Good news for Chancellor Reeves as retail sales and public sector borrowing data are materially better than expected. Picture by Kirsty O'Connor / Treasury.

The British pound holds steady against the euro but cedes more ground to the dollar.

Pound sterling was mixed in the wake of consensus-beating retail sales and some good news on the UK public finances that should go some way to ease concerns about the sustainability of UK debt.

Retail sales for January rose 1.8% y/y, which beat estimates for 0.2%, and marked a significant uplift on December's 0.4%.

The data is all the more surprising as it covers a very wet month in the UK that tends to dampen retail activity.

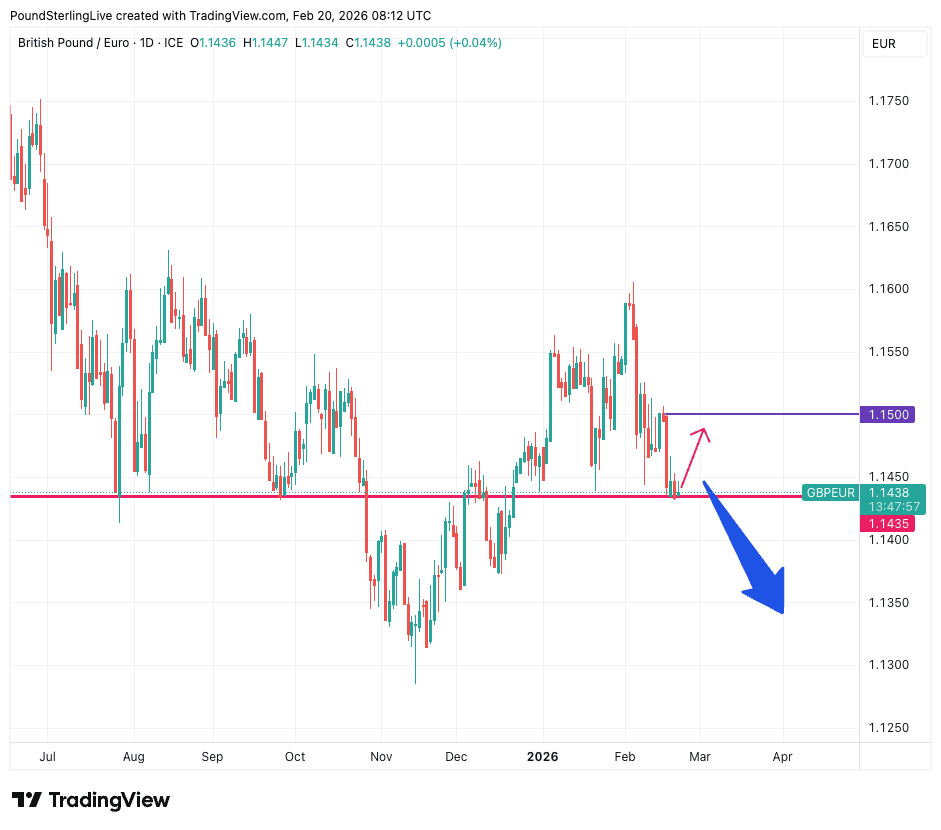

The pound to euro exchange rate trades at 1.1439, just above the important support level at 1.1435, while the pound to dollar exchange rate edges lower to 1.3446.

The implications of the retail sales figures are that the Bank of England needn't rush to cut rates, but in isolation they're not enough to shift the view that the Bank will lower rates next month on account of a deteriorating labour market.

Hence, the limited GBP reaction on the day. Yet, these are undoubtedly good data that stabilise the pound after a volatile week and firm up the currency's outlook.

On this count, it's actually in the public sector borrowing numbers where the day's biggest surprise is to be found.

The government reported a £30N surplus in January, exceeding the 23BN figure expected. January is a rare surplus month for the finances owing to the self-assessment payment deadline.

It means fiscal year-to-date borrowing is £8.3BN lower than forecast with just February and March numbers to come.

Above: GBP/EUR risks are heavily skewed lower, but some good data can help trigger a relief rally above 1.1435.

Consensus projections for the next four quarters, compiled from leading investment banks.

