- EUR/USD steadier on feet & attempting a recovery

- Key averages obstruct near & above 1.08 on chart

- U.S. CPI & bond yields could prompt fresh losses

- If core inflation remains stuck around recent levels

- ECB's views on European recession risk in focus

Image © European Union - European Parliament, Reproduced Under CC Licensing.

The Euro to Dollar exchange rate has rebounded from near three-month lows in recent sessions and entered the new week on the front foot but U.S. inflation, a Federal Reserve (Fed) interest rate decision and European Central Bank (ECB) update are just some of the factors that could undermine its recovery in the days ahead.

Europe's single currency was an underperformer among major currencies in the week to Monday but still managed to rally notably against the Dollar late last week after the Bureau of Labor Statistics reported a sharp increase in new unemployment-related welfare claims for the prior week.

The data was another indication of the Fed's interest rate having the intended effect and the resulting selling of the Dollar helped lift the Euro to almost 1.08 last week despite Eurostat revisions to economic growth estimates suggesting the Euro Area economy slipped into a technical recession in the opening quarter.

"The ECB is likely to downplay a mild technical recession in the euro area as only a handful of countries have been affected," says Nerijus Maciulis, an analyst at Swedbank.

"Manufacturing continues contracting in most euro area countries, while many services sectors have benefited from increased tourist flows and general consumer willingness to splurge on experiences rather than goods. Booming services sectors also explain continued strength in the labour markets," he adds.

Above: Euro to Dollar rate shown at daily intervals with Fibonacci retracements of March rally indicating possible areas of technical support. Click for closer inspection.

What a technical recession means for the ECB won't be known until Thursday but the bank emphasised last month that future policy decisions would be "data dependent" while many economists still expect another increase in interest rates this week, followed by at least one more in either July or September.

It would not necessarily hurt the Euro if the ECB writes off the recession as a technical affair and could help the single currency if the bank indicates further increases are still likely but the risk is of the EUR/USD rebound being undermined beforehand by either Tuesday's U.S. inflation figures or Wednesday's Federal Reserve decision.

"We suspect that the Fed meeting the day before and above all the data releases in the US in the following weeks will generate swings in the significantly more volatile Fed rate expectations that will ultimately do the heavy lifting in driving EUR/USD moves," says Francesco Pesole, an FX strategist at ING.

"The EUR/USD decline throughout the month of May was primarily driven by the hawkish repricing in Fed rate expectations, while market pricing on ECB tightening held relatively stable," Pesole writes in a Monday research briefing.

EUR/USD fell throughout last month as markets gave up pricing-in interest rate for later this year and after U.S. inflation fell less than was expected for the month of April.

Above: Euro to Dollar rate shown at daily intervals with spread or gap between 02-year German and U.S. government bond yields. Click for closer inspection.

The consensus is for inflation to have fallen from 4.9% to 4.1% last month and for the core inflation rate to fall from 5.5% to a new low of 5.3%.

"It feels like volatility will likely peak with the release of US CPI on Tuesday," says Bipan Rai, North American head of FX strategy at CIBC Capital Markets.

"Since the May decision, the data has been mixed though still firm enough to justify additional action from the Fed. We just don’t think that it comes this week," he adds.

U.S. inflation has fallen steadily since last June but the moderation has slowed in recent months while the core inflation rate, which central bankers see as the most reliable reflection of domestic inflation pressures, has remained stuck at 5.5% so far.

The big risk for the Euro and others this week is of the core rate remaining around its recent levels rather than falling further and leading financial markets to anticipate additional increases in the Fed's interest rates, potentially as soon as this Wednesday.

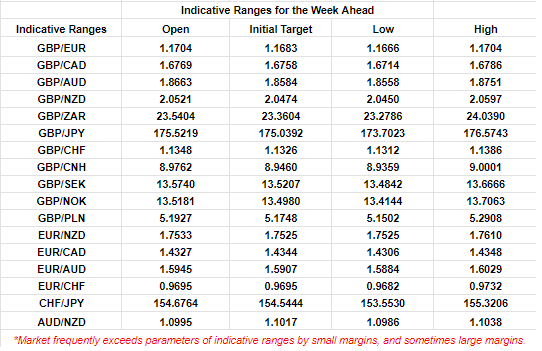

Above: Quantitative model estimates of ranges for this week. Source Pound Sterling Live.

