The immediate outlook for the Pound to Euro exchange rate rests with the message delivered by the European Central Bank at their September policy meeting - here are the issues to consider.

Pound Sterling needs a game-changer aginst the Euro.

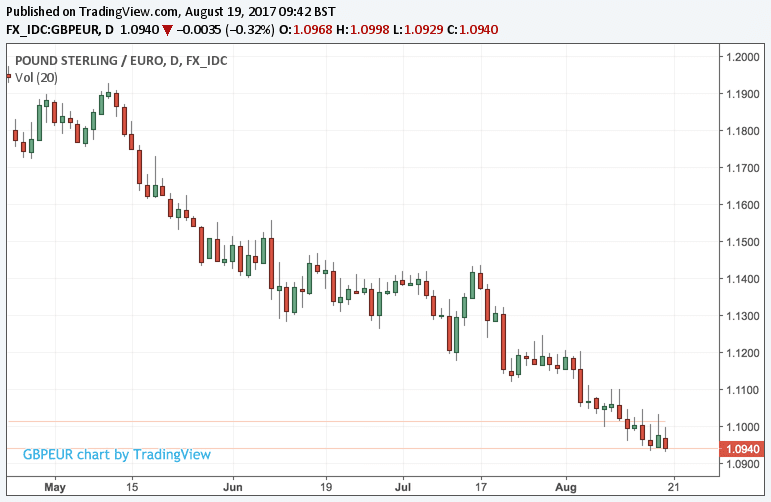

Technical studies tell us that the trend is still unrelentingly pointed lower across all timeframes, so readers hoping for a stronger UK currency must reconcile themselves with the uncomfortable truth that values will likely continue to get worse before they get better in the current market environment.

The Euro "has seen a strong rally since April this year and reinforced its large base set above 0.8852. This keeps the immediate risk still higher," says Christopher Hine, a technical strategist with Credit Suisse commenting on the EUR/GBP outlook.

He believes that there is a very real prospect that the EUR/GBP breaks through resistance at 0.9142 and ultimately hits his “core target” at 0.94.

This gives a fall in the Pound to Euro exchange rate to 1.0633.

Above: Don't try and catch a falling knife: The Pound is going lower according to technical analysts.

Of course this might or might not come to pass and the GBP/EUR could turn around or crack even lower.

What is clear to us is that until we get some real meat in Brexit talks, GBP/EUR’s near-term future rests largely with what happens to the Euro.

How much more strength can it offer, and what could halt or accelerate the strength?

The answer almost certainly rests with the European Central Bank.

The Only Game in Town: The ECB

In July the Euro shot higher as - at a press briefing - ECB President Mario Draghi effectively offered a sanguine response to a question as to whether or not he thought the Euro’s rapid rise to date was of little concern.

"It's true there have been movements in bond price, asset price, exchange rates and so on," noted Draghi, "but financing conditions remain supportive."

We reflected that the ECB President had effectively green-lighted the Euro’s strength to markets who stocked up on yet more Euros.

“Draghi’s verbal shrug-of-the-shoulders on the exchange rate encouraged the subsequent EUR appreciation,” says Mark Wall, Chief Economist at Deutsche Bank.

Above: Watch the full press conference where Draghi shows little concern for a rising Euro.

This narrative has however been questioned on August 17 after the ECB released the minutes to its July meeting and the message appears to be a little different.

The account of the ECB’s July monetary policy meeting have been published in which “concerns were expressed about the risk of the exchange rate overshooting in the future.”

This line spooked markets and the Euro gave up ground to the likes of Sterling and the US Dollar.

So we have mixed messaging here - on one hand Draghi is saying he isn’t too fussed and on the other the minutes to the meeting Draghi had just attended suggest the ECB is actually fussed.

Markets will take this mixed messaging on board and will therefore wait for more direction. It’s by no means a signal of intent by the ECB that it will pursue a weaker exchange rate.

For sure, the ECB will be happy that markets have calmed down somewhat; they would rather the Euro moved higher at a more pedestrian pace.

