- GBP/EUR forecast below 1.10 again

- Inflation to continue cooling as strengthening Sterling impacts prices

- Quotes: Pound-to-Euro exchange rate @ 1.1473, Pound-to-Dollar exchange rate @ 1.4203

© John Gomez, Adobe Stock

Another prominent foreign exchange professional has questioned the validity of Pound Sterling's strong run higher against both the Euro and US Dollar, giving three reasons for staying sceptical on the UK currency's recent run higher.

The Pound has risen to multi-month highs against both the Euro and US Dollar this week, but we warned ahead of the mid-week slump in the currency - triggered by under-par inflation data - there were those in the analyst community who were warning the move was getting stretched.

Adding to this view is Andreas Steno Larsen, a foreign exchange analyst with Nordea Markets - the investment banking branch of the Scandinavian banking giant Nordea Bank.

"The GBP has been the market darling so far this year, as Brexit progress and firmer Bank of England rhetoric have boosted the sterling. But don’t buy into the current positive GBP consensus," says Larsen

Larsen offers three reasons to question Sterling's strength:

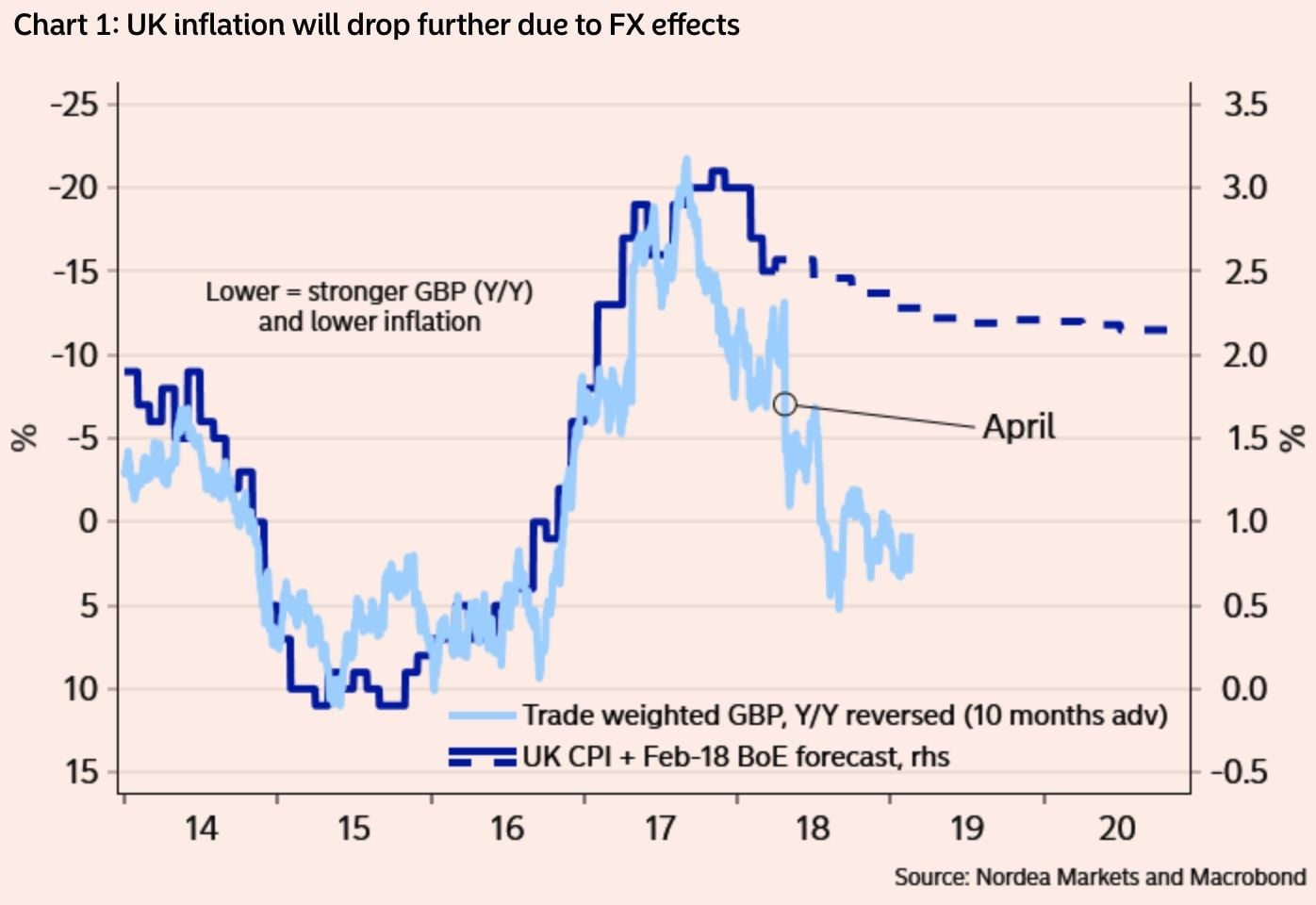

1: Inflation is poised to drop further

A significant sell-off in Sterling was seen on April 18 following the release of March inflation data from the Office for National Statistics which showed both headline CPI and core CPI to be falling faster than economists and the Bank of England had been anticipating.

