Pound sterling forecasts have been reduced as the Bank of England shows it is unlikely to raise interest rates in 2016.

The Bank of England has, as expected, cut their forecasts for UK economic growth and inflation ensuring the prospect of a 2016 interest rate rise remains remote.

Sterling slumped dramatically by over a percent against the euro after it was shown all 9 members of the Monetary Policy Committee voted to keep rates unchanged.

Previously Ian McCafferty had voted for a hike. This suggests the prospect of an interest rate rise in coming months is more distant than ever and any hopes that the event would provide ammunition for a stronger pound have been dashed.

Exchange Rate Reaction: Turning Lower

The reaction by pound sterling to the Inflation Report and policy decision has thus far has been negative and we feel that the positive momentum built up at the start of February 2016 has been washed away.

The pound to euro exchange rate headed down from the day's open at 1.3142 to a close of 1.3017.

The pound to dollar fell from an opening rate of 1.46 to record a close of 1.4585.

The Currency Outlook

Maintaining a positive tone on the GBP's outlook is Andy Scott at HiFX:

“Sterling is unlikely to come under additional pressure as a result of today’s BoE forecasts as the market has already been pricing in the possibility of weaker growth and rates remaining on hold."

Scott reckons focus is likely to remain on the Dollar in the days ahead with global disinflationary forces growing and the U.S. economy slowing – the market is starting to discount the possibility of the Fed hiking this year.

Latest Pound/Euro Exchange Rates

| Live: 1.1673▼ -0.02%12 Month Best:1.1828 |

*Your Bank's Retail Rate

| 1.1276 - 1.1323 |

**Independent Specialist | 1.151 - 1.1556 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

James Rossiter at TD Securities believes that the outlook for sterling is more benign as Carney went to notable lengths to temper any overly-pessimistic conclusions during his press conference.

"This backdrop is likely to leave the GBP more reactive to external considerations than domestic ones, particularly as the UK economic data release calendar is relatively quiet over the next week or two. This suggests the broader near-term trends are likely to remain intact over the next several sessions," says Rossiter.

Inflation Report, Points to Note

- The Bank cuts prediction for GDP growth this year from 2.5% in November to 2.2%.

- Average weekly earnings to increase by 3% this year, down from the 3.75% forecast three months ago

- Inflation will remain below 1 per cent for all of 2016 and will reach its 2 per cent target only by the first quarter of 2018.

Analyst Reactions

"Inflation projections were revised down further in the Inflation Report. This significantly reduces the probability of an initial rate increase this year. We are therefore revising the expected path of sterling down, from GBP/USD 1.45-1.50-1.60-1.62 on the 3m-6m-12m-24m horizon to 1.42-1.48-1.55-1.60." - Asmara Jamaleh at Intesa Sanpaolo.

"The Report’s medium-term inflation projections were little changed from those in November, despite the downward drag of a marked further fall in oil prices and increased anxiety about the pace of global growth. As such, following today’s announcements, our central view of a first MPC rate hike in August 2016 – or indeed of a move this year – now looks less likely." - Lloyds Bank.

"We believe that McCafferty felt that the economy is not in a state to support the beginning of the hiking cycle and so his vote for a hike was no longer tenable. Overall, this supports our view that a hike is off the table until Q4 16," - Andrzej Szczepaniak at Barclays.

“Low inflation has clearly tied the MPC’s hands. However, there remains little reason to be concerned that the near-zero rate of inflation will be anything but good news for the UK. The reason prices are not shifting is because global oil prices have collapsed. This is completely different to if low prices were being driven by a lack of consumer confidence." - James Sproule, Chief Economist at the IoD.

"Amazingly, the first BoE hike is now only priced for 2018." John Cairns, RMB.

Markets Expected a Negative Event

The markets were positioned for a dovish outcome to today's event implying there were risks that sterling could bounce if the Bank was not negative enough. Yet they took no chances and shed exposure to the UK currency in the run-up to the 12:00 event.

The priced-in 12-month Bank of England rates outlook implied in overnight index swaps (OIS) has dropped to the lowest level since May 2013 of late confirming markets were not anticipating a cheery Mark Carney & Co.

In fact, the baseline view now sees a 64 percent probability that rates remain unchanged and a 36 percent probability of a 25 bps cut by February 2017.

Markets had priced the pound higher for at least one 2016 rate hike as recently as a month ago.

"British Pound positioning suggests this dovish shift has entered the exchange rate to a significant extent. Indeed, the latest CFTC Commitment of Traders report shows Sterling speculative positioning is at its most net-short since July 2013," says Ilya Spivak at DailyFX.

We have already reported that the risks to the pound sterling are biased to the upside heading into the event.

Nevertheless, Spivak believes the Bank will have to work particularly hard to drive sterling lower saying a dovish surprise is unlikely.

"For that, officials would probably need to explicitly signal an about-face reversal from their preference for a hike as the next policy move, shifting the conversation from speculation about timing to the direction of policy itself."

ING's Chris Turner sees risk that GBP rates firm a little and GBP performs a little better. "We continue to see a brief window for EUR/GBP to move back to the 0.7525 area and below."

