Image © European Union - European Parliament.

The Euro can retrace the 2025 rally.

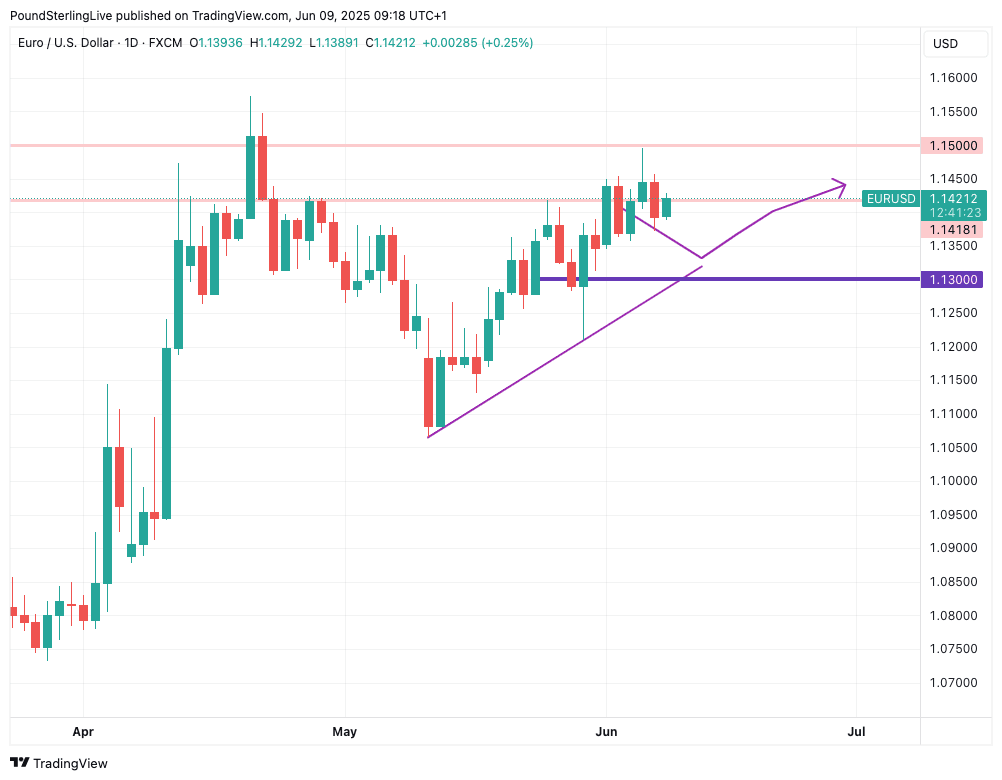

The Euro to Dollar exchange rate (EUR/USD) could retreat further in the coming days before eventually rebooting the 2025 uptrend.

The below chart shows our previous week's forecast annotations, and we are looking to hold onto them in the coming week:

Above: EUR/USD at daily intervals.

Consensus projections for the next four quarters, compiled from leading investment banks.

Access the full forecast →

The annotations provide a rough sketch that describes how we see the near-term playing out: some pullback in the exchange rate as a hefty long position in the trade thwarts upside momentum. (Everyone and his dog is betting against the Dollar, meaning the position is bloated and increasingly inert.)

Any further weakness could extend towards the 1.13 support line over the coming days, and we would look for buying interest to reassert itself from here in keeping with the uptrend, which is annotated by the rising purple line in the chart.

Should 1.13 give way, then we would be inclined to look for a deeper period of consolidation to ensue, perhaps carrying us through the summer months. For now, we think the uptrend holds, and that is why we would look for an eventual move to 1.15 by July.

Euro-Dollar retreated last Friday following a stronger-than-forecast U.S. employment report that showed the economy remains robust despite U.S. President Donald Trump's at-times erratic policy making, verbal attacks on the Federal Reserve and anxiety over tariffs.

To be sure, the U.S. economy is slowing and exceptionalism is waning, which ultimately underpins the Dollar's retreat. However, the official data is telling us that the fallout from tariffs is relatively contained for now, which argues against a rapid decline in the Dollar.

Potentially helping the Dollar recover in the coming days will be trade talks between China and the U.S. in London, with the two sides aiming to resolve issues such as rare-earth exports, tariffs, and restrictions on advanced technology.

The U.S. is seeking to restore flows of critical minerals, and China is seeking tariff reductions and an easing of export controls.

Progress here will settle nerves about the trade war and ultimately point to an overall tariff burden that is lower than a counterfactual where China and the U.S. fail to reach a resolution on outstanding issues.

This would be good for the U.S. economy and the Dollar.

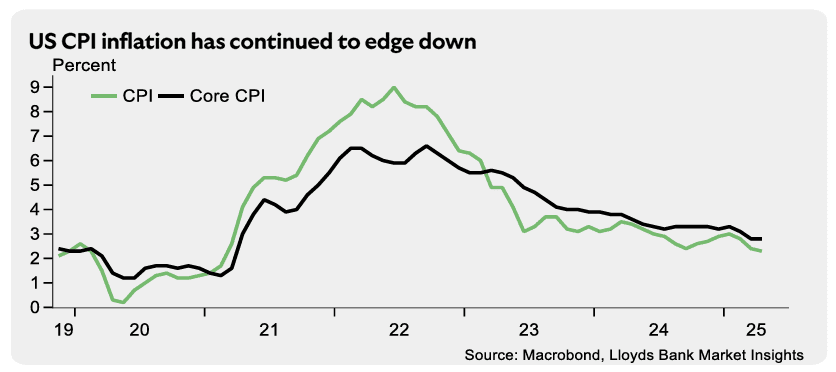

Image courtesy of Lloyds Bank.

The major U.S. calendar event is Wednesday's inflation print, where a reading of 2.5% y/y is expected. Anything above here would lower the odds of a Federal Reserve rate cut in the coming months, and boost the Dollar.

That being said, U.S. interest rate expectations have been relatively irrelevant to the Dollar of late, meaning the broader diversification away from the U.S. by foreign investors in response to Trump's policies should remain the key driver of USD.

"We still think foreign investors will continue to see a stronger case for diversification ahead, especially when there are signs of a less-welcoming environment for foreign investors in U.S. assets. As a result, while Dollar depreciation may be shifting to a new phase, we still think it is here to stay," says Kamakshya Trivedi, FX analyst at Goldman Sachs.