- EUR/USD recovery seen ahead with forecast risks shifting higher.

- Penance paid for EU vaccine missteps with rollout set to quicken.

- As economy shows resilience ahead of a mid-year growth surge.

- Goldman Sachs forecasts 1.21 in three-months as ING eyes 1.22.

- EUR/USD could overcome January highs & hit 1.25 this summer.

Image © Adobe Stock.

- EUR/USD spot rate at time of writing: 1.1898

- Bank transfer rate (indicative guide): 1.1505-1.1590

- FX specialist providers (indicative guide): 1.1702-1.1799

- More information on FX specialist rates here

- Set an exchange rate alert here

The Euro-to-Dollar rate was consolidating a recovery of its 200-day average Tuesday having declined to back off from 1.19 amid increasing signs that it has bottomed out, some of which prompted Goldman Sachs to warn that risks to the bank's bullish forecasts are now shifting to the upside.

There have been multiple signs the Euro has passed peak pessimism and although it still lacks the fundamental case necessary to sustain itself much beyond current levels the bearish prosecution of the single currency has clearly run aground and the balance of risks to the outlook is now shifting to the upside.

Some of these signs are why Goldman Sachs said following a review of the Euro’s performance and prospects that the single currency has paid its penance for earlier shortcomings including missteps in the procurement and rollout of coronavirus vaccines, and that there’s little to justify further losses.

“The Euro depreciated nearly 4% vs the US Dollar in Q1 as markets priced earlier rate hikes from the Fed and as continental Europe experienced another wave of covid infections. Neither factor supports continued EUR/USD weakness, in our view, and we now see upside risks to our 3m forecast of 1.21,” says Zach Pandl, Goldman Sachs’ co-head of global foreign exchange strategy.

The coronavirus picture across Europe remains chequered though there has been clear progress in reducing or at least stemming increases in new infections across Italy, Germany and France as well as in major Eastern European economies over the last week or so.

Above: Euro-Dollar consolidates claim on 200-day average after rebound off 38.2% Fibonacci retracement of 2020's rally.

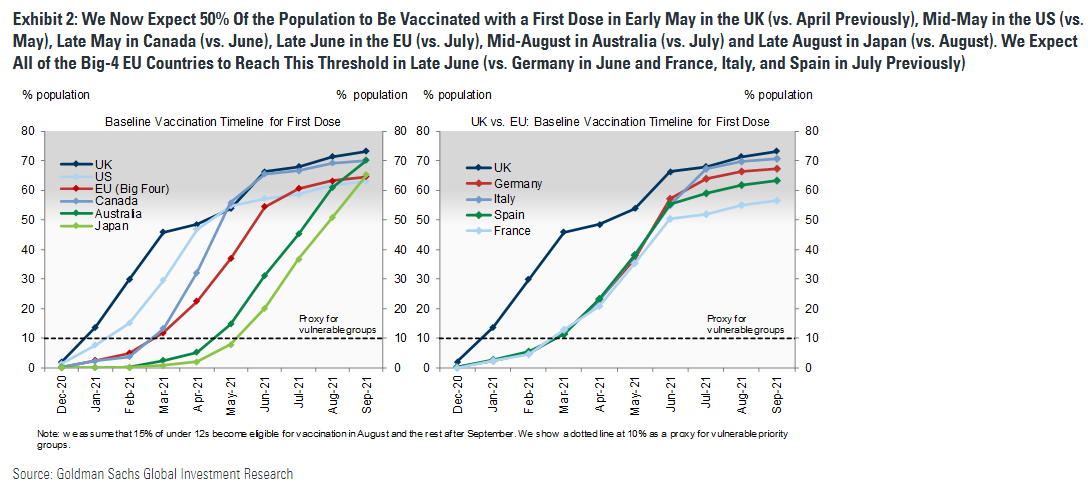

Vaccinations have picked up and are increasingly expected to become more widely available in the months ahead, especially in Europe's major economies.

Indicators of activity in Europe’s services and manufacturing sectors surprised on the upside for the March month and with the continent’s third wave ebbing and vaccination campaign quickening, economists at Goldman Sachs have “rising confidence in their forecast for a mid-year surge in growth.”

Meanwhile, over in the U.S. the bond market sell-off has lost momentum and last week the 10-year bond took a blowout March payrolls report in its stride when barely registering a 600k odd increase that was significantly higher than consensus had suggested was likely.

