Image © European Union, 2025. Photographer: Xavier Lejeune.

Dollar appreciation pressures are building.

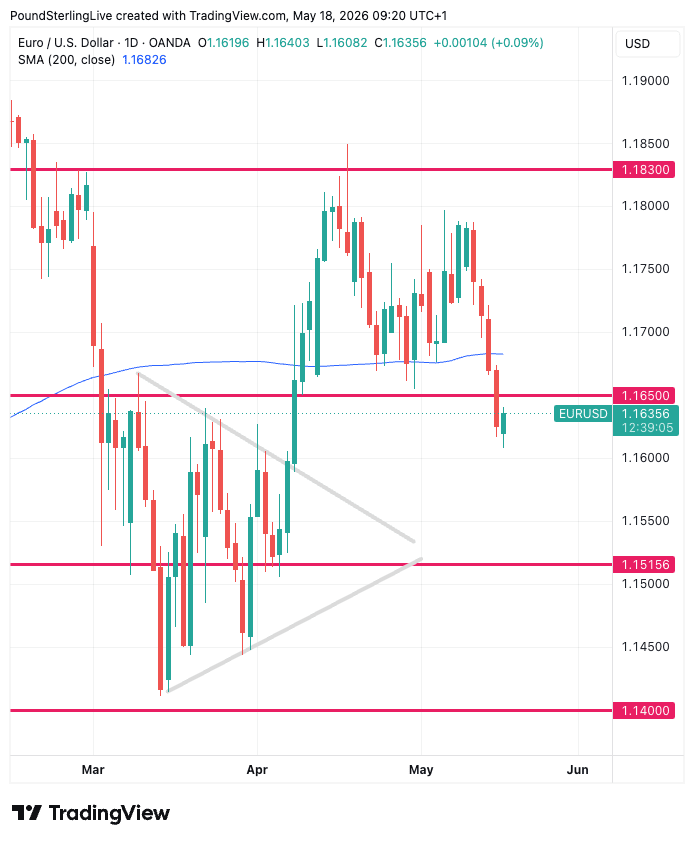

The euro to dollar exchange rate (EUR/USD) faces further downside as USD appreciation pressures build.

Evidence of a shift in market dynamics were clear last week when the pair fell 1.36%, marking the single biggest weekly fall since March.

In the coming week there is the chance that some of those losses are pared as the market catches its breath, but the balance of risks are increasingly tilted towards more near-term pressures.

The dollar’s strength over the last week followed a pair of inflation surprises (CPI and PPI beat expectations handsomely), which helped push U.S. bond yields higher and helped feather demand for dollars.

Above: EUR/USD falls below the 200-day moving average and 1.1650 support, confirming pressures have tilted lower.

The market has bumped up its expectations that the Federal Reserve will need to raise rates in response to these new inflationary pressures.

That's an important narrative shift for a market that has for most of the year expected the USD to suffer as the Fed cuts rates.

"The most interesting regime shift for markets and macro traders will be if the market starts to price in Fed rate hikes. This will light a fire under the USD and FX and bond market volatility," says Brent Donnelly, analyst at Spectra Markets.

"Is it time to get long USD? I think so. I think EURUSD is best: U.S. stocks outperforming and U.S. economy substantially outperforming Europe. And now maybe, just maybe, the market is going to start pricing Fed hikes," he adds.

Meanwhile, geopolitics exacerbates emerging USD demand structures: the Strait of Hormuz remains closed with scant signs of progress towards reopening the Strait. Oil prices are elevated and market nervousness should be enough to keep underlying demand for the USD intact.

At the same time, the U.S. shines as a country that is relatively insulated from Middle East and oil dynamic frictions. After all, it is the world's largest exporter of oil and natural gas, making for increased foreign exchange earnings.

That terms of trade advantage is a natural source of USD support.

And all the time, those energy-importing nations continue to labour under the risk that the latest energy and inflation shock continues in the absence of progress towards the reopening of the crucial Strait of Hormuz.

"We think the clearest risk for a stronger Dollar is if a wider energy shock begins to pressure growth, policy, and prospective returns in other developed countries, particularly Europe," says Kamakshya Trivedi, FX strategist at Goldman Sachs.

Currency strategists at Crédit Agricol say USD 'exceptionalism' is being "revisited" by the markets.

"Global markets seem to have recently woken up to the threat of sticky inflation, its impact on monetary policy and thus the growth outlook around the world," says Valentin Marinov, Head of G10 FX Strategy at Crédit Agricole. "These developments have burnished the appeal of the high-yielding, safe-haven USD as well."

"We expect the King of FX to extend its gains from here," he adds.

Crédit Agricole forecasts euro-dollar at 1.14 by the end of June and 1.12 by the end of September.

Goldman Sachs forecasts 1.14 on a three-month horizon and 1.18 on a six month horizon.

Consensus projections for the next four quarters, compiled from leading investment banks.

Access the full forecast →