Headline inflation fell to 2.5% during the recent month when markets had expected it to hold steady at the same 2.7% seen in February. This is far beneath the Bank of England forecast for inflation of 2.8% in the first quarter.

Core inflation, which removes volatile food and energy items from the goods basket and so is seen as a more reliable measure of domestically generated inflation pressures, also posted a surprise fall when it dropped from 2.5% to 2.3%.

For Nordea Markets, inflation is not going in a direction consistent with a Sterling-supportive Bank of England policy path.

"If historical correlations are anything to go by, the next 2-4 months should bring UK inflation substantially lower – and especially next month’s print will be negatively impacted by FX effects. The Bank of England estimates that Q2 inflation will average 2.7% – it could easily end up averaging well below 2.5%," says Larsen.

However, we would caution there is another popular view which we share and it is this: falling inflation, particularly from such high levels, is ultimately good for the economy in that it takes the pressure of consumers who have for months now seen earnings outstripped by pay increases.

This bodes for a more robust economic performance in 2018 and could in fact suggest to the Bank that raising interest rates can be tolerated by the economy; the path to normalisation will therefore be smoother, and the time to normalise is now.

Now IMF is warning about the perils of low interest rates, leading to an unsustainable build-up of debt. It is a shame that earlier warnings on this issue have not been heeded. https://t.co/omrdEjp99O

