Financial markets have been sent into a tailspin by the unexpected news that Prime Minister May has called a snap June 8 general election to provide her with a stronger mandate for Brexit negotiations.

In response to the news, the Pound has risen against all its counterparts, including the Indian Rupee.

GBP/INR has strengthened a whole Rupee in less than one day, from this morning’s open of 80.90 to a current high of 81.91 following the announcement.

From a technical perspective, the pair has just reached a tranche of obstacles, however, which could make upside progress more difficult.

It is currently intersecting with the 50-day moving average (MA), which is a strong level of dynamic support and resistance and will prove difficult to overcome.

It is also only marginally above the 200-month MA at 80.80, which will also prove difficult to break free from.

Nevertheless, the news of an election is a positive sign for sterling as it raises the possibility of a softening or even possible reversal of Brexit if a more pro-EU government were to gain power, and this provides a strong fundamental stimulus which could be enough to overcome the resistance provided by the exchange rate.

A further bullish sign is the double bottom reversal pattern which has formed at the lows.

Double bottom’s look like the letter ‘W’, and are activated when the exchange rate breaks above the neckline at the high of the intervening peak between the two troughs.

We would want to see a clear break above the neckline at 82.07 – confirmed by a move above 82.15 - to signal an extension higher.

The target generated by activation of a double bottom is equal to the extrapolation of the height of the double bottom from the neckline up, but in this case the major trendline situated above the pattern provides a nearer-term target at 83.00.

The rising MACD, which has been converging with the fall exchange rate on the last two troughs, is a further bullish signal.

Rupee Expected to Remain Strong

For those looking for a pair with which to capitalize on current Sterling strength, however, the Rupee may not be the best choice given analysts are certain it will continue strengthening itself.

The twin effects of a record rise in inflowing capital buying up Indian assets and excess liquidity which cannot be recycled by purchasing imports rapidly enough are causing a rise in the value of the Rupee.

“So what underlies the recent appreciation of the INR? In our view, the surge in foreign portfolio inflows in March and early April amidst excess liquidity and a surplus in the basic balance of payments (BoP) have forced the authorities to tolerate a faster pace of INR appreciation,” said ANZ Bank’s Sanjay Mathur in a recent note on the currency.

The main reason for strong INR is the excess inflow problem following the government’s victory in Uttar Pradesh.

This raised hopes the government would push through further economic reforms which lead to an increase in foreign investment.

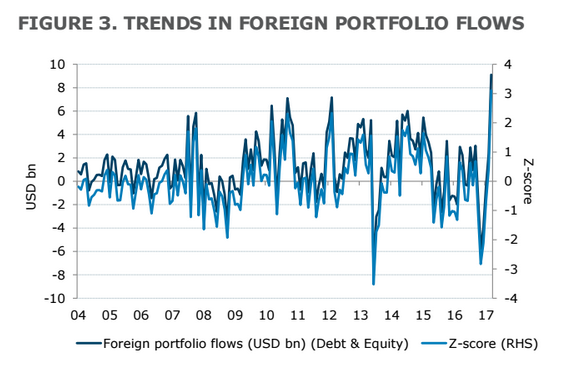

“Inflows in March 2017 had amounted to INR9.1bn, the highest on record. Inflows between 3 and 12 April also added up to a solid USD1.9bn (Figure 3).”

The economy is too weak, however, according to Mathur, to absorb these inflows.

“Surges in foreign portfolio inflows are not unusual for India although not to the same extent as recently. However, a critical difference between previous episodes of surges in portfolio flows such as those in 2010 and 2014 and the present time, is that the real economy is currently weak and incapable of absorbing these inflows through higher imports,” said ANZ.

The Indian government’s initiative to increase bank deposits by phasing out higher denomination notes in circulation created a liquidity glut as people rushed to deposit their higher notes and savings before the deadline rendered them worthless.

This glut has been even more augmented by the increase of inflows, which are more often than not destined for Service companies making them less easy to recycle.

“It should also be noted that the bulk of foreign direct investment (FDI) is in the services sector or for acquiring stakes in already established companies and therefore, cannot easily be neutralised by imports of capital goods. In the absence of this outlet, the burden of managing inflows has fallen squarely on the RBI,” said Mathur.

The Reserve Bank of India does not have the available tools to deal quickly and efficiently with the problem.

“The available toolkit of the Reserve Bank of India (RBI), though extensive, may still be inadequate to absorb the massive liquidity surplus in the system. The proposal to introduce an uncollateralised standing deposit facility (SDF) to augment the central bank's capacity to manage liquidity is symptomatic of this inadequacy,” said ANZ.

The Answer: Market Stabilisation Scheme Bills and Bonds

According to ANZ’s Mathur the answer to the liquidity glut problem may be the RBI’s MSS (Market Stabilisation Scheme).

The MSS scheme was launched in April 2004 to strengthen the RBI's ability to conduct exchange rate and monetary management.

The bills/bonds issued under MSS have all the attributes of the existing treasury bills and dated securities.

These securities will be issued by way of auctions to be conducted by the RBI. The timing of issuance, amount and tenure of such securities will be decided by the RBI.

The purchasing of the MSS assets by commercial bansk will soak up the liquidity overspill.

“Issuance of MSS bills/bonds will probably be the preferred instrument of liquidity absorption,” says Mathur.

However, “MSS issuance also entails a fiscal cost and beyond a point, could impinge on the government’s deficit,” he adds.

This cost is borne by the government, because interest payments on MSS bills/bonds are borne by the state.

Another tool the RBI is considering introducing it SDF – or Standing Deposit Facility – which allows Banks to park money and earn interest with the RBI overnight.

“The principal advantage of the SDF is that it is uncollateralised, implying that the RBI will not be constrained by its holdings of government securities as is the case with reverse repos and OMOs. Several countries including Australia, the Philippines and Indonesia have successfully implemented similar facilities.”

SDF cannot be implemented quickly, however, as it would require an amendment in the RBI charter which currently does not allow the central bank to issue any bonds or deposit facilities on its own account.

Bottom Line: If Inflows Continue Rupee To Remain Strong

The “low absorption capacity of the real economy,” combined with a liquidity glut and excessive foreign inflows means the Rupee is likely to remain overvalued for some time unless the authorities can find an escape valve.

The RBI’s lack of tools to deal with the overhang, however, make it unlikely the excess overspill will find a destination quickly.

“The proposed implementation of the SDF is a step in the right direction but several operational issues will need to be resolved to ensure its success.

“In the interim, the RBI may well be forced to tolerate further appreciation of the INR, particularly if foreign portfolio inflows do not abate,” concludes ANZ’s Mathur.