Image © European Central Bank

Another soft week of trade beckons for the euro, but losses should be relatively contained.

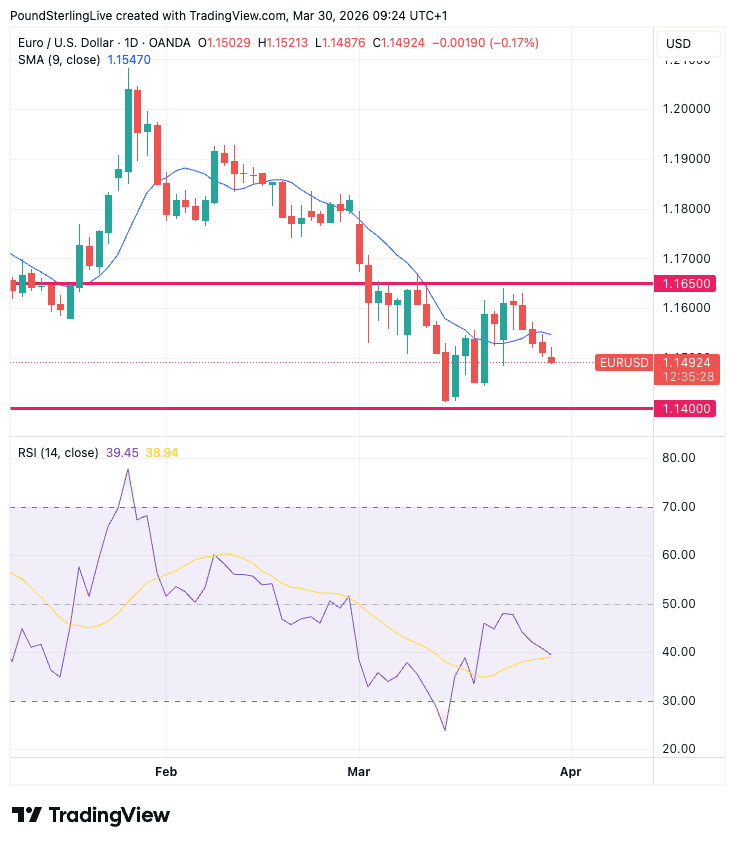

The euro-dollar exchange rate sinks to 1.1496 on Monday as a run of four consecutive daily losses threatens to extend to five, confirming momentum is to the downside.

The daily RSI reads at 39 and is pointing lower, while the pair is back below the nine-day simple moving average at 1.1547.

From here, eyes turn to the March lows, which are close to 1.14, where we would expect some support to emerge.

Although the euro is trending lower again, it is doing so in an orderly fashion and there's nothing to suggest the foreign exchange market is panicking; that should protect the downside.

In this type of environment, where losses are gradual rather than sharp, timing becomes more important for those with international payments, as small day-to-day moves can still accumulate into a meaningful difference.

In such conditions, some may look to set target exchange rates or use market orders to capture short-term improvements, rather than relying on spot pricing alone.

A number of analysts we follow say the dollar is proving relatively subdued and could be much stronger given the scale of the energy crisis, which is starting to have significant negative effects on the global economy.

Fuel rationing and efforts to control consumption are reported in numerous economies as shortages are contemplated. That signals a slowdown in global growth, which is classic manna for the dollar.

