- GBP & UK economy contrarian candidates for outperformance in 2021.

- On Britain's headstart in vaccinations, China's renaissance, Brexit deal.

- Nomura, Westpac, Credit Suisse, Toscafund & Goldman all eyeing GBP.

© IRStone, Adobe Stock

- GBP/USD spot rate at time of writing: 1.3215

- Bank transfer rate (indicative guide): 1.2854-1.2947

- FX specialist providers (indicative guide): 1.2898-1.3124

- More information on FX specialist rates here

Pound Sterling remains among the worst performers for 2020 and the economy one of the most badly affected by the coronavirus, although if an acrimonious Brexit is avoided this month, both the economy and currency could quickly become a contrarian's contenders for outperformance in 2021.

Britain and Europe remained as far apart as ever on Friday over key issues keeping the two sides from the trade and future relationship agreement that's necessary in order to prevent a default to terms governed by the World Trade Organization and a relationship impeded by Most Favoured Nation tariff rates.

The risk of failure may have grown more likely this week than at any other point in the four year period of ever-extending deadlines, which has been the backdrop for Britain's squabble with Europe over sovereignty and trade terms as it bids to win independence from the bloc.

But if despite its seemingly ebbing prospects, an agreement is reached either in the final hours of 2020 or a time after the December 31 expiry of the transition period that has preserved the trade and other conditions of EU membership until now, both Pound Sterling and the UK economy could both soon become a contrarian's contenders for outperformance in 2021.

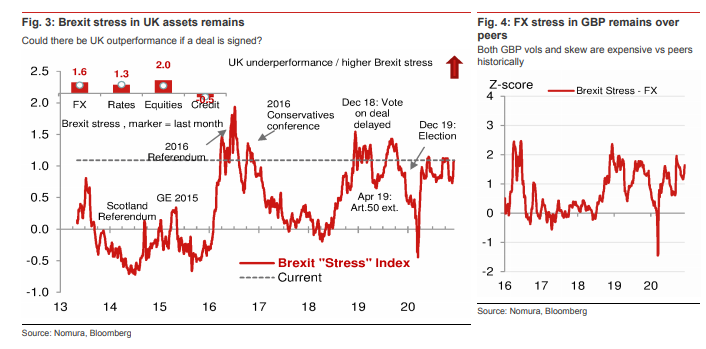

"As we have shown in previous business cycle analysis, GBP tends to outperform in recoveries and underperform in recessions. The underperformance this year due to lockdowns could lead to a complete reversal of that narrative thanks to re-openings giving the UK economy and GBP the most to gain from a vaccine rollout in the G10," says Jordan Rochester, a strategist at Nomura. "We suspect Brexit represents the larger proportion of UK asset price underperformance at this particular juncture, as COVID-19 is a global phenomenon and European peers are in a similar position. Either way, the removal of the hard Brexit tail risk should see Brexit stress fall."

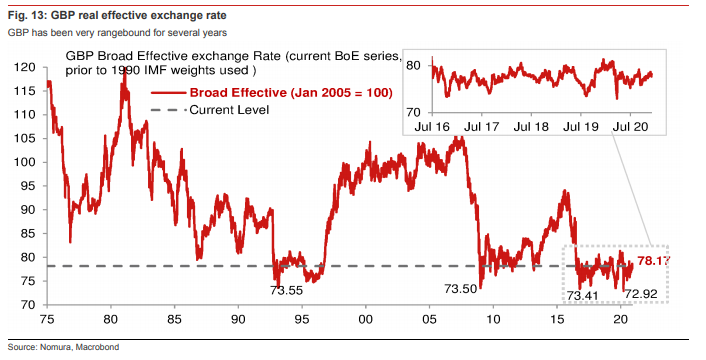

Above: Click for larger images. Nomura's Brexit Stress Index (left), and real-effective-exchange-rate for GBP.

Britain's plight at the hands of the coronavirus has been well documented as the worst of all major industrialised nations since the economy contracted by around a fifth in the second quarter, only for its subsequent rebound to have already lost steam when the second 'lockdown' was imposed in November.

This and persistent uncertainty about the future trade relationship with Brussels has seen the British currency languishing near the bottom of the performance rankings for 2020, with gains over only the oil-linked Norwegian Krone and a U.S. Dollar that is near universally out of favour with investors.