Wednesday's Fed decision is widely expected to see interest rates left unchanged for the first time in more than a year after policymakers suggested throughout May that it could be preferable for them to observe how the economy and inflation respond to the 5% increase implemented since March 2022.

One other factor with scope to impact the Euro is economic data out in China where there is also speculation about a possible interest rate cut from the People's Bank of China (PBoC) in between the Fed and ECB decisions.

This would risk perpetuating the recent weakening of the Renminbi, which has accelerated since early in May while also broadening out to include depreciation against non-Dollar currencies following a string of official reports suggesting the recovery in the world's second-largest economy is losing momentum.

"China's dollar-denominated exports dropped by more than expected 7.5% YoY in May. The downturn in demand from the US and ASEAN was a key factor dragging down export growth," says Tommy Xie, head of Greater China research at OCBC Bank.

"Conversely, China's demand for key commodities such as crude oil and iron ore increased, with imports by volume rising by 12.3% YoY and 3.95% YoY. Nevertheless, imports by value fell by 13.98% YoY and 12.52% YoY," Xie writes in Monday commentary.

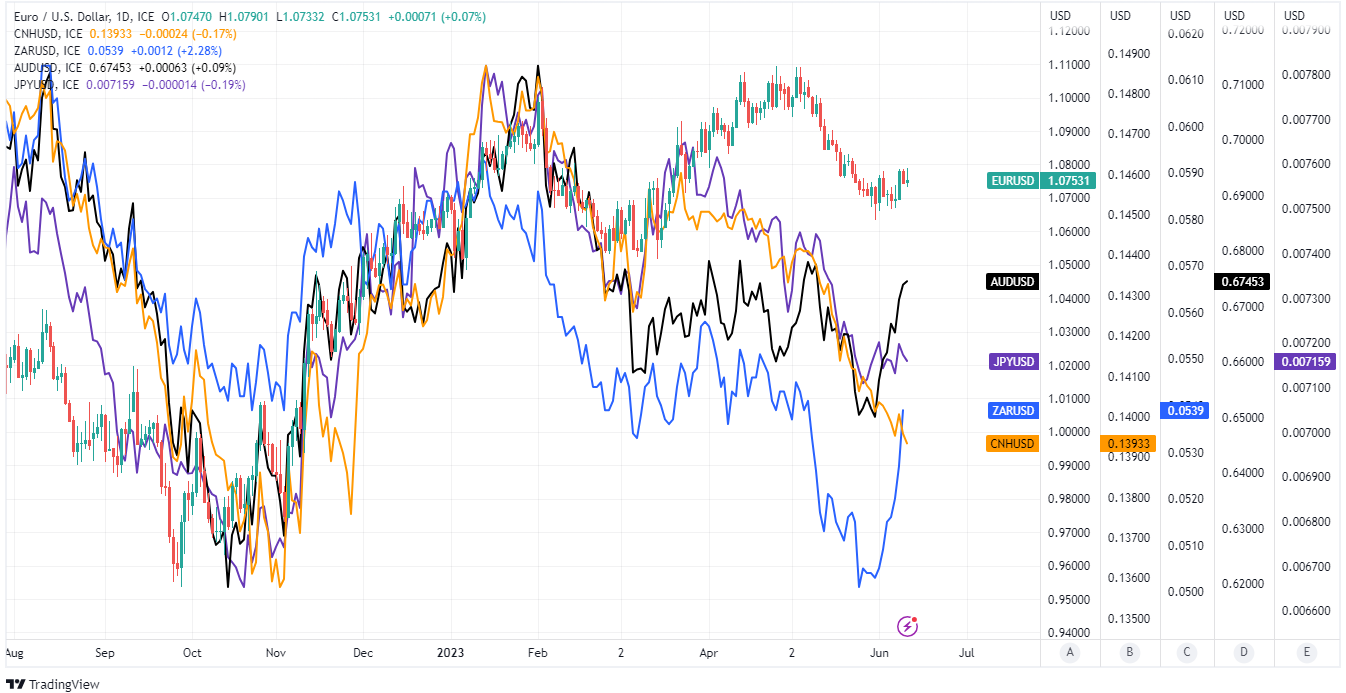

Above: Euro to Dollar rate shown at daily intervals with Reminbi-Dollar rate (orange) and other selected exchange rates.