“We are not ready to say bond markets have fully discounted the coming boom in growth, but range-bound yields suggest that is at least a possibility,” Pandl writes in a recent note. “If bond markets can look through a stronger-than-expected Core CPI result as well, rate volatility may begin to come down, opening room for Dollar shorts vs EUR and potentially other crosses.”

Image © Goldman Sachs Global Investment Research. Click image to enlarge.

The April quieting of the bond market has helped take the wind from the Dollar’s sails while positive developments around vaccinations in Europe and a tentatively less ‘dovish’ European Central Bank (ECB) all appear to play a role in the apparent profit-taking that lifted EUR/USD last week.

Europe’s single currency has risen from 1.17 to 1.19, aided by what appeared to be the closure of short EUR/GBP, EUR/CAD and EUR/NZD trades that were all popular during recent months in price action which has left bearish views on the Euro appearing somewhat stale.

Goldman Sachs forecasts EUR/USD to rise to 1.27 over the next six months, which is substantially above the 1.20 level implied as likely by prices in the market for forward hedging contracts, with the single currency then expected to edge higher to 1.28 by the 12-month horizon.

Analysts at the bank look for the Euro to rise to 1.21 over the next six months, which isn’t dissimilar to the latest forecasts from ING Group.

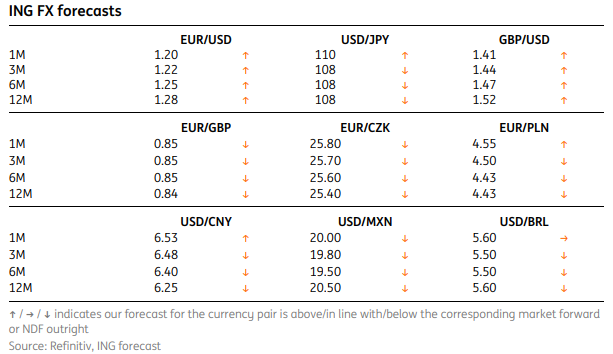

Image © ING Group.

ING sees the single currency rising from its first quarter trough to eventually overcome the highs around 1.2350 seen in January this year.

“The glacial rollout of vaccination programmes and the ‘crown jewel’ of the EU’s fiscal stimulus – the EU’s €750bn Recovery Fund – gathering dust in a Karlsruhe courtroom stand in stark contrast to the achievements in the US. Yet all is not lost,” says Petr Krpata, chief EMEA strategist for FX and bonds at ING. “Our EUR/USD profile is slightly dimmed, but we still expect the EUR to arise from the ashes of European policy.”

Krpata and the ING team also cite a resilient European manufacturing industry and prospect of wider vaccine availability for continuing to expect an economic pick-up and Euro-Dollar recovery in 2021, which is seen lifting the single currency back to 1.20 in one-month horizon and 1.22 in three months.

The bank also looks for the Euro to reach 1.25 this summer, though this isn't expected until much before September. To the extent that these forecasts are on the money they vindicate the Goldman Sachs team for warning of upside risks to the bank’s three month forecast of 1.21 this week.

Image © Natwest Markets.

There are caveats in all cases however, and most notably relating to the U.S. bond market and speed of any further increase in yields. That means this Tuesday's March U.S. inflation data, due out at 13:30, will be a watershed moment for the U.S. Dollar and Euro with analysts and investors looking to see if the bond market can weather an upside surprise.

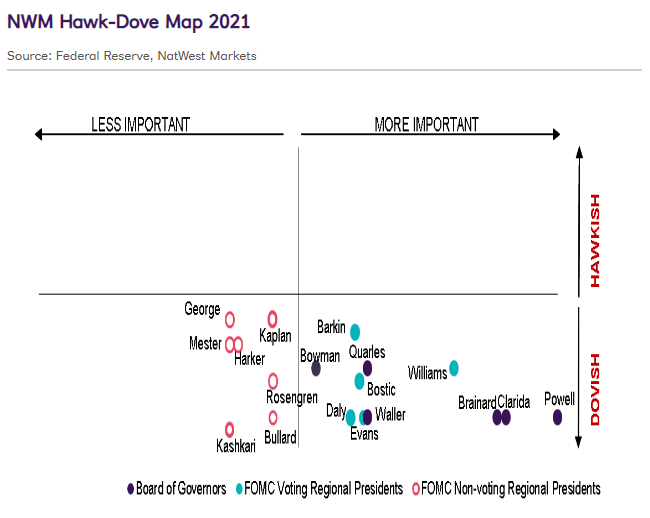

But it could be that both currencies are most sensitive to disappointment given investors’ views on the Federal Reserve (Fed) outlook.

