- FX market's rewarding more QE, sooner

- Growth expectations are what matter for FX says Nomura

- BoE risks 'Japanification' unless it goes bold early on in crisis

Image © Adobe Stock

The British Pound fell by over a percent against the Euro and 1.3% against the U.S. Dollar last week, with a major culprit behind the move cited as Thursday's Bank of England policy meeting.

The Bank raised quantitative easing by £100BN, an amount that markets were expecting, but it was also said this packet of money would be used to finance the purchase of government and corporate bonds up until year end.

The market was quick to do the maths and took away the message that the Bank would in fact be slowing the pace of quantitative easing and the amounts each intervention would involve.

In short, the Bank's support for the economy will ease over coming weeks and months and could therefore be considered 'hawkish'.

A long-held rule of thumb is that a currency appreciates when a central bank is more hawkish than expected, and falls when the scale of monetary easing is larger and more aggressive than expected.

But, as mentioned, the Pound ended up weaker following the Bank's June event, leaving us to scratching our heads.

According to Jordan Rochester, an analyst at Nomura, the market has now come to favour decisive and generous central bank action, purely because of the support it lends the economy in these covid-addled times.

"What has become clear in G10 FX over both the ECB and the BoE meetings this month – if policy supports growth expectations, that is all what matters and the currency will rally as a result," says Rochester.

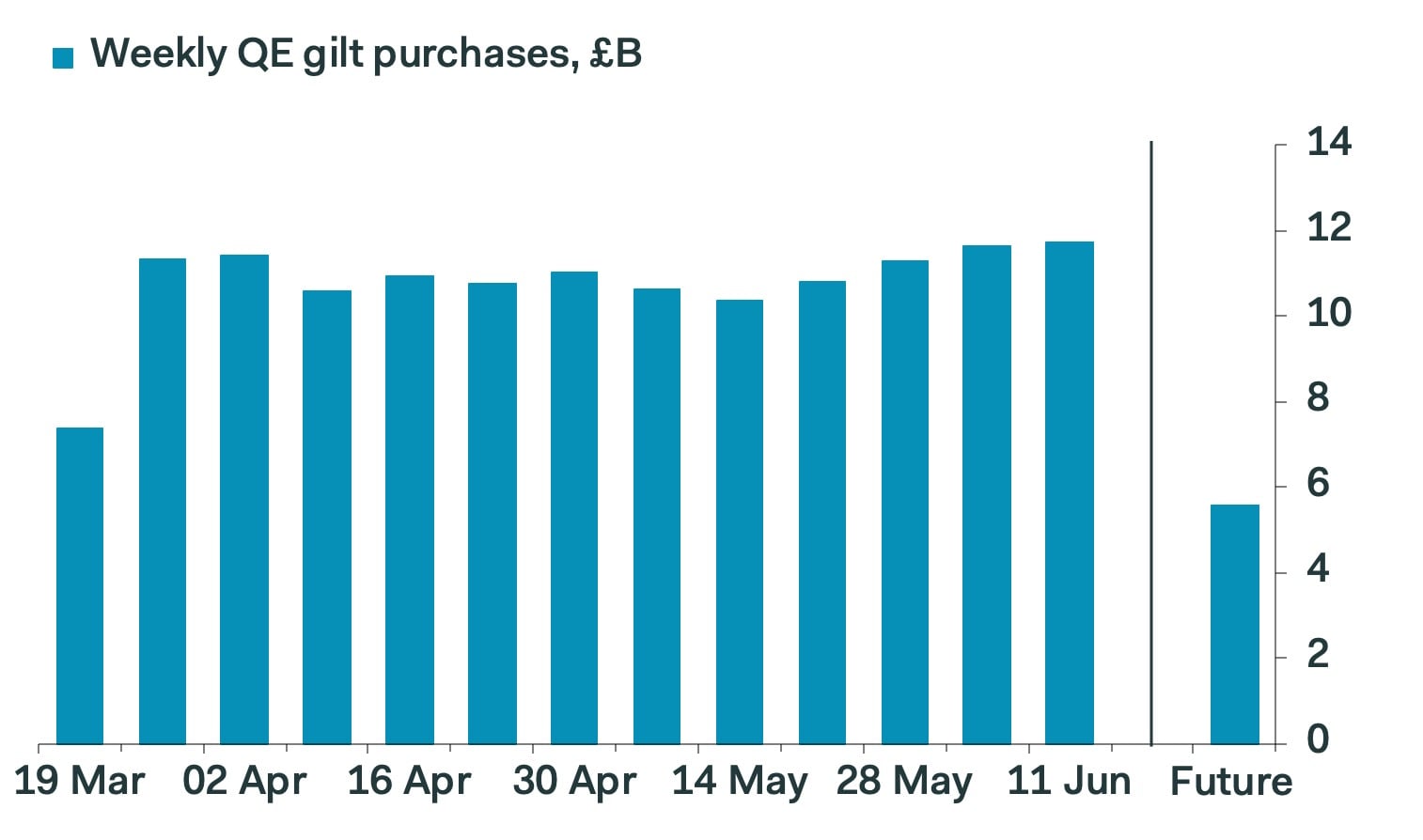

The Bank had bought £150BN worth of UK government bonds (gilts) out of a potential £200BN by June 10 which works out at a spend of around £11.5BN per week plus, excluding the fraction of £10BN in corporate bonds.

The Bank said that the additional increase is enough to go until year-end, which implies reduction to about £6.6BN per week.

In the wake of the event, Sterling lost ground with the Pound-to-Euro exchange rate falling to 1.1125, while the Pound-to-Dollar exchange rate fell to 1.2502.

"Given the immediate market reaction it appears investors were hoping for a little more than the £100bn increase in quantitative easing that has been announced by the Bank of England. Indeed they may have a point in being disappointed by this announcement given the Federal Reserve and European Central Bank are both guiding the market that they will do whatever it takes to keep the economy afloat," says Hinesh Patel, portfolio manager at Quilter Investors.

Image courtesy of Pantheon Macroeconomics

The market's new approach to currencies and central bank easing is reinforced by the Euro's recent run of strength which came in the face of relatively generous fresh stimulus efforts at the European Central Bank.

"For the ECB earlier this month it was a success story of higher QE and a rallying currency for good reasons of higher growth expectations. But for the Bank of England this week the message was muddied and suggested the “worst was behind us” leading to the market expectations of further stimulus beyond the GBP100bn announced yesterday to be disappointing," says Rochester.

Robert Wood, UK Economist at Bank of America Securities says there is another angle as to why market's favour aggressive easing, whereas in the past this might not have been the case.

"Standard economics says the best way to avoid QE becoming semi-permanent would be to ease even more aggressively now. The harder the BoE presses the accelerator the faster it will get to the destination; the faster spare capacity is eliminated the sooner policy can be normalised. What would in our view lock in expectations of permanent QE is a 'Japanification' scenario that potentially comes from too little stimulus," says Wood.

Therefore, if a central bank were to engage in a series of small, but regular, bouts of quantitative easing, the market would take a view that it is becoming an increasingly permanent source of support for the economy.

"Talking about policy tightening now or 'reloading policy' - reducing QE to be able to increase it later - just makes the monetary policy problem worse. The key question for the Monetary Policy Committee, in our view, is how the central bank can ease more, not how it can tighten," says Wood.

For Sterling bulls, more now appears to be better when it comes to the Bank of England aid.