— Andrew Sentance (@asentance) April 18, 2018

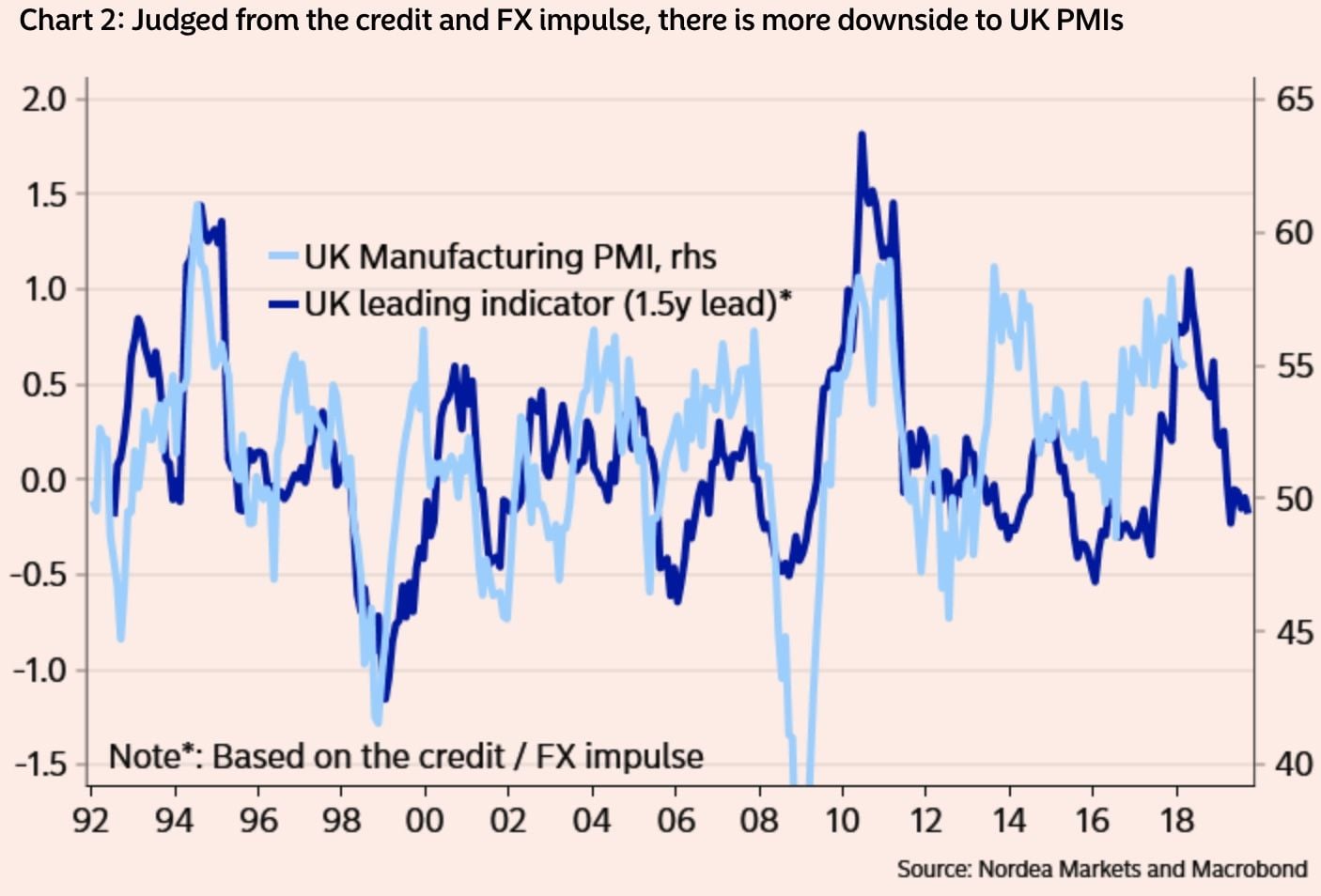

2: UK PMIs "are Vulnerable"

UK economic momentum is fading, as suggested by recent PMI data series released by IHS Markit which are widely seen to be the most accurate and timely survey data available on the economy.

The UK composite PMI dropped two index points in March from 54.5 to 52.5 with the all-important services PMI falling to its lowest level since the EU referendum.

"And as the Global PMI momentum is generally fading, we judge that UK PMIs are amongst the most vulnerable. During 2017 UK PMIs were underpinned by the weakening of the Sterling and by a benign credit impulse from the QE extension and lower interest rates implemented by the Bank of England in the aftermath of Brexit. Both of those positive (FX and credit) impulses to UK PMIs are fading – and that means further downside risks to UK PMIs in coming months," says Larsen.

We do also however caution that the soft-start to the year is often characteristic of the UK, the country does tend to see economic performance improve as the months pass. Indeed, the poor weather that characterised the start of 2018 could well point to grounds for improvement.

Advertisement

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.

