"It is our view that the EUR is not fully priced for the headwinds facing the Eurozone economy," - Rabobank

Image © Alfred Yaghobzadeh, European Commission Audiovisual Services

Europe's single currency benefited from a widespread retreat by the U.S. Dollar ahead of the weekend but its depreciation is not yet over and could yet lead the Euro-Dollar rate to fresh lows in the months ahead, according to newly downgraded forecasts from Goldman Sachs and Rabobank.

Dollars were sold widely on Friday in price action that enabled a beleaguered Euro to rise against most G20 counterparts with the only exceptions being in relation to currencies of commodity exporting economies like Norway, Australia, New Zealand and Canada.

Friday's bid for commodity currencies came amid more speculation about a possible change in the coronavirus-related policies of China's government and enabled EUR/USD to climb back above 0.99, although some forecasters say this latest relief is likely to prove short-lived for the single currency.

"The Euro area’s deteriorating terms of trade are already weighing on the currency, and we expect this has more room to run, especially if the looming recession prompts the ECB to take a more cautious approach, as we expect," says Michael Cahill, a G10 FX strategist at Goldman Sachs.

"As a result, we are nudging down our 3-month EUR/USD forecast to 0.94," Cahill and colleague Isabella Rosenberg write in a Friday research briefing.

Above: Euro to Dollar rate shown at weekly intervals with selected moving-averages. Click image for closer inspection.

Above: Euro to Dollar rate shown at weekly intervals with selected moving-averages. Click image for closer inspection.

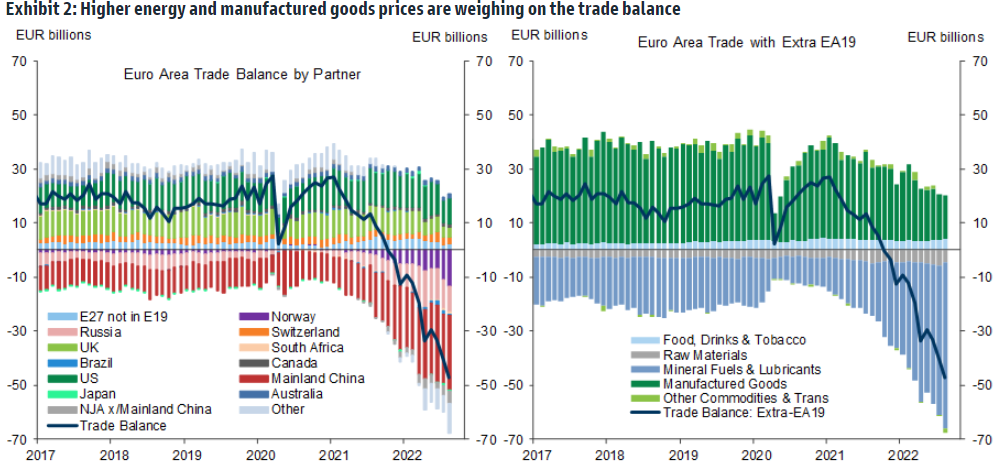

Divergence between Federal Reserve (Fed) and European Central Bank (ECB) interest rates is one factor to have recently weighed heavily upon the Euro but elevated energy costs and the persistent risk of energy supply disruptions are by the far the more important drivers of the single currency's losses.

Historic increases in energy prices have driven inflation higher at the same time as they have hampered the economy and converted the continent's goods and services trade surplus into a gaping deficit that has seen more Euros sold on the market in exchange for Dollars and other currencies this year.

"Using our GSFEER model, we can more formally explore what a more permanent shift to higher import prices would mean for the currency, and specially the Euro’s “fair value"," Cahill and Rosenberg say.

"We are already seeing evidence that higher production costs are weighing on Euro area activity, with implications at least for the near-term outlook, and some concerning signs for the long-run production capacity," they add.

Goldman Sachs estimates that Europe's single currency would now be fairly valued around 1.24 against the Dollar but notes that it has been trading at a discount to estimates of fair value for some time, hence why Cahill and Rosenberg downgraded the firm's forecast for EUR/USD on Friday.

This estimate of fair value has itself been downgraded from around 1.45 at the start of the year and a point when EUR/USD was trading near to 1.12.

Source: Goldman Sachs Global Investment Research. Click image for closer inspection.

Source: Goldman Sachs Global Investment Research. Click image for closer inspection.

"This morning’s release of September German factory orders data registered a shockingly weak -4.0% m/m fall, far worse than the market consensus of -0.5% m/m," says Jane Foley, head of FX strategy at Rabobank.

"Yet, there has been an onslaught of risks facing the German production sector in recent months from both the demand and supply sides. It is our view that the EUR is not fully priced for the headwinds facing the Eurozone economy," she adds in a Friday review of forecasts for the Euro.

Foley cites high energy prices and uncertainty about "where gas for next winter or the winter after that will come from" for thinking the darkest days may be yet to come for the Eurozone industrial sector, overall economy and currency.

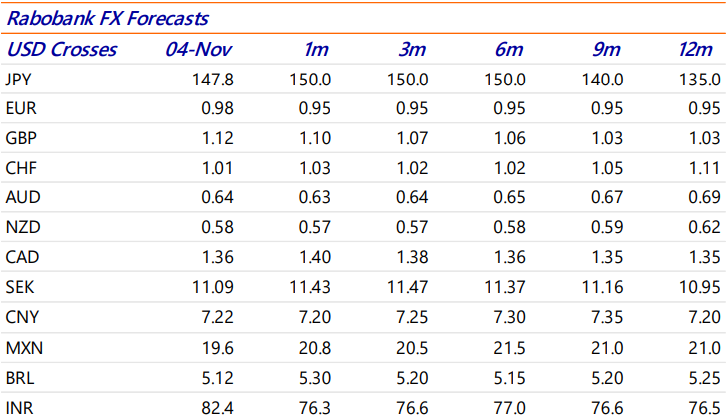

She and the Rabobank team had previously expected the Euro-Dollar rate to recover to 1.05 by the end of next year but downgraded that forecast this week and warned of a possible decline to 0.95 in the months ahead.

"The BASF decision [to reduce production in Europe] was clearly based on a medium or longer-term cost evaluation. Other high energy-using producers in sectors such as pulp, aluminium smelting, glass, and vehicle manufacturing had already come to similar conclusions," she says.

Source: Rabobank. Click image for closer inspection.

Source: Rabobank. Click image for closer inspection.