{wbamp-hide start}{wbamp-hide end}{wbamp-show start}{wbamp-show end}

In both cases the Pound has risen barely more than one percent, while the economy is on course for a double-digit annualised contraction that dwarfs anything expected of others elsewhere in Europe and the broader industrialised world. But this month has also been a potential gamechanger for Sterling as well as the UK economy, with Britain having become the first country to began rolling out a coronavirus vaccine, which means both now have a shot at becoming relative outperformers next year.

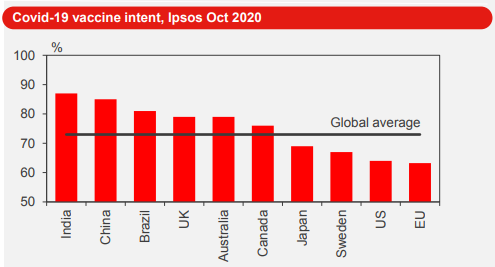

"By year’s end, the US and the UK will have enough doses to vaccinate 6% and 8% of their populations respectively and 25%-30% by March 2021. Thereafter, the UK is in a better position to maintain a strong rollout, with vaccine intent in the UK notably higher than the US," says Richard Franulovich, head of FX strategy at Westpac. "The UK and Canada look better placed in the G10 race, proving additional tailwinds for GBP and CAD next year."

Source: Westpac.

Britain's December approval of the vaccine made by Pfizer and BioNTech has already seen some of society's most vulnerable receive the novel immunisation treatment, while the government has plans and the pre-ordered supplies to provide a quarter of the population with a shot before March next year.

As a result, the remaining coronavirus-related restrictions on activity in place across the country could conceivably be removed within the coming quarters, enabling the economy to recover unconstrained or encumbered by meddlesome and often capacity-limiting impositions on businesses.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

This could have knock-on implications for growth as well as the performance of the Pound in 2021, which have so-far gone underappreciated by the market.

"BoE chief economist Haldane told a parliamentary committee that the spate of vaccine breakthroughs has been “to the positive side” of the central bank’s central assumption. He added that it is “tough to know for sure” if he would have voted in favour of the GBP 150bn rise in extra asset purchases the BoE announced earlier this month had he known that these announcements were imminent. This is a remarkable admission, " says Shahab Jalinoos, head of FX strategy at Credit Suisse. "It suggests that a caucus could rapidly form in favour of more symmetric risks around future interest rate paths than has been the case if both trade talks go well and the UK economy beats expectations for speed of re-opening and recovery, which could then set GBP apart from some other major currencies as a potential 2021 outperformer."

Source: Credit Suisse.

Downbeat views on the UK economic outlook were mainstream in November when the country was placed back into a form of 'lockdown,' which led the average of new forecasts collected by HM Treasury that month to slip from from -10.6% for 2020, to -11%. Meanwhile, the average projection for 2021 also declined, from +5.3% to just +4.8%, meaning that before this week's vaccine announcement the UK economy was expected by the market to recover less than half its losses next year.

In addition, forecasts made by the independent Office for Budget Responsibility (OBR) following HM Treasury's spending review in November pointed to a -11.3% annualised decline in GDP for 2020, and also a recovery of less than half that for next year. But even before the government's vaccine approval some economists saw the OBR and market's views as too pessimistic.

{wbamp-hide start}

GBP/USD Forecasts Q2 2023Period: Q2 2023 Onwards |

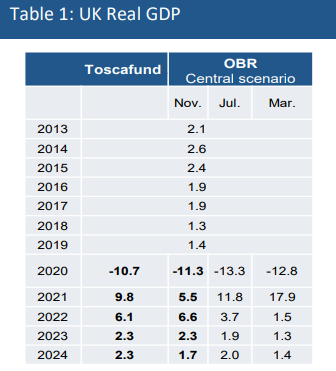

"The OBR has warned UK REAL GDP would not return to its pre-coronavirus-crisis level until 2022Q3," says Dr Savvas Savouri, at Toscafund Asset Management, a London based asset manager for around $4 bn in 2019. "I believe its delayed recovery forecasts suffer from falsis principiis proficisci, founded, that is, on a range of false and missing premises, which collectively make for a worse economic and jobs outlook than we will see in reality."

