France's President Macron seeks to make the case for more joint issuance of EU bonds at a meeting of EU leaders later this month. Image Copyright: European Union.

France is lobbying fellow EU countries to bolster the Euro's reserve currency status.

Paris has lobbied fellow EU members to pledge additional measures aimed at raising the euro’s profile as a global reserve currency, as part of Paris’ long-standing campaign for more joint borrowing.

The development comes as the U.S. Dollar's status as the de facto global currency is brought into question by erratic and insular policy-making under U.S. President Donald Trump.

A draft EU statement circulated by France ahead of an EU leaders' summit wants EU institutions "to explore actions to reinforce the international role of the euro".

France says international investors are looking for a safe haven from U.S. Treasury debt, so the EU should issue more joint debt to service the market, according to officials familiar with its thinking.

W. Brad Bechtel, head of FX strategy at Jefferies Bank, says he sees a window of opportunity for the Euro:

"The U.S. is basically giving it to them if they feel compelled to take it," he says of the opportunity for the Euro to claim a share of the USD's reserve status.

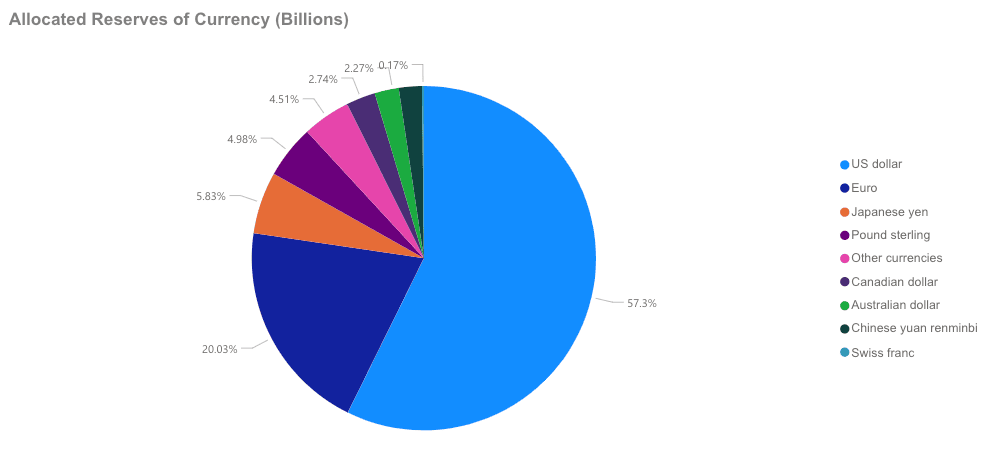

Image source: IMF.

A reserve currency status is highly coveted because it brings significant economic, financial, and geopolitical advantages.

It allows the U.S. to borrow more cheaply as investors are willing to accept lower yields on government debt.

Separately, IMF managing director Kristalina Georgieva said in Luxembourg this week that "there is a great opportunity for the euro to play a bigger role globally".

The ECB’s chief economist, Philip Lane, said earlier this month that the design of the Eurozone had resulted in an "undersupply of safe assets".

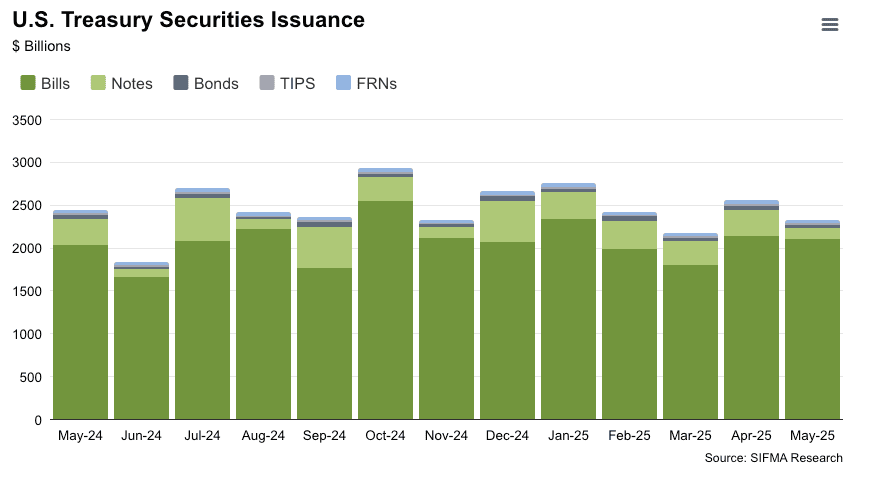

The U.S. owes much of its privileged reserve status to the significant size of the U.S. Treasury bond market. German Bunds are the closest thing resembling the safety of the U.S. Treasury that the Euro has in its corner.

