A strong short-covering rally in Pound Sterling saw the currency easily outperform its G10 rivals but can further gains be expected over coming days? We assess what the coming week holds.

- Pound to Dollar exchange rate today (6-11-16): 1.1237

- Pound to Euro exchange rate today: 1.2520

- Euro to Pound Sterling exchange rate today: 0.8902

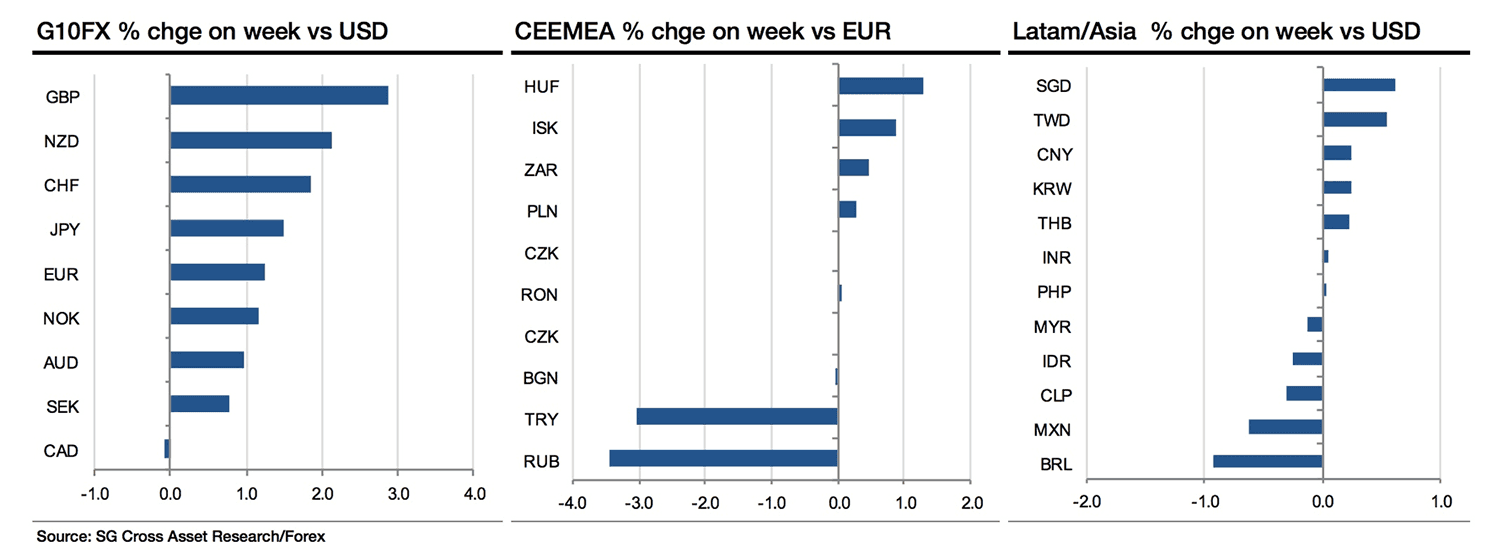

The currency performance board for the week 31st October-4th November saw GBP come out on top while the US Dollar only marginally managed to outperform a maligned Canadian Dollar.

Indeed, the biggest story involves the negativity heaped on North America currencies as polls tighten ahead of the November 8th U.S. presidential elections.

As can be seen the US Dollar, Canadian Dollar and Mexican Peso all had a rotter of a week:

"The week has all been about the shrinking opinion poll gap between Hillary Clinton and Donald Trump. A 7 point lead for Mrs Clinton two weeks ago has been whittled down to 1.3% on the last reading and anxiety haunts the currency market. The Dollar’s the main loser in G10, beating only the Canadian Dollar which is an obvious ‘loser’ from Mr. Trump winning," says Kit Juckes, a strategist with Societe Generale in London.

The second big story of the week was the short-squeeze higher in Sterling.

