A leading investment management company still see outstanding risk premia stemming from the uncertainty of the closely fought referendum campaign.

- “We see no significant, lasting damage to the UK economy.” - Michael Stanes at Heartwood Investment Management.

- Echoes view of fund manager Neil Woodward who calls Brexit a 'nil sum game' for economy

- Sterling to be the 'lightning rod' absorbing any further risk associated with the vote.

The close fought nature of the in-out campaign is likely to weigh on the pound as the date for the June 23 referendum nears, according to a leading portfolio manager.

However, the overall impact on the economy of the UK leaving or staying is relatively balanced.

Money manager Michael Stanes of Heartwood Investment Management, says U.K financial assets would likely have to absorb a risk premium in the weeks preceding the vote, with sterling bearing the brunt:

“A higher risk premium across UK financial markets is likely to persist in the interim to June 23rd, with sterling most likely to be the lightning rod.”

He also emphasized that sterling has already absorbed a fair share of the outstanding risk premium, possibly putting a limit of some sort on future losses:

“We have already observed the UK currency’s meaningful depreciation since David Cameron announced the new settlement with the EU, having fallen 6% on a trade-weighted basis since the start of the year.”

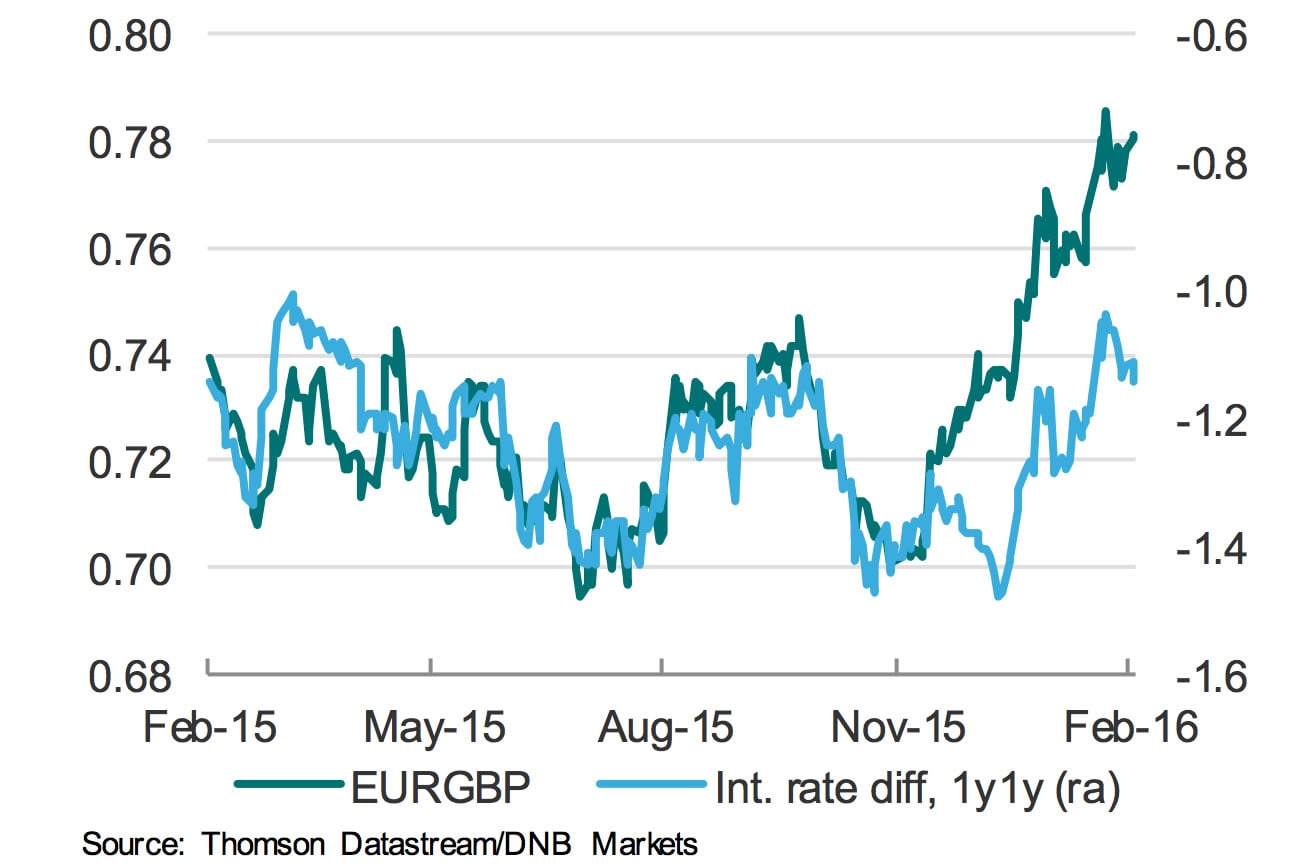

Above: Sterling should be higher against the euro according to the difference between UK and EU interest rates, bu these are not normal times.

Sterling Post-Referendum

How sterling will perform after the vote depends on the result, if the electorate vote to remain in the E.U, Stanes expects sterling and sterling denominated assets to rally:

“We would expect a vote to stay in the EU to be seen as business as usual and a net positive for UK financial markets, especially given concerns around funding the UK’s sizeable current account deficit.”

A vote to leave would lead to a more uncertain reaction from the markets – at least in the short-term, and a negative outlook for the pound:

“Sterling is likely to be most vulnerable on concerns of capital flight risk needed to fund the deficit, although its recent weakness has gone some way to reflect these risks.”

Latest Pound/Euro Exchange Rates

| Live: 1.1586▼ -0.14%12 Month Best:1.1754 |

*Your Bank's Retail Rate

| 1.1192 - 1.1238 |

**Independent Specialist | 1.1424 - 1.147 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

Stanes refrains from putting a figure percentage on sterling’s losses, unlike Capital Economics’s Roger Bootle, who suggested a vote to leave the EU would lead to a 15% fall in the pound.

Regardless of whether people vote to stay in or leave, Heartwood does not see any lasting damage to the economy:

“We see no significant, lasting damage to the UK economy.”

The view echoes that put forward by respected fund manager Neil Woodford who commissioned Capital Economics to establish the facts surrounding a Brexit.

In Woodford's view, Brexit and staying in the EU represent a 'nil-sum game' for the economy.

Gilts Most Resilient and German Bunds Taking Safety Demand

Hartwood sees Gilts as the asset class most resilient to the impact of investor concerns both before and after the referendum:

“The UK gilt market may sell off moderately, particularly if there has been a risk off trade in advance of the decision, but longer-term economic fundamental dynamics will continue to drive bond yields, which should be ultimately positive for gilts, and in particular there would be no clouds overhanging the UK’s sovereign credit rating.”

Heartwood pointed out that a flight to the safety would be the most probable reaction in Europe, with German assets gaining as a consequence:

“The financial repercussions of the UK’s departure from the EU should be contained from the European perspective, although expect short-term headline noise questioning the validity of the EU project. German assets would probably be considered a safe-haven for euro-based investors, as equity and bond markets in periphery countries come under pressure.”