The UK economy is set to end 2017 on a stronger-than-forecast footing, according to new survey data, and an under-pressure Pound Sterling has welcomed the news.

The Pound edged higher against the Euro and Dollar Friday after the all-important Services PMI from IHS Markit and the CIPS rose faster than was expected for October.

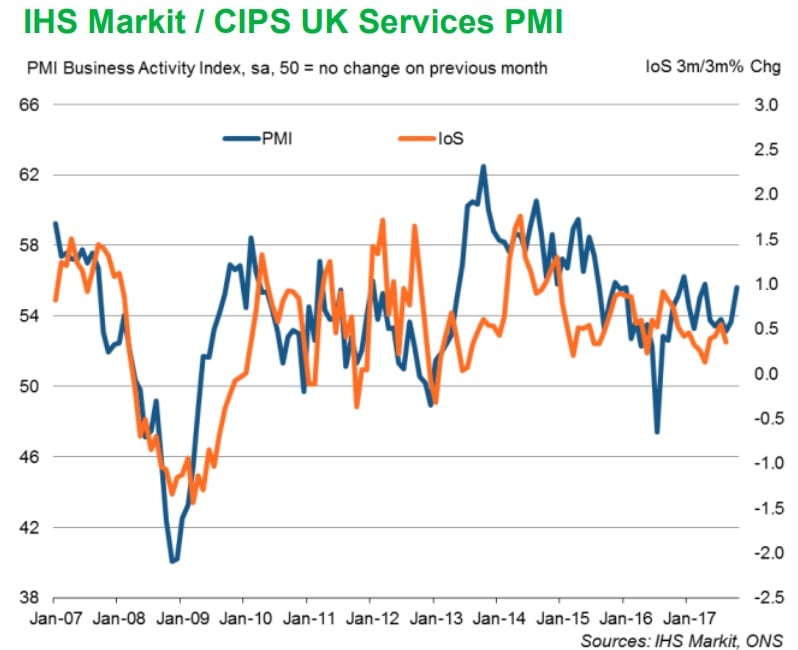

October’s purchasing manager’s index (PMI) reading came in at 55.6, up from 53.6, when it had been forecast by economists to edge downward by a fraction.

Activity in the services industry, which accounts for around 80% of UK economic output, rose at its fastest pace since April. Resilient client demand and a solid rate of new orders were cited as being among the factors behind the move.

“The good news was that October saw business activity across services, manufacturing and construction grow at its fastest rate for six months,” says Chris Williamson, chief business economist at IHS Markit.

Despite the surprise surge, Williamson notes that business confidence took a dent during the month due to concerns over the pace of client investment over the coming quarters. Such concerns are a symptom of uncertainty over the extent to which investment could be impacted by Brexit-related developments.

Williamson also flags a six month low in the rate of new job creation across the services sector during October - although this follows several quarters of strong gains.

"On the basis of past form, the index points to an acceleration in services growth from Q3’s 0.4% rate to about 0.7% or so," says Ruth Gregory, a UK economist at Capital Economics. "The strengthening of the survey’s forward-looking balances suggest that the services sector should be able to sustain this momentum too."

The report suggests the UK economy approaches year-end in better shape than it was just a few months previously, providing much-needed support for Sterling.

The Pound-to-Euro exchange rate was quoted 0.54%% higher at 1.1285 around the London close after falling by around 1.4% Thursday.

Above: The Pound-to-Euro exchange rate shown at hourly intervals.

The Pound was quoted 0.11% higher against the Dollar at 1.3066 around the London close after similarly steep losses Thursday.

Above: The Pound-to-Dollar exchange rate shown at hourly intervals.

The services PMI makes it a clean-sweep for the November PMI releases - construction and manufacturing industries both came in better than was expected this week, with the respective indices rising when they had both been forecast to sit relatively flat.

"Following the improvement in the manufacturing and construction surveys earlier this week, the economy-wide PMI rose from 53.6 to 55.3, suggesting that quarterly GDP growth is running at about 0.5%, a bit above Q3’s 0.4% rate," says Capital Economics' Gregory.

October’s PMI surveys follow closely on the heels of the latest GDP report that suggested the UK economy may have regained some of its lost momentum during the third quarter, but they also come in the wake of a Bank of England interest rate hike that roiled markets.

Get up to 5% more foreign exchange by using a specialist provider by getting closer to the real market rate and avoid the gaping spreads charged by your bank for international payments. Learn more here.

Bank of England Jilts Markets

Despite the positive tone set by the latest economic statistics, the Pound has its work cut out if it is to reclaim lost ground, partiuclarly after Thursday's price action.

The Pound suffered falls in excess of 1.0% against the Dollar, Euro and a host of other major currencies after the Bank of England raised interest rates for the first time in more than a decade.

An interest rate rise is typically viewed as positive for a currency but hints from the Bank about future rate rises seen Sterling into decline.

“The BoE surprised on the dovish side yesterday (despite the 25bp hike) given the downgrade to its forward rate guidance – dropping the wording that market expectations for future rate increases are too low,” says Petr Krpata, chief EMEA foreign exchange strategist at ING Group.

Markets had duly anticipated the Bank of England would add 25 basis points to the cash rate Thursday, taking it to 0.50%, but were also pricing a further two hikes to come once into 2018 and beyond.

“Given that the BoE rate outlook previously provided a fair degree of support to GBP, sterling’s collapse yesterday should not come as a surprise,” Krpata adds.

Crucially, for traders, the Monetary Policy Committee omitted an earlier-clause that said rates might need to rise “faster than the market expects” over the coming years, from its statement which left markets with the impression that earlier bets were either on-the-money or overly optimistic.

“Whilst the MPC managed a “dovish hike” yesterday, we suspect there is a greater risk of that impact fading going forward,” says Derek Halpenny, European head of global markets research at MUFG. “With the 2-year Gilt yield trading below the official Bank Rate, we view current market pricing as overly pessimistic.”

Next Up: Back to the Brexit

With the Bank of England's eagerly anticipated rate hike now a fixture in the rearview mirror, attention returns to the November budget from the Chancellor and the state of Brexit negotiations, both of which could exert influence over the direction of Sterling.

“The key going forward is not the forward guidance of the MPC but economic data and Brexit progress. The financial markets have a natural tendency to maintain a risk premium related to a cliff-edge Brexit in March 2019,” Halpenny notes.

Brexit negotiations will resume on November 09 and 10, where markets will look to see signs that a deal is near, while the UK Treasury is set to unveil its latest budget on November 22.

“We now expect GBP to settle at the post BoE outlook adjusted (softer) levels with the next near-term catalyst for a change in GBP direction being 2017 Autumn Budget (22 Nov),” says ING’s Krpata.

The budget is key not only because it could yield the announcement of fiscal policies that impact the economy, but because it could also give way to renewed effort to oust the Chancellor Philip Hammond.

Hammond is one of the cabinet voices to have sought continued membership of the single market and customs union for the UK after March 2019 and is seen by the market as one of the government’s key supporters of a so-called soft Brexit.

Concerns are that, given his track record of controversial policy announcements and relative unpopularity with the party membership, budget that goes down poorly could see backbench MPs attempt to remove him from office.

Get up to 5% more foreign exchange by using a specialist provider by getting closer to the real market rate and avoid the gaping spreads charged by your bank for international payments. Learn more here.