“A game change of a week for Sterling had it up around 2.5% and on pace for its best since March,” says Joe Manimbo at Western Union. “The short-run game for the pound changed for the better after the risk of an economy-choking hard-Brexit receded after the U.K. High court ruled that Parliament would have to approve the government’s Brexit plan.”

Pound heads for longest run of gains since before Brexit vote https://t.co/XJgbwNG6lD pic.twitter.com/Y8X981AWxv

— Bloomberg Brexit (@Brexit) November 4, 2016

The Bank of England further aided Sterling after shifting its policy bias into neutral from rate-cutting mode, while it also helped Sterling sentiment that Governor Mark Carney agreed to stay 12 months longer until mid-2019, offering a welcome sense of continuity as the country navigates its exit from the European Union.

“The pound has had an exceptional week in the light of a series of political events relating to Brexit and the economy,” says Paresh Davdra, CEO and Co-Founder of RationalFX.

A big pop higher was delivered on Thursday October 3rd when the Bank of England surprised markets by notably upgrading their growth forecasts for the UK economy.

The Bank also communicated they they do not see further interest rate cuts as being likely with market pricing going so far as suggesting the next move could be to actually raise interest rates.

Expectations for higher interest rates tend to be supportive of currencies.

Sterling also benefitted on the US Dollar’s woes stemming from Donald Trump’s better performance in the US election polls which unsettled investors.

America goes to the polls on the 8th November and, “if this week is any indication, the culmination of the US elections and uncertainty over who the next President might be could prove to be beneficial for the pound in the immediate future,” says Davdra.

Latest Pound/Euro Exchange Rates

| Live: 1.1803▼ -0.07%12 Month Best:1.1828 |

*Your Bank's Retail Rate

| 1.1402 - 1.1449 |

**Independent Specialist | 1.1638 - 1.1685 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

It is too early to say how a victory for either side will influence foreign exchange markets but we would warn that volatility is highly likely.

"The polls continue to tighten and we see the risk that following payrolls market liquidity dries up, as market participants await for Tuesday’s election results. Reduced liquidity is likely to inject greater dispersion in the price action," says Mark McCormick at TD Securities.

So far we note Trump's gains have been met with Dollar weakness as the policy uncertainty that the candidate brings could well see the US Federal Reserve shy away from raising interest rates in December.

It is the promise of a rate rise in December that is the ultimate guarantor of the Dollar's current strength.

The Week Ahead for the Pound

The Bank of England's press conference suggested that the contents of the Agents’ Survey were a key factor behind its change in stance.

"On the growth side, we suspect that reasonably steady investment intentions were behind the BoE’s belief that growth will hold up in the near-term. And on inflation, we expect to see strong signs of rising input costs, something that the PMI surveys have indicated are a major concern for businesses," say TD Securities.

The Bank's agents survey comes out on November 9th and forms the highlight of the week.

But for a currency that is sentiment driven it will be all about Brexit headlines and we look for the hard-Brexit story to become the key downside risk for a currency that really needs a kitchen sink of positivity thrown at it to eke out even the smallest amount of upside impetus.

Much of the hard-Brexit debate had been priced into the Pound this week but the Article 50 ruling on Thursday has seen much of it priced out again.

So we could well see Sterling suffer on any indications that the Government does intend to take a closed approach to next year's negotiations.

The Week Ahead for the Dollar

Markets continue to price in a high chance of a Clinton victory, but odds of a Trump win have risen, suggesting scope for an election surprise.

"Polls have progressively tightened and though are still in Clinton's favor, factors such as polling bias and low turnout mean that the outcome remains highly unpredictable. We recommend hedging a Trump victory, given our expectation for 5Y rates to fall 20-30bp in such an event," say strategists at TD Securities.

The Week Ahead for the Euro

TD Securities tell clients to watch this week's Eurogroup Meeting on November 7th.

"This meeting wasn’t really on our radar until a recent announcement that the topic of inflation would be added to the agenda, with the EC and ECB to present their assessment of recent inflation developments in the EZ. It’s a long shot, but perhaps FinMins will finally more seriously consider the structural reforms that Draghi has been asking for in order to support the region’s inflation outlook," say TD Securities.