Image © European Central Bank

- Technical indicators argue trend may now be down

- Strong data from US and safe-haven flows supportive of USD

- Upside risk for Euro in the week ahead, however, from the ECB meeting; Dollar sees release of inflation data

The Dollar made a come back last week after exceptionally strong US data and the threat of the trade war escalating combined to support the currency. Key highlights were manufacturing ISM rising above 60 and payrolls hitting 201k in August.

The Euro, on the other hand, weakened after German trade and manufacturing numbers disappointed.

The difference in performance was reflected in the exchange rate, which may well have reversed trend on a short-term vista.

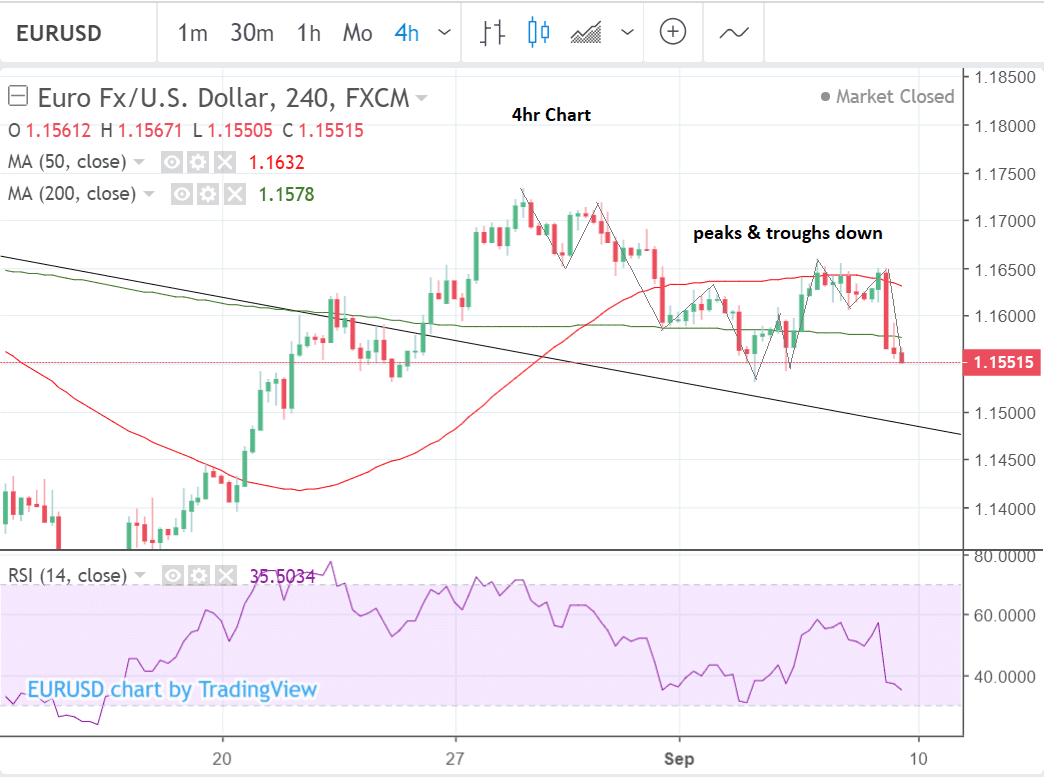

The 4hr chart is the timeframe usually reserved for determining the short-term trend and looking at EUR/USD we note how a case could be made for the trend now being down on this timeframe, after the progress of peaks and troughs, of higher highs and higher lows, appeared to reverse and start moving down following the August 28 peak.

