Image © Adobe Images

The UK economy is hard-wired to weaken its currency over the long-term, according to new analysis conducted by HSBC.

HSBC shows that the UK economy is unlikely to command a currency that can rise over a multi-year timeline unless it can shake its addiction to imports, something that leaves the Pound reliant on the money of external investors.

The UK is a net importer meaning it spends more than it earns, which represents a 'core' economic problem for the Pound.

"Having a strong core is also crucially important for currencies. Having a strong and stable source of funding provides a backdrop for less vulnerability and ultimately a good base from which a currency can make gains," says Dominic Bunning, Head of European FX Research.

"For both the EUR and GBP, things are looking increasingly worrying on this front," he explains.

Both the Eurozone and UK face challenging cyclical dynamics, these include weakening growth, higher inflation and constrained monetary policy.

"But the deterioration in both currencies’ core balances is becoming a more concerning medium term threat," says Bunning.

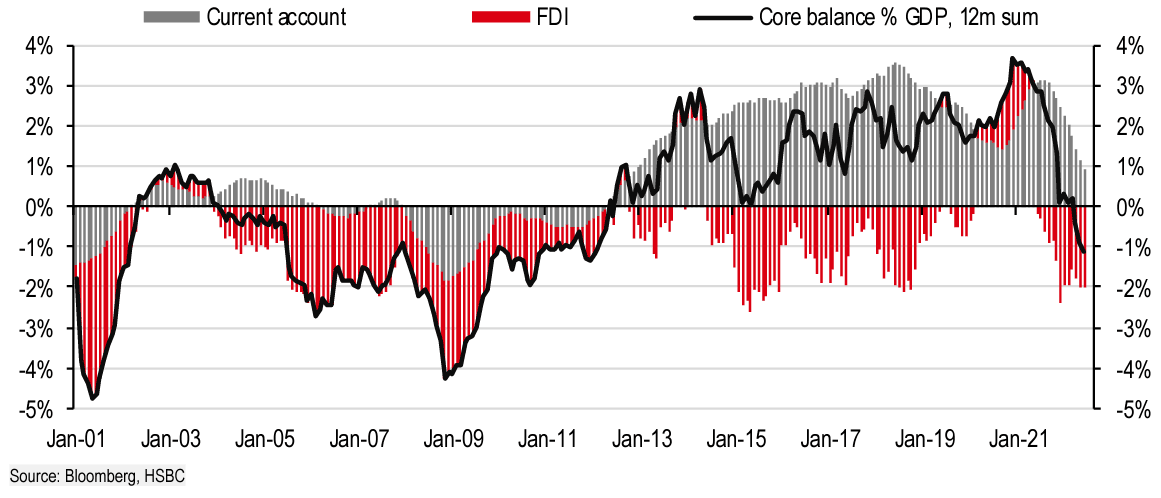

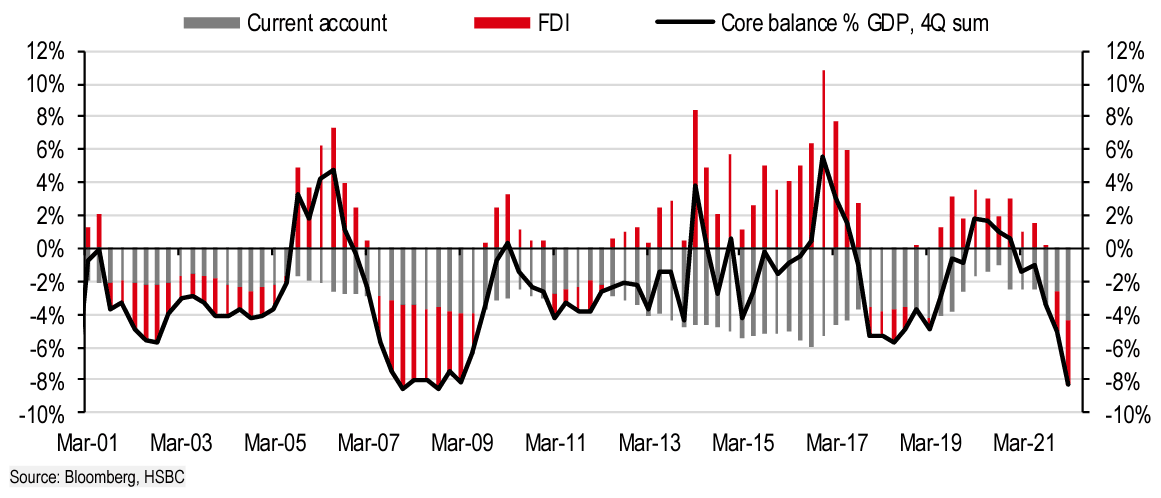

He explains the core balance measures the sum of current account flows and net Foreign Direct Investment (FDI), and is seen as a more stable source of inflows for a currency.

The Australian Dollar is an example of a currency that continues to benefit from its strong core: Australia's trade balance continues to expand as it exports iron ore, coal and natural gas to the global economy.

The UK's current account deficit has meanwhile widened as the UK imports these types of commodities, as well as all sorts of other goods.