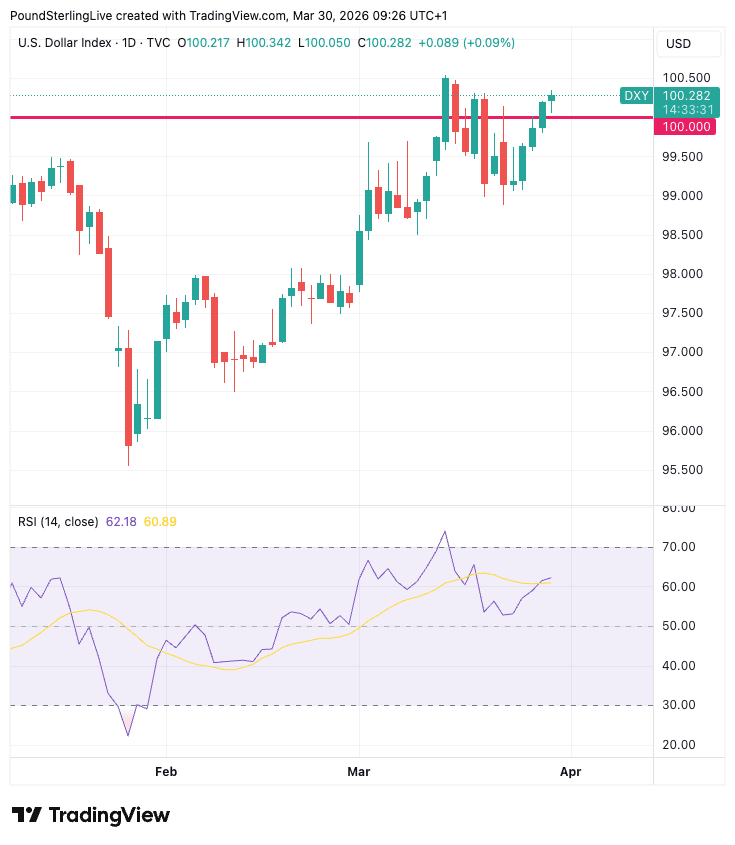

Yet, the dollar index, a measure of broader dollar performance, is struggling to crack through the ceiling at 100. That's keeping EUR/USD supported above 1.14.

👉 For those planning transfers, this creates a more balanced but still fragile environment, where the downside in EUR/USD remains intact, but is unlikely to accelerate without a fresh catalyst.

Where larger amounts are involved, even modest moves in the exchange rate can materially affect the outcome, particularly when combined with the wider margins typically charged by banks on international payments.

Currency strategists at Barclays say we're still "a few months out" from a euro recovery as escalation risks in the Middle East are high and it will take some time to establish a new equilibrium once the conflict ends.

But when that happens, the euro-dollar is forecast by analysts at the bank to snap back.

"At that point the dollar could weaken more broadly and we have pencilled in a 1.18 EUR/$ forecast for the next quarter. Of course the path can be highly volatile and it is very hard to underwrite the risk from an oil spike," says a regular weekly analysis from Barclays.

Above: The dollar index is capped below resistance at 100. We're watching the current move through here and are alert to the potential for a break and run higher. That would send the euro-dollar lower more forcefully.

Analysts at ING say the euro-dollar weakness is cyclical rather than structural, and under all scenarios, the exchange rate will still end the year above current levels, even as near-term risks remain skewed to the downside.

"All our EUR/USD scenarios end up above current spot levels by the end of the year," says ING.

So although the near-term favours further euro-dollar weakness, and that's what we anticipate in the coming week, it's clear there are limits to that weakness.

A consistent observation made by economists is that the oil and energy chaos sparked by the Iran crisis is different to that sparked by Russia's invasion of Iran. That was very much a Eurocentric shock, and the EUR/USD pair fell below parity at the time.

This time is different as Asia is the Middle East's biggest customer of oil and natural gas: indeed, money markets have moved to 'price in' rate hikes at the European Central Bank, judging that the central bank will raise rates in response to rising inflation risks.

That is offering the euro a floor against the dollar, given that similar repricing in Federal Reserve expectations has not been as aggressive.

Navigating that split outlook requires balancing near-term execution against longer-term expectations.

In situations like this, some may look to stage their transfers over time or combine fixed rates with flexible orders, reducing exposure to short-term volatility while retaining upside potential if the market turns.

Having access to guidance can help structure this approach more effectively, particularly where both timing and execution matter.