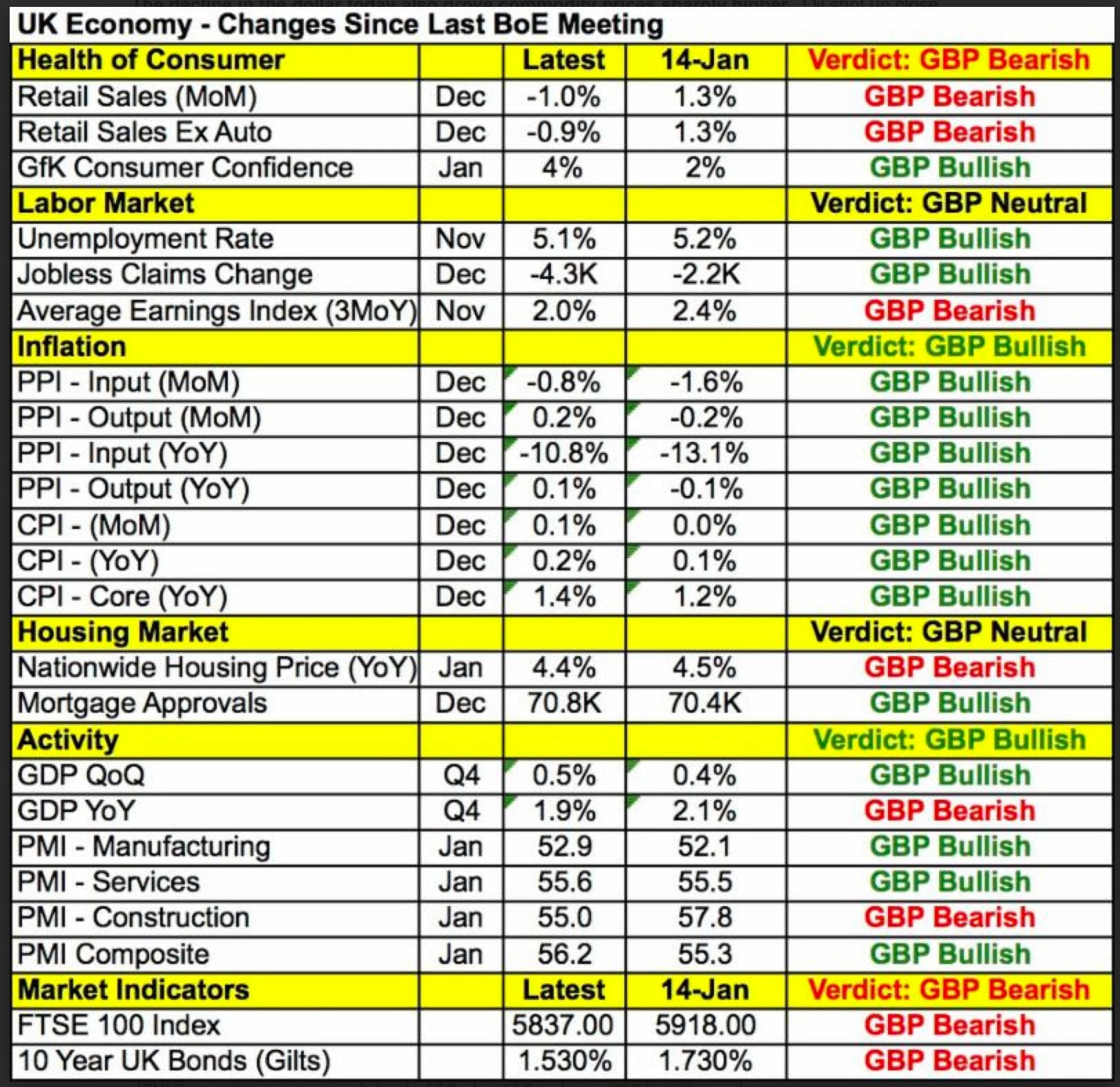

The data-flow out of the UK economy has been supportive of a more upbeat assessment. Look at the following table, courtesy of BK Asset Management:

The Agenda

The quarterly Inflation Report, interest rate decision and release of the minutes to that decision takes place at 12:00.

Governor Mark Carney is then presented before the press at 12:45 to expand on the Bank’s thinking.

Ahead of the event we note a scathing assessment of the Bank’s forward guidance policy.

Dominic Rossi, the head of global equities at Fidelity, has said in a BBC interview that Mark Carney and his team have done a good job on confusing markets with their policy guidance.

The thinking at the Bank is that guiding markets on when they may change policy smooths out the potential for shocks.

However, Rossi argues, “the Bank of England's inflation forecasts have been poor and therefore the guidance towards interest rates has been too aggressive at times and I think the fact the bank is now rolling back from yet another interest rate forecast illustrates the point."

Today we look for downgrades to the inflation and growth profile of the UK economy.

Most analysts we have received communication from do however note that the prospect for radical downgrades are slim.

Hence, the day could end up being positive for sterling. Stay tuned.