The Pound is only able to maintain value if this deficit is funded by other means, usually via the inflow of money from international investors looking to snap up UK assets.

This is a precarious flow for the Pound to rely on, described by former Bank of England Governor Mark Carney as "the kindness of strangers".

But, of late the Eurozone has also started to witness such negative dynamics.

"The Eurozone's core balance has fallen from a surplus of nearly 4% of GDP to a deficit of 1% of GDP in the last 18 months.

As the core balance deteriorated the Euro-Dollar exchange rate has fallen to parity.

Above: "The Eurozone 'core balance' has deteriorated rapidly from a sizeable surplus to a deficit" - HSBC.

The Eurozone has traditionally relied on Germany's export prowess to generate current account surpluses, but this has changed in 2022 as global demand subsidies.

The current account deficit has only grown as the cost of importing fossil fuels and commodities rocketed following Russia's invasion of Ukraine.

But this is a problem that has beset the UK for many years.

Above: "The UK 'core balance' started from a worse position and has worsened even further" - HSBC.

"The UK has seen an even bigger decline from a surplus of 2% of GDP to a deficit of 8% of GDP in the last two years," says Bunning.

The ONS said the UK's underlying current account deficit, excluding precious metals, expanded to £44.2BN, or 7.1% of gross GDP in Quarter 1.

This was largely driven by the country's trade deficit, a hangover of an ongoing addiction to commodity and goods imports and inability to export on a meaningful scale.

Given there is no prospect of this situation turning around for many years, the deficit is likely to remain a constant feature of the UK economy.

All this spells trouble for the Pound.

"These deficits require external financing. This in itself is not an issue, but for both the EUR and GBP, these flows are potentially more volatile and vulnerable to external conditions," says Bunning.

The UK's financial account showed a net inflow in the first quarter of 2022 of £29.6BN, as UK liabilities increased more than assets.

"This suggests that in the near-term there is an asymmetric risk to the downside for both currencies amidst tighter global funding pressures and weakening global risk sentiment," says Bunning.

"These structural imbalances require a gradually weaker currency through time," he adds.

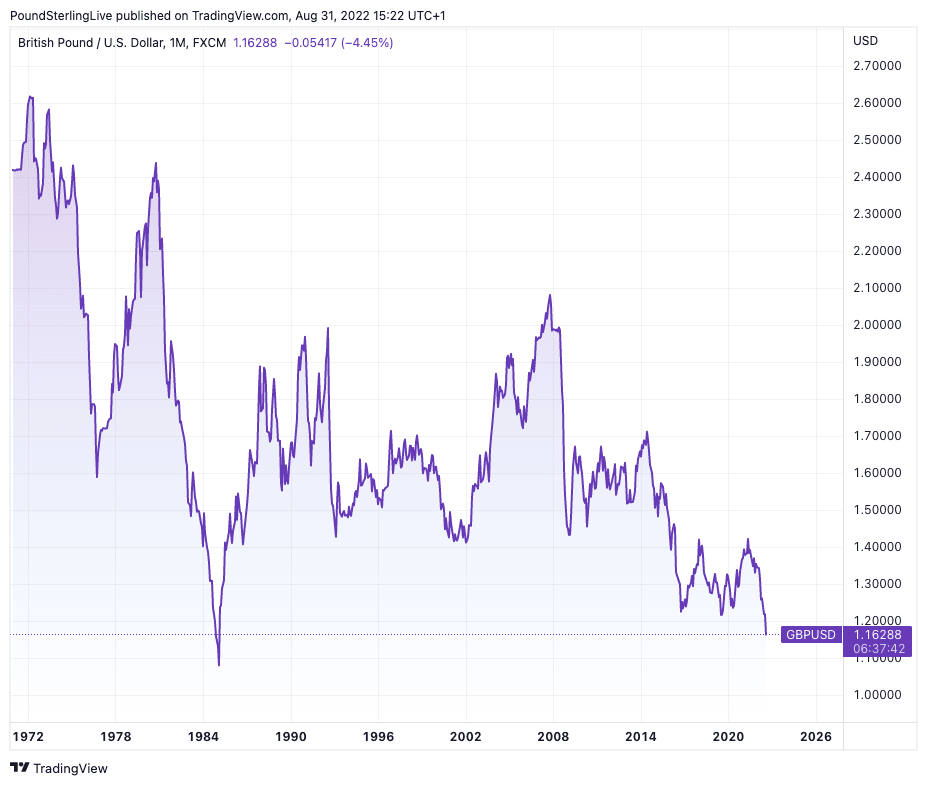

This would help explain why the Pound has ultimately been on a multi-decade trend of decline against the Dollar:

Based on HSBC's findings, this trend of depreciation against the Dollar will ultimately continue and a test of parity, and an eventual move below, will be inevitable over coming years.

"On a longer-term horizon, the weakening of the core balances also suggests that neither currency is especially cheap from a valuation perspective," says Bunning. "An overshoot to the downside may be greater than we have previously envisaged."

Given the Eurozone also faces similar 'core' issues to the UK, the Pound to Euro exchange rate might be more stable longer-term.

However, the Euro might find itself better supported were the Eurozone economy to start firing on all cylinders again.