“Neither Powell nor Clarida provided much new specificity on what "substantial further progress," other than Clarida reiterating that it is based on actual progress. Ultimately, the bigger question is how the data will evolve,” says Kevin Cummins, chief U.S. economist at Natwest Markets. “While "substantial further progress" on the maximum employment goal seems likely in our view (given the scope for growth once the economy fully re-opens), the outlook for inflation remains more unclear. Clarida mentioned the importance of inflation data at the end of this year will be key to whether the expected uptick in inflation in coming months is transitory or long-lasting. Specifically, he said “We would expect those to be transitory and as the year progresses and we go into next year, if they’re not, then we’ll have to take that into account certainly.”

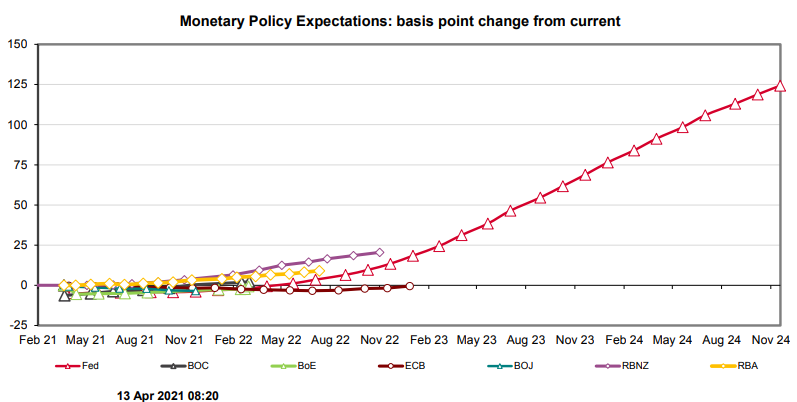

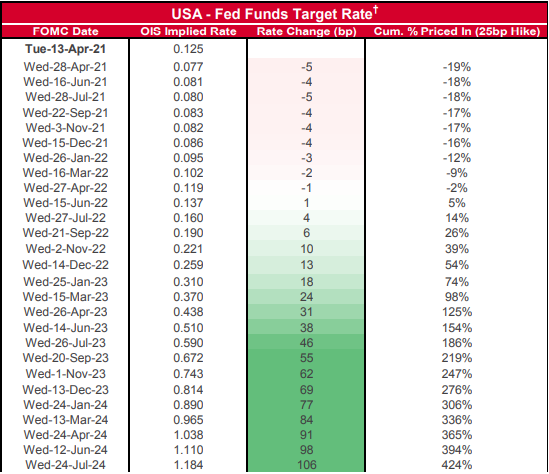

Pricing of overnight-index-swaps, a derivative market that enables inventors to protect against as well as speculate on changes in interest rates, implied on Tuesday that investors see around a 50:50 chance of the Fed raising the Federal Funds rate to a higher range of 0.25% to 0.50% by the end of 2022.

Image © Westpac.

That market also implied a fairly hefty chance of at least two rate rises taking the range up to between 0.50% to 0.75% before the end of 2023, which helps to explain why the U.S. Dollar has strengthened broadly in recent months but creates a vulnerability for the greenback.

The above kind of interest rate outlook and Dollar’s prospects going forward are hinged almost entirely on the the likely U.S. inflation situation around year-end because in order for the Fed to begin raising interest rates around the end of next year, it would likely first need to be in a position to begin tapering its $120bn per month quantitative easing programme from the end of 2021.

“Westpac is a little more cautious on 2021 US growth than the FOMC, but also anticipates the output gap will close by the end of 2022. We are again more circumspect on the US’ prospects in 2023 and beyond, absent an infrastructure and investment stimulus package later this year. We therefore believe the FOMC is right to wait to see its expectations achieved before acting on policy, both with respect to a taper and, eventually, rate increases,” says Westpac's Elliot Clarke. “We expect the US 10-year yield will only tend towards 2.5% by end-2022, the FOMC’s longer-run estimate of the neutral Fed Funds Rate. While the US looks set to outperform the global recovery in 2021, for our entire forecast period to end-2022, it is more likely to lag, particularly against Asia and emerging markets where medium-term development prospects are stronger.”

Image © Westpac.