It could therefore be that the Pound to Euro exchange rate continues to head lower, albeit at a slower pace.

But time and again we have heard central banks talk their currencies down to only see it head in the other direction as the key point about verbal intervention is it needs to be backed up by action.

The second the market figures out that the words coming out of the Chief’s mouth are hollow, they will exact punishment.

That is why the ECB’s approach to its tapering programme is ultimately where the Euro’s fate lies.

Get up to 5% more foreign exchange by using a specialist provider by getting closer to the real market rate and avoid the gaping spreads charged by your bank for international payments. Learn more here.

What is Tapering and Why Does it Matter?

The European Central Bank is currently buying €60BN worth of bonds a month under its quantitative easing programme which seeks to ensure price financial stability in the Eurozone - it is hoped injecting this amount of cash into the economy will stimulate growth and push prices up such that inflation reaches a target of 2%.

But months of better-than-forecast economic growth suggests prices will soon rise to hit target and the bond purchase programme therefore becomes redundant at best, dangerous at worst.

For markets the question becomes how and when the €60BN bond buying programme - also known as quantitative easing - is shut down.

How this is done is incredibly important - go too fast and interest rates and the Euro shoot higher which could potentially destabilise the Eurozone. Go too slow and the economy could overheat and inflation surges beyond the 2% target.

Markets expect the ECB to announce a slower pace of asset purchases in September, with actual tapering likely to begin in early 2018.

Economists believe the ECB will likely bring monthly purchases down by €15–20 billion and should take at least a quarter.

Anticipation for such a move has seen the Euro move notably higher against the US Dollar, Pound Sterling and most other major currencies over the course of 2017.

The risk now is that the ECB - having seen how high the Euro has climbed - decides to push back the date of tapering. They could also announce a smaller-than-expected taper amount which would see the programme run for longer than many are expecting.

For instance, Deutsche Bank’s view is the ECB may announce at the press conference on 26 October that it is extending QE until mid-2018 at the slower rate of EUR40bn per month.

Such a move would certainly shake the Euro lower; the key vulnerability for the currency right now therefore is the whole debate around tapering.

The Way Forward: September 7 = The Euro’s Day with Destiny

The Euro’s route forward is likely to be determined by communications from key ECB board members and communications from the Bank itself at official meetings.

Watch Draghi’s appearance in Jackson Hole, Wyoming where he is to attend the Kansas Fed’s Symposium.

In the past he has signalled policy intentions at the event. While press reports suggest this time no such communication is likely, he could still directly address the Euro’s valuation.

Again, talk will likely have limited impact on the Euro.

The biggie for the Euro therefore comes at the September ECB meeting where forecasts from the Bank’s staff are also released. This would likely be where the intent to taper is announced.

No taper announcement in September will surely hurt the Euro hard. The meeting takes place on September 7.

So until then, remember the trend is your friend - or rather not your friend if you are dismayed by the Pound’s relentless decline in value.

Get up to 5% more foreign exchange by using a specialist provider by getting closer to the real market rate and avoid the gaping spreads charged by your bank for international payments. Learn more here.

Markets Occupied with Terror

Headlines will prove a distraction for markets on news of a major terror attack in Spain's Catalonia region.

13 people were killed in an attack in Barcelona after a van drove into crowds before five suspects have been shot dead as police intercepted a car that was running people down in the Spanish town of Cambrils.

A picture is emerging this morning of an apparently coordinated terror plot to hit multiple targets across the country’s Catalonia region.

"It was also a sea of red on European share market bourses. Investors showed favour for safer-haven assets like bonds, after a tragic terrorist attack in Spain," says Janu Chan, an economist with St. George Bank.

Five terrorists wearing fake suicide belts have been shot dead by police after ramming civilians with a car in a Spanish seaside town in a second vehicle attack, as police named a man being hunted as the suspected Barcelona van driver.

One woman died and six other people, including a police officer, were injured in Cambrils - hours after a rampaging van driver left 13 people dead and more than 100 wounded around 70 miles away in Barcelona.