Toscafund looks for a 2021 recovery to lift GDP by 9.8% that year and a further 6.1% in 2022 before growth tails off to 2.3% in each of the next two years, with the effect that Britain's economy recovers the output lost to the coronavirus-related shutdowns sooner than the OBR and market consensus envisage.

Source: Toscafund Asset Management

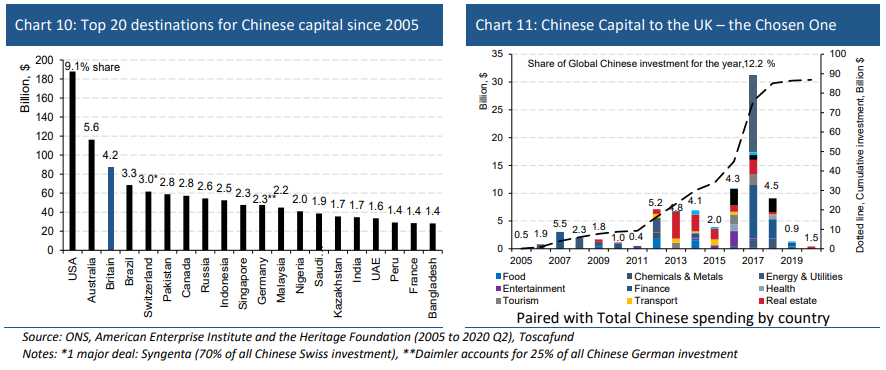

The multi-asset investment firm sees international developments also favouring a stronger UK rebound than has been assumed by the OBR and others, most notably the outperformance of China, which has already recovered the output lost to the coronavirus 'lockdown' in Hubei province back in January.

China's currency has risen almost as sharply this year as any of its major rivals after benefiting not only from a best-in-class GDP rebound but also expectations for the so-far contested U.S. election to install the Democratic Party's Joe Biden into the White House in January. With this comes an improved chance of a less confrontational relationship between the world's two largest economies, after a two-year tariff fight saw international trade disrupted by U.S. duties and retaliatory levies from Beijing.

But expectations of a 2021 world trade recovery have solidified since the U.S. election, while hopes of an eventual removal of American tariffs have also been on the rise. Burgeoning recovery expectations and the resulting demand for western goods and services from domestic China are a potentially positive omen for the UK, which tends to be a large recipient of tourist and student arrivals from the world's second largest economy.

Source: Toscafund Asset Management

"No nation across Europe is leveraged more into this than the UK," Savouri says, citing a 15-year tendency for Chinese capital to favour the Britain over other European countries. "The UK economy entered this fateful year with a CONSIDERABLE store of growth left unfulfilled because of FRUSTRATING uncertainty. Uncertainty related to Brexit – a difficulty since the General Election of 2015 to clearly see the nature of the UK economy in relation to the EU. And uncertainty wrought by THE unfolding PARLIAMENTARY CHAOS – the UK was, after all, governed from the summer of 2017 until December 2019 by an essentially lame-duck Tory Party. This accepted, entering 2021 we will know that Brexit has been a DONE DEAL and a majority Government – led by Johnson, or otherwise – is in place until the next election in late 2024."

Another long and ongoing source of pessimism on the outlook for the UK economy is the widespread expectation that adjusting to a new trade relationship with the EU will have a net-negative impact on growth in the coming year. However, Toscafund instead takes the view that an still-anticipated agreement will unlock pent-up investment demand and boost the economy further. Others also while others see a deal lifting the economy, in addition to the Pound in potentially significant ways.

"Although we look for a notable contraction in Q4 and slow turnaround in Q1, we expect a sharp rebound as covid-sensitive industries begin to normalise in Q2. As a result, we expect real GDP growth of 7% in 2021 and 6.2% in 2022, with the UK economy returning to its pre-covid level in 2022H1. Although these forecasts are similar to the Bank of England’s, they are significantly above consensus," says Sven Jari Stehn, chief European economist at Goldman Sachs. "Given our constructive economic view and the likelihood of a Brexit deal, our markets team sees significant potential upside to UK domestic stocks and Sterling, with [GBP/USD] at 1.44 in twelve months."