Consensus projections for the next four quarters, compiled from leading investment banks.

Access the full forecast →

Picture by Simon Dawson / No 10 Downing Street

Hints of another household energy bailout risk triggering another Truss-style crisis in UK financial markets.

A financially skint British government could introduce packages to support households in the face of a new energy cost shock, which seriously raises the odds of a destabilising bond market reaction.

"No matter the headwinds, supporting working people and their families with the cost of living is always top of my mind," said Prime Minister Keir Starmer on Monday concerning the issue of rising energy prices.

He said Chancellor Rachel Reeves was in touch with the Bank of England, which is the clearest sign that the government is worried that measures could trigger unforeseen financial reactions.

That Reeves is talking to the Bank is in itself a signal as it conjures up memories of former Prime Minister Liz Truss' time; she unveiled an energy support package for households in 2022, which at the time was estimated to cost £60BN for just the first six months.

That package was then followed by her infamous 'mini budget' that included tax reductions; markets assessed the totality of energy spending and tax reductions and sold UK bonds owing to concerns about the trajectory of UK debt dynamics.

But, a post-mortem of what happened at the time showed that this bond market selloff triggered an unforeseen problem in a corner of the pension funding system that ultimately turned the selloff into a fire sale.

The pound plummeted.

That Reeves is in touch with the Bank of England suggests she is testing the waters and scoping for potential issues in the financial plumbing to avoid a Truss-style meltdown.

However, the fundamentals are just as unenviable today as they were in 2022. The UK's debt dynamics have not improved since those days and the risks are the same: a significant increase in government borrowing will come at a time when other sovereigns are looking to borrow to fund their own mitigation strategies.

"We doubt further fiscal support for households - hinted at by the Prime Minister - can be affordable," says Robert Wood, Chief UK Economist at Pantheon Macroeconomics. "Money would anyway be better spent on firms more exposed to spot energy."

"The last thing we need now is large fiscal interventions from the UK and other gov’ts to try and hold down the 'cost of living'. Leave the BoE to control inflation with interest rates & use fiscal policy to manage public spending/tax in line with sound economic principles," says economist Andrew Sentance, a former member of the Bank of England's MPC.

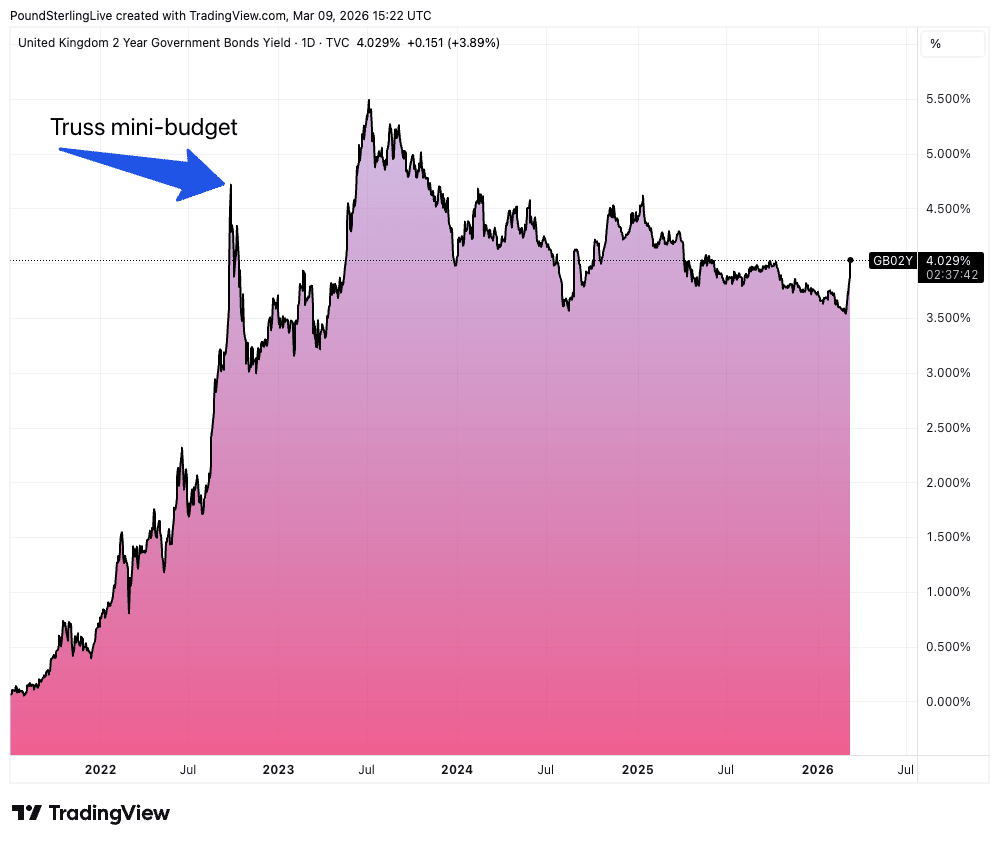

Above: The interest rate (yield) on UK two-year bonds.

UK two-year bond yields - which are closely aligned with Bank of England rate expectations - rose to 4.060% on Monday, the highest level since May 2025.

The rise comes as investors no longer see the Bank of England cutting interest rates in 2026 and see a 70% chance that the next move will be a hike.

The longer-dated end of the bond market, which also incorporates investor calculations on how uniquely risky a country's debt is, is also climbing.

The 30-year bond yield is up at 5.33% and the 10-year at 4.7%, a level last seen in October.

The UK also pays interest on much of its borrowings according to what the RPI inflation rate is doing. Analysis from Lloyds Bank shows that the sensitivity of debt-interest payments on index-linked gilts is £9.6bn per 1ppt on RPI inflation in 2029-30.

Therefore, a ~2.5ppt shock to inflation would be enough to wipe out the government’s projected £23.6BN 'headroom' it gave itself via various tax raising measures in November's budget.

"With higher energy prices causing doubts about the case for further rate cuts, and exposing the constraints on fiscal space to respond, other markets may well have to factor in some risk of potentially higher short and longer term market rates," says a note released Monday by Lloyds Bank.

For the pound, the memories of 2022 will act as a significant headwind.