Image © European Central Bank, reproduced under CC licensing

ECB rate hike and U.S. inflation to set the tone for an under-pressure euro-to-dollar conversion in the coming days.

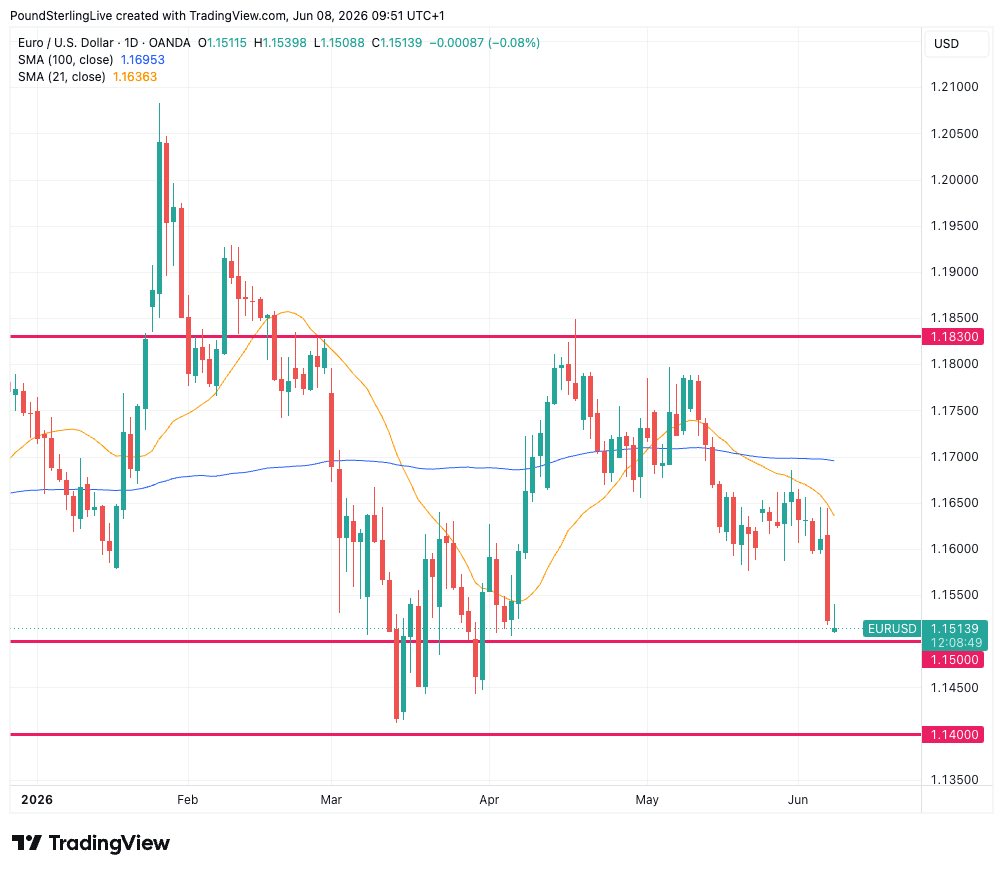

EUR/USD enters the new week with the technical outlook deteriorating after the pair broke below several important support levels and extended the correction from the May highs.

The pair is at 1.1516 on Monday, nursing a chunky 0.76% fall registered on Friday, a move that tips the balance in favour of further downside.

The euro is now trading beneath both its 21-day moving average near 1.1640 and its 100-day moving average near 1.1700, confirming a bearish short-term trend and reinforcing the view that rallies are being sold.

"The euro suffered its sharpest one‑day decline since early March on Friday, falling more than 0.7% against the dollar and finally breaking convincingly below the 1.16 support level - a move that had looked increasingly vulnerable for weeks as negative macro drivers steadily accumulated," says George Vessey, an analyst at Convera.

The move below 1.1600 means a support that acted as a pivot throughout May has been breached, leaving the next line of support at 1.1500 under immediate pressure.

"The pressure on EUR/USD has become broader and more structural. Interest rate differentials have continued to shift back in the dollar’s favour, the eurozone growth backdrop is deteriorating, energy prices remain elevated, and renewed tariff uncertainty is adding another layer of downside risk for Europe’s export‑dependent economy," explains Vessey.

The key level to watch now is 1.1500.

