-Short-term EUR/USD forecasts cut at BMO Capital Markets.

-BofAML locks in profits on short trade but reiterates bearish target.

-Long-term outlook is bright but "equilibrium" lower than once thought.

© Goroden Kkoff, Adobe Stock

The Euro-to-Dollar rate rose Friday as the greenback eased in the wake of a weeks-long rally, although respite for the exchange rate may be limited if strategists at two major investment banks are right in having slashed their forecasts and reaffirmed earlier bearish bets against it.

Europe's single currency has now lost all of its 2018 gains after the Eurozone economy was shown to have hit a soft patch during the first quarter and since American bond yields broke out to new multi-year highs at the end of April, shocking the US Dollar back into life after more than a year of steep declines.

It is against this backdrop that strategists at BMO Capital Markets have taken an axe to their short-term Euro-to-Dollar rate forecasts, while the FX team at Bank of America Merrill Lynch has locked in some of its profits on what was a bold but incredibly bearish bet against the exchange rate at the time they entered into it back in April.

Above: EUR/USD rate shown at daily intervals.

"Periodic squeezes on long-EURUSD exposures will likely continue to occur," says Stephen Gallo, head of G10 FX strategy at BMO Capital Markets, in a note announcing the bank's latest forecasts for the exchange rate. "EURUSD longs remain impatient due to the carry associated with holding that position."

The soft patch in Eurozone growth this year was not out of sync with events seen elsewhere in the developed world but recent falls in inflation and consequent concerns over whether the European Central Bank will be able to complete an exit from its quantitative easing programme later this year have dented market confidence in the EUR/USD rate.

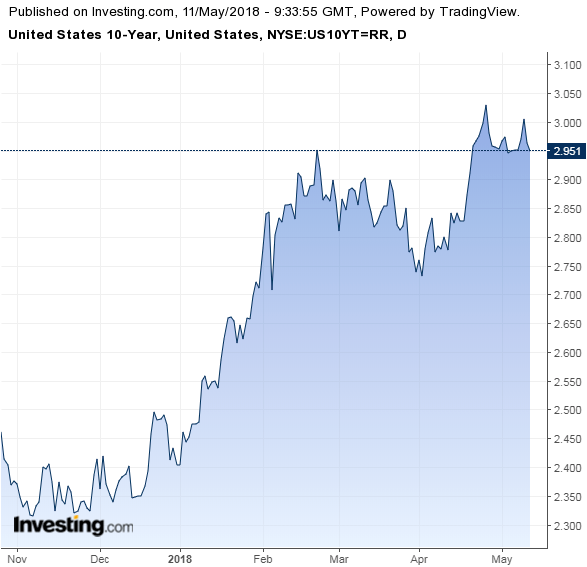

In addition, the sharp rise in US interest rates and bond yields has raised the cost of betting on the exchange rate because traders who sell the Dollar and buy the Euro are forced to pay or forgo the interest rate differential.

Above: US 10 Year Government Bond Yield.

This combined with uncertainty over the short-term outlook for the Euro have seen earlier speculative "long positions" closed out during recent weeks, compounding downside pressure on the exchange rate.

As a result the BMO FX team have cut their one, three and six month targets for the currency pair, with the latest set of projections envisaging that the EUR/USD rate hovers close to 1.18 this month before rising steadily to 1.21 and 1.25 over three and six months. These are downgrades from February targets of 1.24, 1.25 and 1.26 respectively, although they still imply that the worst is now over for the Euro.

"Given structural factors, there is little that the ECB can do to push underlying inflation higher but higher oil prices may do the job. Low rates are feeding political tension in some parts of the bloc. We expect a summer shift in the ECB’s language confirming QE won’t continue in 2019 at the current pace," Gallo adds.

Gallo and the BMO FX team are also still bullish in their longer term EUR/USD outlook, forecasting the exchange rate will rise as high as 1.30 over a 12 month horizon. However, not everybody is on board with this thinking. In fact, strategists at Bank of America are still betting the Euro reaches fresh lows against the Dollar during the weeks and months ahead.

Above: EUR/USD rate shown at weekly intervals.

"Historical correlations with data were already supportive of a stronger USD in Q1. However, the market was expecting Eurozone data to improve in Q2. This is not happening. As the USD strengthens, short positions are getting squeezed," says Athanasios Vamvakidis, an FX strategist at Bank of America Merrill Lynch. "This week, we lowered our stop loss in our short EURUSD trade to 1.21 from 1.26, keeping our target to 1.15."

Vamvakidis and the BAML team bet against the EUR/USD rate in mid-April, going short at the 1.2378 level and targetting a fall to 1.15 before the end of June, with an original stop loss set at 1.26. They've now lowered this stop loss to lock in some of their profits but are still forecasting a decline to 1.15 over the coming weeks.

Much like Gallo at BMO, Vamvakidis also says the EUR/USD will rise steadily over the rest of the year, just not as far. The BAML target for the exchange rate at year-end is 1.25.

"The key risk to our bullish USD call at this point is central bank USD selling. Our proprietary flows show persistent official sector USD selling this year, which has actually accelerated during the recent USD rally. Although such flows could limit USD appreciation, they could also allow the USD to rally more if they were to stops," Vamvakidis adds.

These forecast and trade adjustments come hard on the heels of a separate research report from BAML that argued that "fair value" for the EUR/USD rate over the longer term may actually be much lower than the market thinks it is.

Above: EUR/USD rate shown at monthly intervals

Currently, the consensus forecast for the EUR/USD rate is for it to reach 1.28 by the end of 2018 and 1.30 in 2018. Meanwhile the prices of FX forwards, which are financial derivatives that enable companies and consumers to lock in exchange rates years in advance, place the EUR/USD rate respectively at 1.39 and 1.52 in five and 10 years time.

Vamvakidis says this suggest the market sees "fair value" for the exchange rate as being a long way above current market rates, which he also says is wrong.

"Looking at the EUR real effective exchange rate, it is very close to its historical average. This is also the case for the USD real effective exchange rate. This suggests the EURUSD equilibrium is unlikely to be far from the current EURUSD level. Otherwise, the USD will be much weaker than its historical average, while the EUR will by much stronger than its historical average," the strategist writes.

While there are grounds for thinking the EUR/USD rate and its "equilibrium" will still rise over time, the current consenus implies the exchange rate will return to the levels it was at before the ECB began its QE and negative interest rate policies, while overlooking the way in which the world has changed during the last four years or more.

The crucial oversight is that before the ECB first began it's QE programme, the Federal Reserve was also running its own stimulus programme and American interest rates were close to zero.

Since that time, the Fed has ceased its intervention in American bond markets and the Federal Funds rate has risen so that it now stands at 1.75%, while some Eurozone interest rates are still deep in negative territory and the main refinancing rate still sits at zero. This is a game changer when it comes to currency valuation.

Advertisement

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.