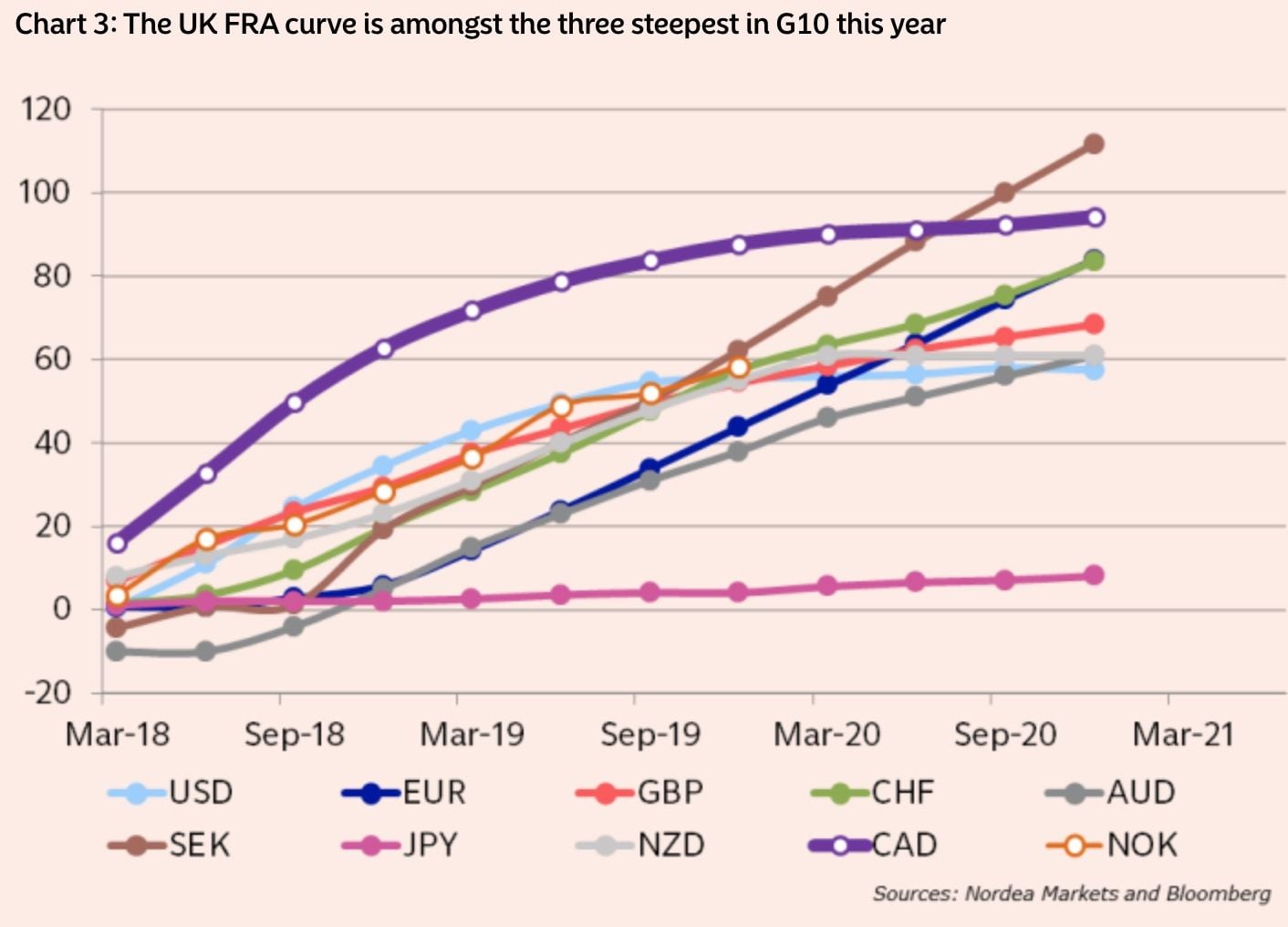

3: Bank of England pricing is already stretched

The question of Bank of England interest rate rises are a key driver of Sterling; the rule-of-thumb being that the faster the expected pace of hikes, the stronger the Pound, the slower the rate of hikes, the weaker Pound will go.

For Nordea Markets, the pricing of the Bank of England is too aggressive considering the fading inflation and growth momentum.

Until the end of 2018 more than 40bp are priced into the UK sterling futures curve (on top of the already big implied probability of a hike in May). That implies at least one further hike on top of the expected hike in May.

"As inflation momentum is fading, PMIs are fading and wage growth is only picking up moderately, we wouldn’t be surprised if the Bank of England decides on a very soft message to accompany the hike in May," says Larsen. "It is not a foregone conclusion that a hike will be quickly followed by more hikes."

This view is shared elsewhere, notably by Samuel Tombs at Pantheon Macroeconomics who has declined to join the consensus view that the Bank of England will raise rates this May, saying it would instead opt to see whether the recent run of lacklustre economic releases are temporary.

"Inflation has undershot the MPC’s forecast, 2.8%, again, suggesting that investors have concluded too hastily that a May rate hike is a done deal. The boost to inflation from sterling’s depreciation is fading much more swiftly than the Committee anticipated," says Tombs. "The MPC likely will conclude that it needs to increase Bank Rate by 0.25% only once this year."

Nordea's Forecasts for the Pound

Summing up the above, Nordea Markets say they forecast 0.91 in EUR/GBP over the coming 3-5 months, implying a Pound-to-Euro exchange rate of 1.09-1.10. This is in turn likely to place downside pressure on the GBP/USD, but Nordea don't have a specific price target for this pair.

"Despite the inflation setback, there is still a high likelihood of a hike by the Bank of England in May, but we don’t consider it a done deal. And the risk/reward is probably best in betting against a hike," says Larsen.

But, and here is a glimmer of hope, "longer out (+12 months) the valuation versus PPP/fair value models is still supportive of a stronger GBP."

Advertisement

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.