But Germany's fiscal discipline means there are far fewer Bunds in circulation.

Above: The USD reserve status is underpinned by the significant issuance of U.S. Treasury bonds. Image courtesy of sifma.org.

The argument being made by France, the ECB's President Christina Lagarde, Lane and the IMF's Georgieva is that an increase in 'Euro bonds' on behalf of all EU countries can create the necessary large pool of safe assets that the Euro requires to challenge the U.S. Dollar's privileged reserve status.

"We are witnessing a profound shift in the global order: open markets and multilateral rules are fracturing, and even the dominant role of the US dollar, the cornerstone of the system, is no longer certain," Lagarde said earlier this week in the FT.

However, proponents of a 'reserve euro' also acknowledge the headwinds that stand in the way of achieving this.

"Europe must strengthen three foundational pillars: geopolitical credibility, economic resilience, and legal and institutional integrity," said Lagarde.

Jefferies says that Europe lacks the depth and liquidity in fixed income markets that underpin the dollar’s global status.

Regulatory fragmentation, unresolved energy vulnerabilities, and institutional inefficiencies will also continue to weigh on the euro’s ability to achieve a reserve status that mirrors that of the U.S.

"Lagarde is correct to say that eurozone cohesion, including removing national vetoes and deepening capital markets, is essential if the euro is to meaningfully rival the dollar," the Jefferies note says.

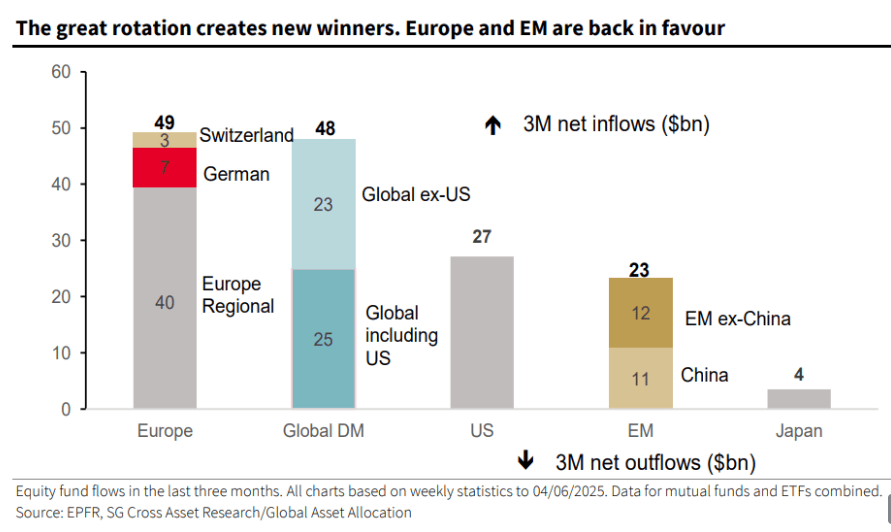

Above image courtesy of Société Générale.

A fresh analysis from Société Générale reveals accelerating signs of "de-dollarisation" in global financial markets, as central banks and institutional investors diversify away from U.S. assets in response to geopolitical risks, policy unpredictability, and structural shifts in the global economy.

Société Générale’s latest fund flow analysis also identifies structural shifts in capital allocation. U.S. equity and bond markets are seeing relatively weaker foreign inflows compared to previous cycles, particularly from reserve managers and sovereign wealth funds.

Meanwhile, allocations to non-U.S. markets, especially in Asia, have steadily increased.

According to Bank of America’s latest Global Fund Manager Survey, global fund managers are more underweight the U.S. dollar than at any point in the past two decades, reflecting a major shift in sentiment amid concerns over U.S. fiscal stability and diminishing rate support.

The June survey, which polled 206 participants managing a collective $640 billion in assets, found that net investor positioning on the dollar has fallen to its lowest level since 2004.

This marks a stark reversal from recent years when dollar strength dominated global currency markets on the back of aggressive Federal Reserve tightening and safe-haven flows.

"Relative to history, investors are overweight the Euro, bonds, & utilities and are underweight the U.S. dollar, energy, & US stocks," says Bank of America.