Access the full forecast →

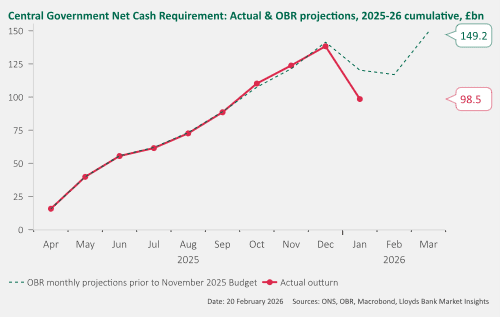

Often a flashpoint for the pound, the country's finances were shown to be in a much better position than expected in January. "For gilt market participants looking ahead to the Spring Statement on 3 March this is the more newsworthy release," says a morning note from Lloyds Bank covering the release.

"On inspection, whilst tax receipts did surprise to the upside that wasn’t the main story. Really more of the news was from government spending being lower than expected," says Lloyds Bank, explaining:

"Where this report was remarkable was on the cash requirement (CGNCR) and this is important because this is the variable that drives calculations for the gilt remit. CGNCR so far for 2025-26 is now reported as being £21.8bn less than expected."

Image courtesy of Lloyds Bank.

Economists say should this gap persist for the next two months, then the 2025-26 funding programme will have raised almost £22bn more than needed and that this overfund can be used to reduce the funding programme for 2026-27 all else equal.

"Given the noise involved with monthly variations and timing effects, this is likely an over-simplified first take but it is nevertheless a market-friendly outturn in terms of future supply expectations," says Lloyds.

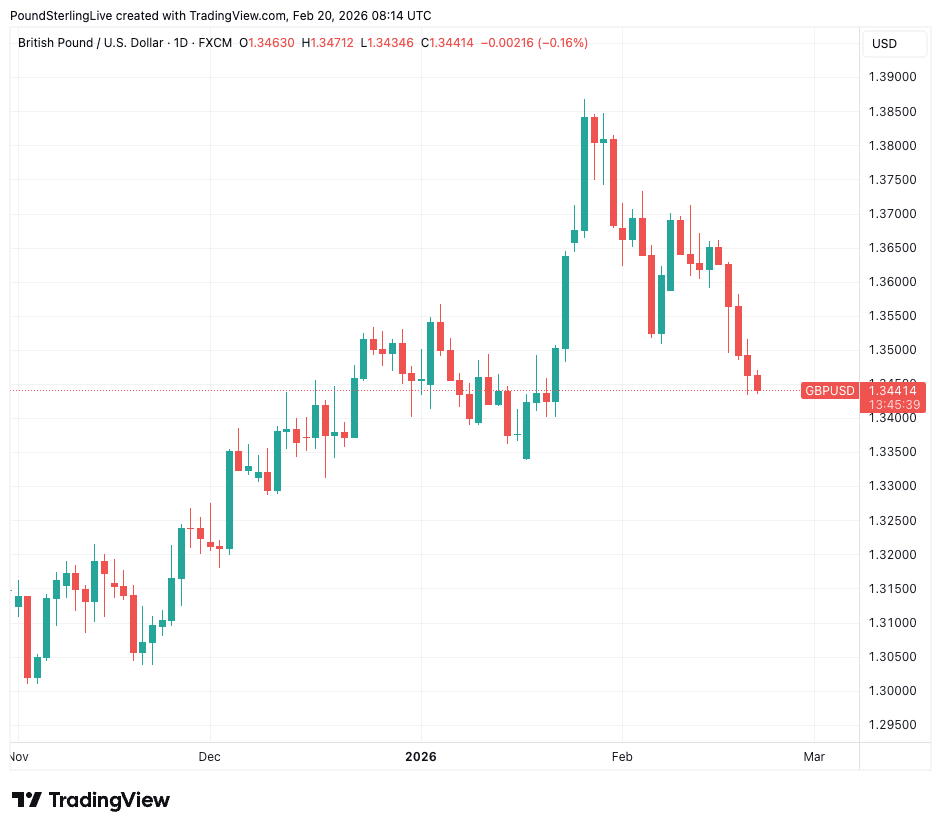

Above: GBP/USD relinquishes its gains for the year on account of a USD comeback.

Turning to the GBP more generally, the USD's recovery is the big theme of the week in FX, with the currency finally taking note of the positives in the U.S. economy.

GBP/USD has relinquished it's 2026 gains on account of a run of above-consensus data and minutes from the Federal Reserve that showed some policy makers would be minded to raise interest rates if the data turns out stronger than expected.

This blows a hole in the view that the dollar is on course for a negative year on account of a Fed that will cut rates more than its peers.

It also raises questions as to whether the consensus USD-negative call made by investment banks for 2026 ended before the year had really got started.