The big question for EUR/USD traders as we approach the dying strikes of the year is whether the EUR/USD pair will reach parity or not.

Analysts appear split on the subject.

Those at Morgan Stanley, for example, see more downside and a probable lurch towards the one Euro for one Dollar level; whilst other’s such as Canadian lender CIBC point to underlying support for the Euro which could make it a harder to push it any lower.

Monday's gruesome terrorist attacks have dampened the outlook for the Euro by increasing the chances of a far-right political backlash in Europe and a dismantling of the EU.

The Dollar, meanwhile, was supported by a positive outlook for employment sector, after Janet Yellen said in a speech at Baltimore University that graduates faced very good prospects in the job market.

The Argument for Parity

Morgan Stanley are on the side of those arguing for parity, as they see the Dollar rising on expectations of more Federal Reserve interest rate increases.

“We previously saw USD beginning to rally again in the new year.

"Following the hawkish Fed meeting, we are bringing forward that expected strength and expect USD to rally in line with the themes we have been discussing.

“The revising up of the 2017 dots and the neutral rate, along with Yellen's pushback on her support for an overheating economy, are all hawkish signs and more reason for the rates market to reprice higher,” says the Bank.

They see the medium-term outlook as USD positive too as Donald Trump’s pro-Dollar policy agenda comes into play.

Higher fiscal stimulus, trade protectionism and repatriation of corporate cash piles from abroad are all likely to drive up demand for and the value of the Dollar.

Contrast this with their analysis of the Euro, which they see weakening due to “an accommodative ECB,” and you have all the ingredients for a plunge to parity.

Resilient Euro

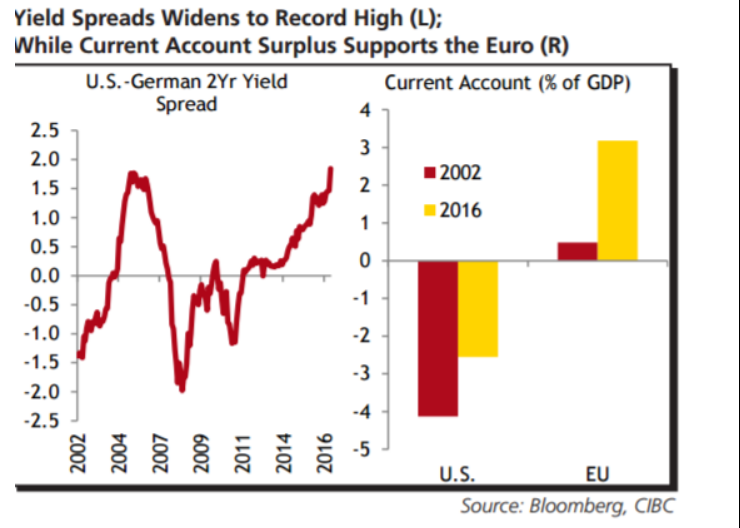

CIBC on the other hand, argue that the Euro is likely to recover in 2017 due to its large Current Account surplus.

“There is a countervailing force which could spoil a New Year’s parity for EURUSD.

“The current account surplus in the Eurozone is not only large, it is much higher as a share of GDP than when the euro traded below parity back in 2002,” argue CIBC.

Divergence in Short-Term Yields

One problem noted by both banks is the growing disparity between US short-term debt yields (2-year and below) and Eurozone short-term debt yields.

Short-term Eurozone bond prices are rising because the ECB has made lower yielding debt – which is generally short-term - eligible for inclusion in its QE programme.

Yields move inversely to bond prices so the ECB’s decision had the effect of pushing down Euro bond yields.

Lower yields generally equal a weaker currency, so with Eurozone yields falling and US yields rising, the Dollar is expected to appreciate versus the Euro.

This is due to higher yields attracting more international capital to a country as higher yields are a sign of raised inflation expectations and therefore higher future interest rates.

International investors like higher interest rates as it means they get more return on their money.

Morgan Stanley see this disparity as critical to their forecast for a lower EUR/USD:

“The ECB allowing purchases of bonds in the 2-year tenor and below the depo rate weakens the EUR by lowering front-end yield differentials – which EURUSD is more sensitive to – and steepening the yield curve which will help bank profitability and encourage the export of capital. “

CIBC also note the yield differential between US and Eurozone 2-year debt reaching a decade high – but they don’t see this as critical since they feel much of Trump’s policy agenda’s impact on the Dollar has already been ‘priced in’.

“With a lot already priced in in terms of US fiscal and monetary policy, the current account surplus in Europe should see the euro gradually regain some recent lost ground in 2017.”

Eurozone Inflation Possibly Set to Rise

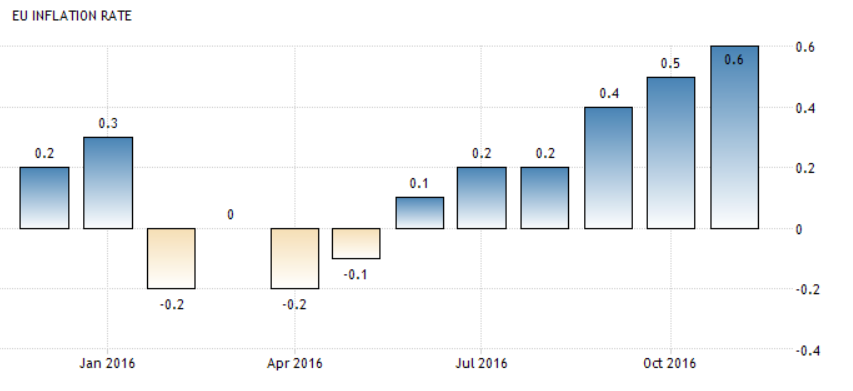

One positive factor for the Euro not mentioned by either bank is the possibility of rising inflation expectations in Euroland.

November inflation in the Eurozone was recently confirmed at 0.6%, from 0.5% in October and 0.4% in September.

It is steadily rising as a result of the, “higher cost of restaurants and cafés and rents and tobacco.”

Interestingly the price of fuel, including heating oil, fell in November despite the price of Crude rising.

This is explained by the large amount of forward buying which takes place in the energy industry which leads to a lag in the impact of base costs.

What seems likely is that higher crude oil prices will filter through and raise fuel costs which will further push up Eurozone inflation in the short and medium-term.

This, in turn, is likely to raise short-term Eurozone bond yields which may be at overstretched extremes currently.

Technical View Suggests No Parity

Technically the pair is struggling to push lower.

Although it has made lows of 1.0350, progress below that has not been possible.

Downside momentum is slowing markedlyThe MACD indicator has not fallen as much as the exchange rate and this has set up a bullish convergence between momentum and price.

The MACD indicator has not fallen as much as the exchange rate and this has set up a bullish convergence between momentum and price.

Such a convergence is a bullish sign for the exchange rate.

Another bullish sign, noted by Commerzbank's Karen Jones is that the TD Countdown indicator has reached a count of 13 and formed a TD Perfected Setup on the EUR/USD daily, meaning the downtrend may now be overstretched, and due a reversal.

Nevertheless, despite this, the trend is still clearly down for now and this apparent contradiction in signals may be resolved by the pair at the very least going sideways for a while.