Although the EUR/USD pair has broken below some key levels and the short-term trend remains down, there are signs it could be exhausted, at least in the short-term.

EUR/USD extended its short-term downtrend following a hawkish Federal Reserve meeting on Wednesday, December 14.

It has seen further pressure at the start of the trading week from the optimistic Dollar-supportive comments of Fed Chair Janet Yellen who said employment prospects for graduates now looked "very good", and a weaker Euro on the back of heightened political tensions in the EU following a spate of Jihadist terrorist attacks in Berlin and Istanbul.

Before the start of the week were more bullish in our outlook as despite the pair being in a concerted downtrend it was showing signs of exhaustion and due a rebound, now, however, we are more balanced in our outlook.

Technical Outlook

The pair broke below both the December 5 lows at 1.0503 and the 1.0460 March lows, and although it looks set to continue, we see signs the downtrend could be a due a correction

The MACD momentum indicator, for example, is converging bullishly with the price.

This means that although price fell to a new low MACD did not, and this non-confirmation, or “convergence” is a bullish sign for the pair.

Commerzbank’s Karen Jones is also sceptical about the strength of the downtrend, referencing indicators which suggest it may be overstretched.

The TD Countdown indicator has reached 13 which is a sign of exhaustion.

The RSI is not confirming the new low like MACD and this convergence is a sign bears' hold could be weakening.

“But also we note the 13 counts on the daily chart and the fact that the daily RSI has not confirmed the new low and we may see some consolidation around this zone,” said Jones.

Bond Flows

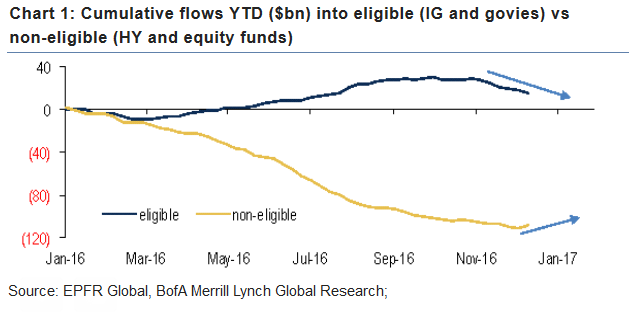

Further supporting the view that the pair may be about to consolidate or recover is research showing that since the European Central Bank (ECB) lowered its monthly QE purchases, from 80 to 60bn, investors have moved out of high grade assets.

This has caused an increase in supply of high grade Eurozone bonds and Eurozone government debt which has been noted by Bank of America Merrill Lynch (BOFAML).

The increased supply has led to a fall in prices and higher yields.

Flows have also increased to higher yielding assets such as stocks, which recorded inflows that were the “highest in 40 weeks,” said BOFAML.

A rise in government bond yields normally increases the value of a currency so this move caused by ECB ‘tapering’ could be supporting the Euro more than analysts had expected.

“Over the past week, investors have moved out of eligible assets, embracing non-eligible ones. high grade credit and government bond funds have been hit by outflows. Contrariwise, equity and HY funds have recorded inflows,” said BOFAML.

The chart below shows how the ECB’s decision to ‘taper’ asset purchases of ‘eligible’ debt may have begun a change in trend for demand for the two sets of assets.

This change in trend, if it holds, may signal a rise in Eurozone sovereign bond yields which would be supportive for the Euro.

As a by-product it might also be supportive of Eurozone stocks.

Data in the week ahead for the Euro

From a data perspective, the main event for the Euro in the week ahead is the German Ifo Business Climate Index, which is released on Monday, December 19 at 09.00 (GMT).

The Ifo is a survey of a cross-section of business people and is used to assess the medium-term outlook for the business climate, it is considered an accurate forward indicator for the economy.

Data in the week ahead for the Dollar

For the Dollar, the week starts with Existing Home Sales in November, at 15.00 (GMT) on Wednesday, December 21, which is expected to show a 5.5m rise in sales.

Then Crude Oil Inventories are out at 15.30 on the same day.

Thursday, December 22, at 13.30 sees the release of Core Durable Goods Orders, which are expected to show a 0.2% rise in November.

The second estimate of GDP in the third quarter is out at 13.30 on Thursday, December 22, and is expected to show a 3.3% rise quarter-on-quarter.