Image © Adobe Images

The pound can rebound against the dollar early in the week, but the outlook has certainly shifted in favour of further weakness as the dollar makes a comeback.

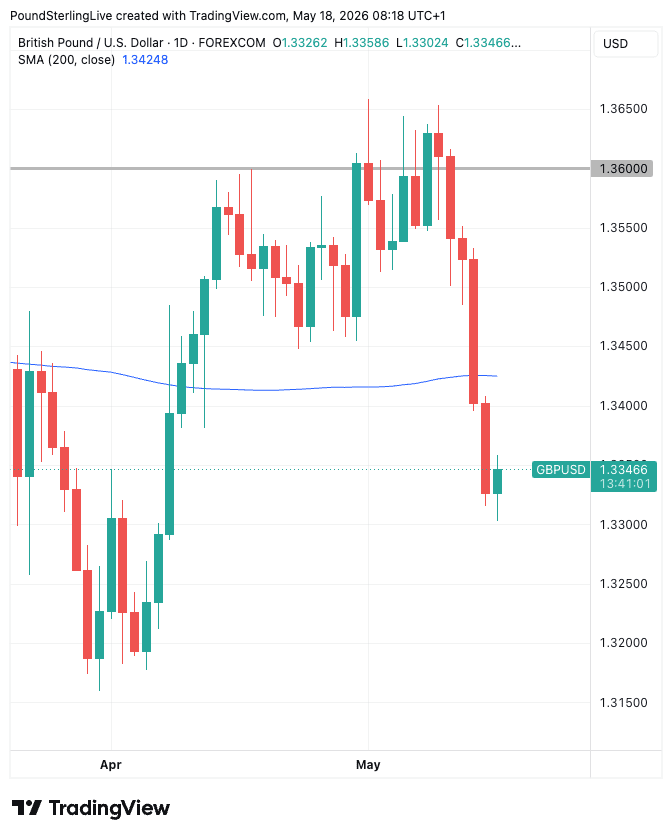

Last week, the pound to dollar exchange rate experienced its biggest weekly loss since November 2024, a sign that momentum is turning in favour of the dollar.

That loss was a combination of a powerful USD rebound, where the Greenback outperformed all G10 peers, and a broader selloff in the pound owing to rising political risks in the United Kingdom.

GBP/USD fell to a new one-month low on Monday at 1.3302, but has since recovered to 1.3350 by the time of writing. That early price action could hint that the 1.33 level could emerge as an early source of support and there is a chance that the first half of this week sees some mean-reversion of last week's sizeable selloff, which would take the market back to 1.3429, which is where the 200-day moving average is located.

If the 200-day MA level prevents further recovery, then it will be confirmed as a key resistance point. From there, further weakness would likely resume and a move below 1.33 transpires.

The dollar will remain the dominant partner in the pound-dollar exchange rate in the coming days. USD has recently outperformed all peers as traders adjust to the increasing likelihood the Federal Reserve will raise interest rates later this year.

The market has until now expected the Fed to lower interest rates on the view that inflation was steadily declining and the labour market was showing signs of emerging weakness.

However, recent data tells a story of ongoing economic resilience and a sharp rise in inflationary pressures.

Last week, it was revealed that headline CPI shot up to 3.8% y/y in April, and core rose to 2.8%. PPI inflation - which can tend to lead CPI inflation - surged to 6.0%, core PPI to 5.2%.

"We are revising our Fed call and no longer expect rate cuts in 2026," says TD Securities in a market briefing out Friday.

Should Fed rate hike bets rise further this week, the dollar would likely strengthen further.

Given this, the highlight for the USD is this week's two appearances of newly installed Fed Chair, Kevin Warsh, as we get to hear his thinking on the rates debate.

"I believe Waller’s two appearances are the most important events this week. If he flips hawkish, that’s a game changer. If he embraces a very dovish track, that is too," says Brent Donnelly, a strategist at Spectra Markets.

He speaks on Tuesday afternoon and again on Friday afternoon.

"The Tuesday appearance is a panel slot, and the Friday one is most interesting as it’s a full-on speech covering the economic outlook," says Donnelly.§

Turning to the GBP side of the equation, we're watching for further negative political headlines. Last week saw the pound drop sharply after Andy Burnham confirmed he would be standing in a by-election, which would allow him to return to Westminster.

The Labour Party will then install him as Prime Minister.

The pound dropped sharply after his announcement to account for higher odds of market-unfriendly outcomes under a Burnham government.

Burnham is now commanding close to a 60% chance of becoming the next Prime Minister, according to Polymarket. That suggests to us the market has largely priced the eventuality.

Of course, those odds could rise to 100%, which means a further move lower in sterling, but we suspect much of the Burnham adjustment has already happened.

"We close our short GBP/USD spot trade at 1.3397. We entered the trade at 1.3420 on 23 March," says strategist Kamal Sharma.

He says GBP political risk premia increased in the wake of last week's local elections as expected, which was the initial motivation for the trade.

"With these catalysts now behind us, we view it as prudent to exit following today's GBP selloff," says Sharma.

With a political repricing behind it, GBP/USD's risks are more symmetric this week.

Datawise, Wednesday's UK inflation figures will be of interest. The market looks for headline CPI to have eased back to 3.0% in April. Anything above this, and the pressure on the Bank of England to raise interest rates will rise.

That will keep UK bond yields elevated, providing some support for the pound via the interest rates channel.

Anything less, and yields could fall back, which could weigh on the pound more broadly.