- Technical studies suggest a solid support level has formed in the mid-1.15s

- Watch survey data out of the Eurozone this week for guidance on the Euro

- Employment and manufacturing numbers dominate the Dollar's week ahead

Image © European Central Bank

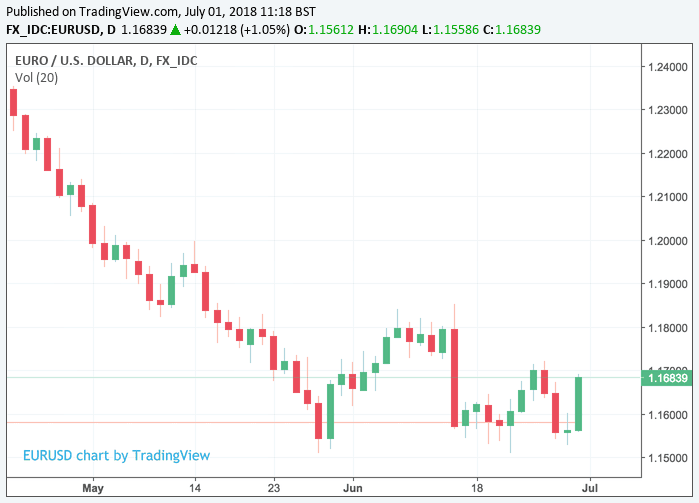

The EUR/USD exchange rate put in a strong rally on the final day of June with the market closing at 1.1683 having been as low as 1.1558 earlier in the day.

The recovery from this level is significant as it confirms the existence of a solid level of support in the 1.15-1.1550 area below which the market appears reluctant to move.

Therefore, we would expect any weakness in the coming week to find support at these levels.

However, the bias we hold is for gains to be eked out as the momentum following Friday's move should offer further help to the Euro in the short-term.

"EUR/USD is firmer but still range bound. We note that shorter term price signals

are modestly constructive above 1.1620," says Shaun Osborne with Scotiabank who feels the high close on the day and the week add to near-term upside pressures.

According to Osborne, Friday's high close forms the third leg of a “morning star” bull reversal on the daily chart – "reaffirming strong support at 1.1500/10 after last week’s key reversal day."

If the exchange rate is indeed entering a short-term uptrend it could rise towards the first major resistance level at 1.1840.

Advertisement

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.

Economic Data and Events to Watch for the Euro

The week ahead in Europe sees a steady stream of economic data hit the wires each day, ranging from the latest IHS Markit PMI surveys of the bloc's various manufacturing and services sectors to unemployment figures for the month of May. However, all are relatively minor releases that will have only limited impact on expectations for economic growth, monetary policy and the Euro.

June's IHS Markit PMI survey of the Eurozone manufacturing industry is the most prominent release in the calendar for Monday, with economics looking for the index to hold steady at 55.0, in line with the number produced by the initial "flash" estimate produced in the middle of the month.

Tuesday markets will focus on Eurostat's estimate of bloc-wide unemployment for May, which is forecast to hold steady at 8.5% for the month. And Wednesday markets will look toward the IHS Markit Services PMI for the Eurozone, with consensus suggesting this too will hold steady at the 55.0 indicated by the flash release two weeks ago.

Both PMI indices have recently given back around half of the 12 month gains they were sat on back in January and February but are still nestled comfortably above the 50.0 no change level, which suggests the Eurozone economy is still growing at a decent, albeit reduced, rate.

Thursday, financial markets will focus on the Destatis estimate of German factory orders for the month of May, due out at 07:00 am London time. Economists are looking for industrial orders to have risen by 1.1% for the month, marking only a partial reversal of the -2.5% fall seen in April. German factory orders also fell by 1.1% in March and by 3.9% in January. German industrial production data for May will be released Friday at 07:00 also, with markets looking for output to have risen by 0.3% after a -1% fall in April.

Economic Data and Events to Watch for the US Dollar

The week ahead in the US promises another action-packed period for currency traders, with the latest ISM Manufacturing Index reading and the June nonfarm payrolls report the main events of note.

Monday markets will watch the ISM Manufacturing Index for a steer on momentum within the US manufacturing sector. Consensus suggests the index will decline from 58.7 in May to 58.2 for the recent month, although this will still leave the benchmark of US manufacturing activity sat close to its highest level in nearly a decade.

Thursday markets will look to the ISM Non-Manufacturing Index for a measure of activity in the US services sector, for clues as to the pace of the US expansion. Consensus is for the index to slip from 58.6 in May to 58.3 in June.

Friday the market will focus on the latest US employment figures, with nonfarm payrolls forecast to have risen by 200,000 in June, down from 223,000 in May. The unemployment rate is expected to hold steady at 3.8%.

All of the data released next week will be important for the US Dollar and other international exchange rates as economists are increasingly forecasting that US economic growth could top an annualised rate of 4% for the second-quarter, which would mark a significant out performance of the rest of world economy.

Any data that confirms these bullish views will be sure to have a positive impact on the US Dollar while anything that causes markets to question those projections would deal the greenback a heavy blow given that the Dollar Index has now risen by more than 7% since the middle of April.

Advertisement

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.