The European Central Bank (ECB) is gearing up to end its quantitative easing (QE) programme and when it does the Euro to Dollar exchange rate should rise by 4% suggests analyst Petr Krpata at ING Bank.

The call comes just days before the ECB's June policy meeting at which the latest set of forecasts and guidance for the Eurozone's monetary system are due to be laid out.

The Euro has rallied with gusto over recent weeks in anticipation of some change in stance and we believe there is the slight chance of disappointment which could hurt the Euro.

However, Krpata has his eyes on the remainder of 2017.

The ECB’s QE policy - also known officially as the asset purchase programme - has kept the Euro weak by flooding the market with easy money and therefore diluting individual unit value, and by keeping bond yields low due to extensive bond buying by Central Bank.

When the price of bonds rise which is what happens under QE, yields fall, because the bond holder has paid more than the original value, which is what the holder gets back once the bond reaches maturity.

Rising – not falling - yields are more attractive to foreign investors, so by capping them via QE, the central bank reduces one source of currency demand.

QE also forces the central bank to keep base lending rates low which cuts down a further source of demand for the currency – form carry traders seeking to profit from interest rate arbitrage.

Carry traders borrow in a cheap currency to buy a currency with higher interest rate.

Due to persistently low rates the Euro has become a Carry funding currency, which is borrowed by traders to buy higher interest currencies.

But borrowing to sell keeps the Euro cheap.

Much of these dampening factors, however, will begin to ease if (and when) the ECB switches off QE.

According to Krpata the Euro will rise another 4% during the dismantling of QE, up to a target at roughly 1.15, assuming no major volatility from the Dollar side of the pair.

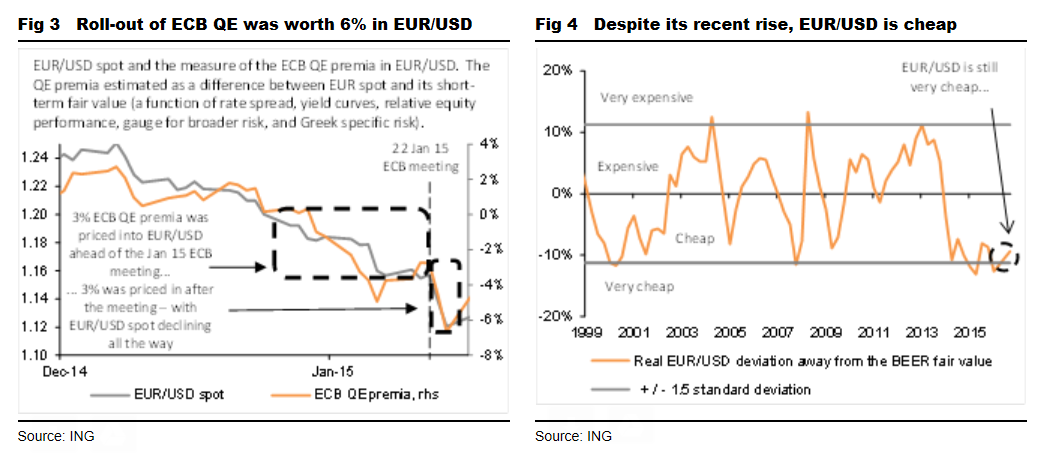

This is calculated by estimating the amount the pair lost when QE was first brought in in January 2015.

“Back in 1Q15, we estimated that ECB QE was worth around 6% in EUR/USD (lower),” says Krpata.

Breaking this down he says that the 6% estimate consists of a 3% QE premia priced into EUR/USD ahead of the 22 Jan 2015 QE announcement; and the post announcement 3% fall in the cross.

Its logical that if the pair lost 6.0% when QE was brought in it will gain the same amount when it is removed.

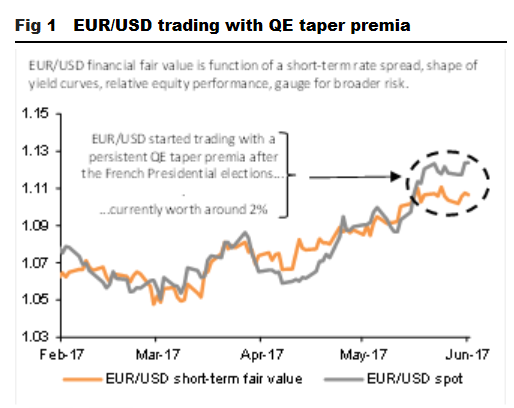

Krpata says that 2% has already been priced in, following the French Presidential election, when EUR/USD rose to 2% above fair value as determined by short-term interest rate differentials.

ING estimate that the market is currently pricing around 2% worth of ECB QE taper premia into EUR/USD.

This is depicted in the below graphic which shows EUR/USD spot persistently trading above its short-term fair financial value.

"When such deviations become persistent, it suggests that factors other than short-term fundamentals are currently driving the cross – in the case of EUR/USD we judge it is the market expectation of an eventual ECB QE tapering,” says Krpata.

"When such deviations become persistent, it suggests that factors other than short-term fundamentals are currently driving the cross – in the case of EUR/USD we judge it is the market expectation of an eventual ECB QE tapering,” says Krpata.

The remaining 4% is forecast to be priced in to EUR/USD from Thursday, June 08, when the ECB is expected to make its first steps towards ‘tapering’ QE.

ING don’t expect the undervalued EUR/USD to get to or exceed 1.15 overnight. Next week’s June ECB meeting may not be the catalyst for it.

“Rather, the importance of next week’s meeting (and the removal of the easing bias via the omission of ‘lower rates’ outlook) is that it should represent a first cautious step towards policy normalisation,” says Krpata.

ING see more upside to EUR/USD this summer - most likely around or after the ECB’s July meeting - once code words suggesting the eventual QE policy tapering are sent (e.g. an announcement that an internal ECB committee is “tasked” to assess QE taper options).”