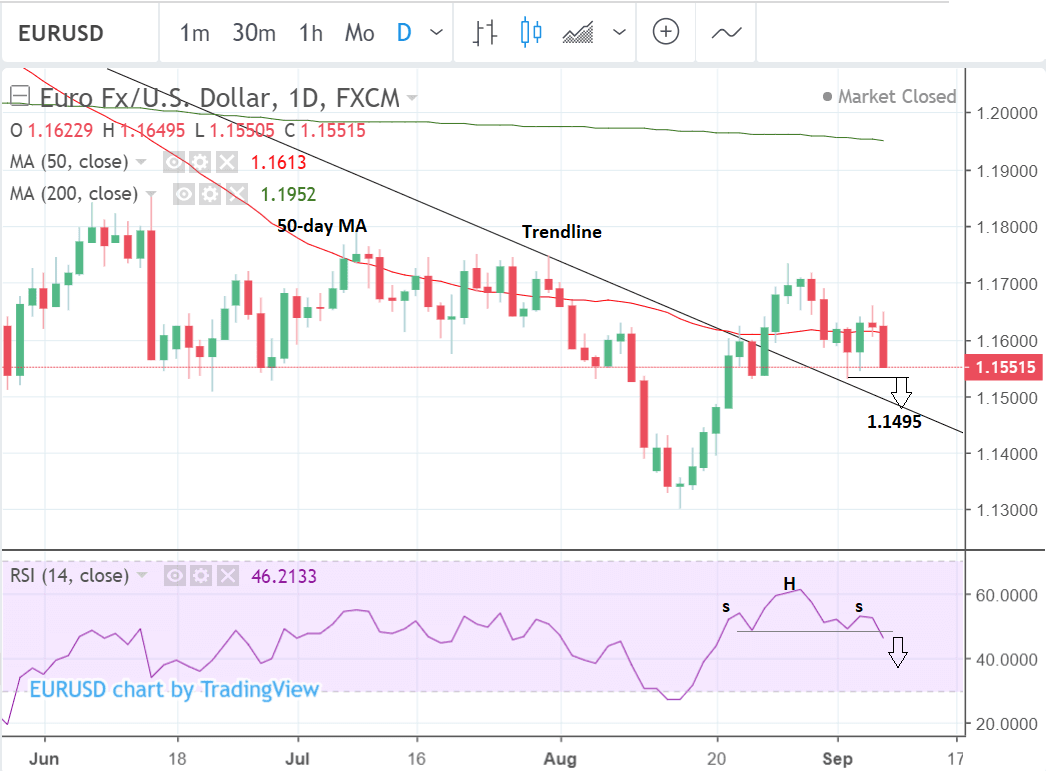

This is backed up by evidence from the daily chart which shows a possible bearish head and shoulders topping pattern may have formed on the RSI indicator in the bottom panel. The RSI may have broken below the neckline of the pattern too providing confirmation of the start of a move down equal to the height of the pattern. This would suggest deeper declines for the underlying exchange rate too.

The pair has also broken back below the 50-day moving average after breaking above the MA on the way up - this too is a bearish sign.

EUR/USD is still trading above the trendline it broke through on August 24 but this and the stronger prior trend up are the only bullish signs for the pair from a technical perspective.

A break below the 1.1530 lows would confirm deeper declines to the next downside target at 1.1495, where the old trendline sits and is expected to provide support to the exchange rate at that level.

Advertisement

Get up to 5% more foreign exchange for international payments by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here

The Euro: What to Watch

The main event for the Euro in the week ahead is the conclusion of the policy meeting of the European Central Bank (ECB) on Thursday at 12.45 B.S.T.

In June the ECB signalled it would be tapering its quantitative easing (QE) programme with a view to to ending QE altogether by the end of 2018 and many analysts see a good chance that it will reduce the volume of monthly asset purchases (probably from 30bn to 15bn) at the meeting this Thursday.

If it does it should provide the Euro with a boost, as it will confirm the ECB's roadmap to normalisation; if it doesn't it could weigh on the single currency.

A recent run of poor data - especially from Germany - and a surprise fall in inflation, coupled with increased political risk from Italy are major headwinds which threaten to derail the ECB's plans to curtail QE, and a taper on Thursday is not a 'done deal'.

Most major bank analysts, however, still appear to expect the ECB to remain on track to taper and not all recent data out of Europe has been poor, as evinced by the Eurozone PMI for August which in the end met expectations on their final revision.

Analysts at Wells Fargo don't see a change in policy happening at the September meeting.

"In our view, the ECB is unlikely to provide many new signals at its policy announcement next week, particularly given ongoing concerns around Italy and global trade. Instead, we believe it is more important to monitor the incoming European data flow for clues on whether the ECB might deviate from the policy schedule it laid out at its June announcement," say Wells Fargo.

The other main release for the Euro is ZEW economic sentiment in August, out at 10.00 on Tuesday.

The ZEW index showed a fall to -11.1 in July, the third negative reading in a row - an unusual run of bad data for the indicator.

The index is based on the balance of survey responses from 350 German financial experts and is considered a fairly reliable forward indicator for broader economic growth int eh region, so another negative reading could weigh on the Euro.

The Dollar: What to Watch

Trade war related safe-haven flows are expected to be the main driver of the US Dollar in the week ahead.

The US government has still not decided whether it is going to raise anymore tariffs on Chinese imports but an announcement on the issue is imminent.

If it decides to raise tariffs on more goods, as is feared could happen, it could benefit the Dollar which should rise on increased safe-haven demand.

The China-US trade conflict is not the only external driver that could send more inflows into the US - a further factor could be more general emerging market (EM) risk as currency stresses simmer in the likes of Brazil, South Africa, Turkey and Argentina.

If these stresses extend, the US Dollar will likely benefit from increased safe-haven flows.

More strong data will only likely add to demand for dollars - investors are increasingly looking to the west in their search for a combination of reliability and yield and the US now offers both ever since growth started to motor ahead in Q2.

Further strong data in the week ahead will only tip the balance more in the US's favour leading to more EM into US flows, and increasing demand for the US Dollar in the process.

Inflation data on Thursday is expected to be a key metric in the week ahead as it shapes Federal reserve policy response and a higher reading makes it more likely the Fed will continue to aggressively hike rates. Current mean forecasts are for broad inflation to dip to 2.8% in August from 2.9% in July and core to remain unchanged at 2.4%, when results are released at 13.30 B.S.T.

Friday is likely to see the biggest Dollar movers, however, as retail sales numbers, industrial production and Michigan sentiment data are released.

Retail sales are forecast to show a 0.4% rise in August compared to July when it is released at 13.30, and core retail sales a 0.5% rise.

Industrial production is expected to show a 0.3% increase when it comes out at 14.15, and Michigan sentiment to increase to 96.6 when it comes out at 15.00.

Advertisement

Get up to 5% more foreign exchange for international payments by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here