With Pound Sterling having risen sharply against the Euro this week, should speculators look to bet on a decline from these levels? We hear two arguments for and against.

Right now, the Pound is being driven almost exlusively by expectations for future moves on interest rates at the Bank of England.

But, the narrative will ultimately revert back to the tricky issue of Brexit negotiations we are told.

And on this front, traders should be inclined to view a recovery of the Pound-to-Euro exchange rate as a selling opportunity as opposed to a sustainable turnaround.

This is the view of strategists at Rabobank who say parity between the two currencies cannot be ruled out.

The Dutch bank issued its recommendation amid a broad correction in the Pound, brought about by a hawkish turn at the Bank of England that has now led traders to bet on an interest rate hike in the UK as soon as November.

“Our central projections put EUR/GBP at 0.96 on a 12 month view and to 0.98 in 15-18 months, though we do not rule out a move to parity if politicians fail to allay fears that a cliff edge is looming,” says Jane Foley, a senior fx strategist at Rabobank.

Foley sees the re-emergence of a Brexit related narrative as a likely source of downside pressure on the Pound toward year-end.

“It is possible that the BoE could ratchet up the hawkish rhetoric at this week’s policy meeting which could steer GBP on a firmer course near-term,” Foley said in a note earlier this week.

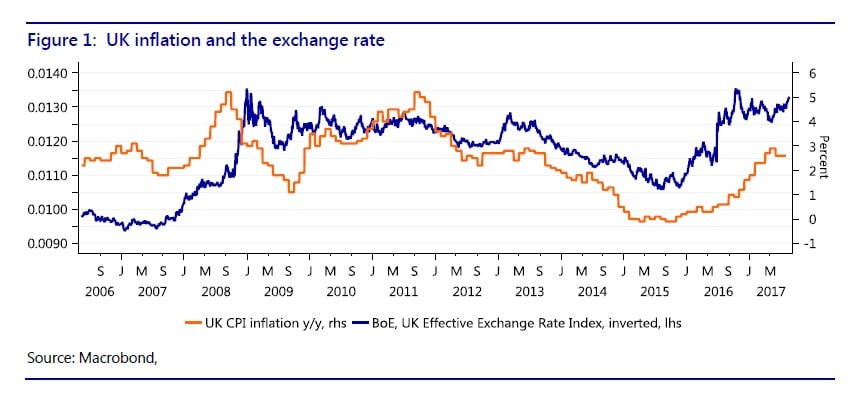

Bank of England hawkishness comes after August inflation rose more than was expected, threatening the 3% level, with the figures highlighting how a devalued Sterling continues to drive consumer price pressures further north of the BoE’s 2% inflation target.

Should CPI reach 3% then the Bank of England Governor, Mark Carney, will be required to set out plans to bring it down, in a public letter to HM Treasury.

UK CPI Inflation & GBP Effective Exchange Rate. Source: RaboResearch.

With less than 18 months to go before Britain’s scheduled exit from the EU, and little concrete progress to date on post-Brexit trade, Foley and the Rabobank team see downward pressure on the Pound renewing over the coming months.

“Consequently, we would be looking at a near-term recovery for Sterling as a selling opportunity vs. the EUR,” says Foley.

Brexit negotiations not moving beyond the so-called financial settlement by year-end could be the catalyst for further losses.

Too Soon to Sell

But Oliver Harvey, a Macro Strategist with Deutsche Bank in London says it would not be wise to lean against the Pound at this stage.

"Yesterday's meeting was even more hawkish than we expected and we have subsequently changed our rate call for a hike in November. With this still less than 100% priced, and given the build up in short positioning over recent weeks, we wouldn’t fade the rally in GBP just yet," says Harvey.

The Deutsche Bank analyst notes the market is still only pricing around a 50-60% likelihood of a rate hike in November and there could therefore be further catch-up to play, which will support Sterling.

But absent a meaningful deterioration in labour market or growth data, "we expect the BoE to raise rates. While we don't see this as the start of a Fedstyle hiking cycle, GBP remains very cheap on short-end spreads," says Harvey.