This support line has repeatedly contained declines since March and represents the final major floor before the March-April lows around 1.1400 come into focus.

Although the pair may be vulnerable to a short-term bounce after the recent selloff, any recovery is likely to encounter resistance around 1.1600 initially and then the 21-day moving average at 1.1640.

Euro Week Ahead: ECB's Insurance Rate Hike

The headline event of the week for euro exchange rates will be Thursday's ECB interest rate decision, where an insurance hike of 25 basis points is expected.

That's the ECB saying it's ready to get ahead of inflation, even if it acknowledges the Eurozone's economy has slowed markedly over recent months.

A slowing economy and rising inflation underscore the unenviable position the ECB finds itself in, as raising rates will likely only contribute to that loss of economic momentum. The more cautious members of the Governing Council won't be comfortable hiking, even if they know it's necessary.

These policymakers will be acutely aware that a central bank's most important asset is its credibility, and not doing anything in the face of rising inflation could undermine it.

For this reason, the 'insurance hike' won't necessarily be the start of a 'hawkish' cycle at the ECB, and for the euro outlook that matters, as it suggests the ECB is not minded to follow up with further hikes.

Any subsequent retreat in ECB rate hike expectations in the coming weeks could weigh on the euro further.

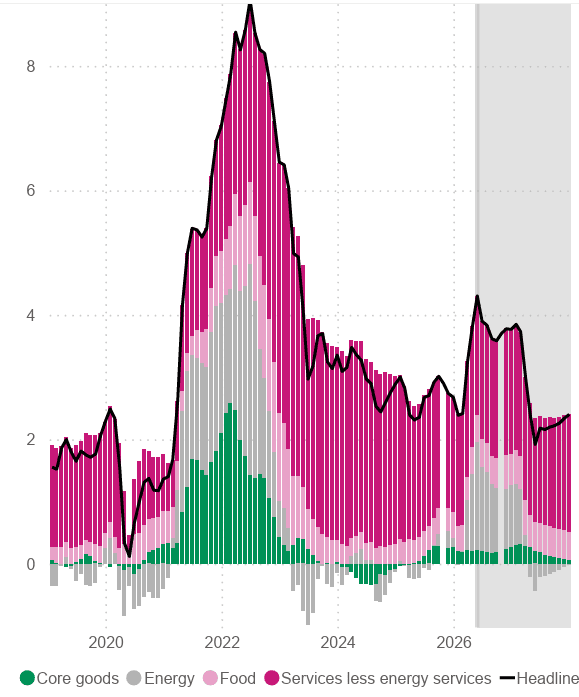

The Dollar's Week Ahead: CPI Could Bake in Fed Rate Hike

The dollar's on a winning streak thanks to a run of above-consensus U.S. data prints, which were topped off by Friday's impressively strong U.S. labour market report that confirmed the economy filled 172K jobs in May.

In response, traders moved to price in approximately 35 basis points of rate hikes from the Fed by year-end, up from 15bp ahead of the report.

That's a significant repricing that explains the dollar's broad advance, which could extend if Wednesday's U.S. inflation print comes in on the hot side.

Headline CPI is expected to have risen 0.3% m/m in May, down from 0.6%, but that'll be enough to help raise the annual rate rise to 4.2% from 3.8%.

Core inflation is seen rising up to 0.5% m/m from 0.4% in April, helping the y/y rise to 2.9% in May from 2.8% previously.

Above: Contributions to headline CPI. Services remain significant, even if a rise in energy costs lifts headline in the short-term.

These data are too hot for the Fed to ignore, and it should, at the very least, abandon its 'dovish' guidance that saw it anticipating a rate cut as the next move.

For the dollar, that's supportive and underpins the downbeat stance we adopt on GBP/USD in the coming days.

However, for the currency to advance further and squeeze euro-dollar lower, the headline figures must beat expectations, which is something economists at Crédit Agricole think will happen.

"We expect US headline CPI to accelerate further in May, to 4.30% YoY, from 3.81% in April and 3.26% in March," says Jean-François Perrin, Senior Inflation Strategist at Crédit Agricole.

"For the Fed, recent inflation data has clearly been an unwelcome development, with headline inflation surging due to the energy driven spike from the Iran war. When combined with signs of stabilisation in the labour market evident in recent jobs data, this has quashed any chance of near-term rate cuts," says Perrin.