Zhuang in a note to clients.

India’s Rupee has fallen back against the Pound through the course of April, but this is more a function of short-term Sterling strength within a more protracted period of weakness. The pair had fallen to multi-year low at 79.50 back in early April to recover to current levels around 82.50.

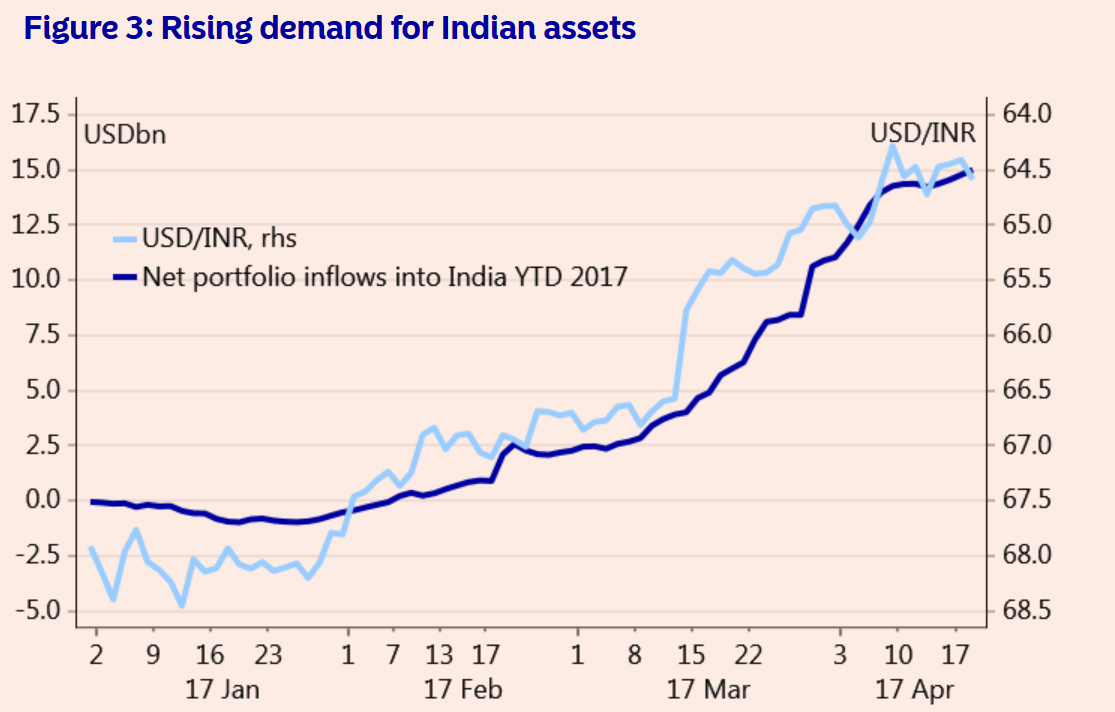

But against the US Dollar the Rupee has enjoyed some good notable strength having pushed USD/INR from 69.00 seen back in December down to the current levels around 64.00.

The currency continues to benefit from a steady rise in foreign investment inflows due to the government’s economic reforms, which have made the country more attractive to outside investors.

“Year-to-date net foreign capital inflows into India amounted to USD 15bn by mid-April. In the near term, the INR rally seems overdone and we expect a moderate correction,” says Zhuang in a note dated April 26.

But its longer-term potential is intact argues Zhuang:

“Market-friendly reforms to boost domestic demand combined with Modi’s strengthened political position will keep attracting foreign companies and investors seeking high growth and political stability.

Charts confirm a high correlation between the rising INR and increasing capital investment.

Reserve Bank to Keep Rates High

The Rupee is likely to be further supported by a Reserve Bank of India that will be likely to raise interest rates as they combat the threat of inflation.

Inflation inched up to 3.5% in February and the Reserve Bank of India remains on guard for an inflation bump due to the liquidity glut caused by the demonetisation programme, which forced Indians to bank high denomination notes or risk being left with redundant notes after they were withdrawn.

It is feared this combined with other factors such as surges in investment, growth and food price inflation caused by the weather is likely to keep the central bank from cutting rates.

Higher interest rates are positive for a currency as it only gives added reason for international investors to send capital into the country so the Rupee would be expected to benefit.

Growth Surprisingly Robust

Growth has been surprisingly robust despite the negative impact demonitisation was expected to have on the economy, but Zhuang says the follow-through from draining so much liquidity from the economy could impact in Q1’s figures, which are still to come out.

“It is possible that the Q4 GDP data have understated the adverse impact of the demonetisation. Activities in cash-based informal sectors, such as retail trade, are likely not fully captured by national account data. Hence, there is good reason to be cautious on Q1 growth, especially given continued falling consumer and business confidence. We have kept our growth forecast unchanged at 7.1% and 7.5% for this year and the next,” says Zhuang.

Rupee to Gain from Banking Reform

Amongst the plethora of market positive reforms embarked on by the Modi government is the intention to tackle high number of non-performing loans by creating ‘bad banks’ who would purchase the loans from the commercial bank’s thus removing them from their balance sheets.

“Since the high NPL ratio is a key reason for India’s sluggish credit and investment growth, we are encouraged by any meaningful development in resolving the problem,” says Zhuang.

Given the country is already attracting much foreign capital anyway, reforms of the country’s banks, some of whom suffer from balance sheets with 20% of loans non-performing, is likely to open the floodgates to even more capital inflows, further shoring up Rupee strength.