Get up to 5% more foreign exchange by using a specialist provider by getting closer to the real market rate and avoid the gaping spreads charged by your bank for international payments. Learn more here.

Top Of The Class

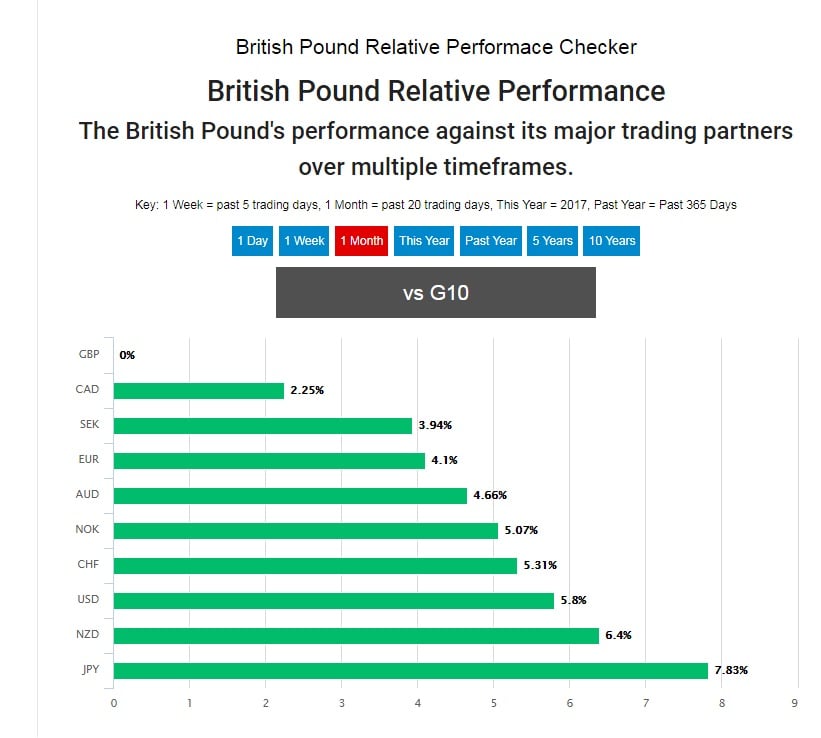

The Pound-to-Euro rate has risen by 2.6% during the last week and its year to date loss has slimmed to just -4.4%, down from more than 7% last week.

The is while the Pound-to-Dollar rate has risen by a lesser 1.6% during the recent week, to trade at a new one-year high of 1.3450, and is up by nearly 9% for the year to date.

In the last week, Sterling has been the best performing currency in the G10 basket. It has gained nearly 5% against the Japanese Yen.

"Counting Hawks": A Carney Call, Or Nothing At All?

Added to the prospect of mounting political pressures on the Pound, the Monetary Policy Committee is likely to keep the bank rate at its current record low of 0.25% until August 2018 as a minimum, according to Foley.

“Although we expect the majority of the committee to remain in favour of steady rates until August 2018 at the earliest, we do expect most MPC meetings between now and then to contain hawkish undertones,” says Foley.

Foley’s forecast suggests Bank of England rate setters may talk tough over the coming months, but action from the Old Lady of Threadneedle Street will probably be quite thin on the ground, which begs a question.

Can Jawboning Alone Prop Up The Pound?

Recent history shows central bank jawboning alone is unlikely to have a durable effect on market pricing of a currency when fundamentals strongly favour the other side of a policy maker’s trade.

The European Central Bank’s recent failure to coax the Euro back from a two and a half year peak against the Dollar is a case in point.

And with UK economic growth slowing sharply in the first half and the economy appearing in a fragile position during the third quarter, it still remains to be seen whether the economy could actually withstand any withdrawal of stimulus or tightening of policy.

“We expect Sterling to resume its decline before long, as the macro data flow show further UK growth deceleration,” said Guy Stear, an economist at Societe Generale, in a note earlier this week. Stear said Friday that market pricing of an interest rate hike in the first quarter of 2018 is excessive.