© European Central Bank, reproduced under CC licensing

- EUR/USD spot rate at time of writing: 1.2140

- Bank transfer rate (indicative guide): 1.1692-1.1777

- FX specialist providers (indicative guide): 1.1934-1.2031

- More information on FX specialist rates here

The Euro-Dollar rate could be on the cusp of becoming a more prominent consideration in European Central Bank (ECB) policymaking, a development that could see the Euro outlook more closely tied to that of Pound Sterling.

ECB policymakers are reportedly investigating the extent to which the EUR/USD rally of 2020 has been driven by differences between monetary policies of the ECB and Federal Reserve (Fed) with a view to determining if offsetting action needs to be taken, according to a Tuesday report from Bloomberg News.

The review is potentially a tentative step toward linking the rising Euro more explicitly with persistently inadequate Eurozone inflation and could ultimately see policy decisions taken at least partly in response to the impact currency fluctuations have on the outlook for price pressures.

"This unusual focus on the exchange rates seems to confirm our fears that the ECB increasingly wants to use the euro as the scapegoat for the inflation target being missed. At that point it would only be a very small step to conclude that due to EUR appreciation further monetary policy easing might be required," says Esther Reichelt, an analyst at Commerzbank. "Thanks to the ECB applying the brakes, the upside in EUR-USD seems increasingly unattractive for now."

The Euro was lower against most major rivals as the Dollar rebounded ahead of the latest Fed decision and amid widespread risk-aversion in global markets, but EUR/USD was still up more than 10% for the year to Wednesday.

Above: EUR/USD shown at weekly intervals alongside EUR/CNH (blue).

Dollars have been sold widely and many analysts still expect most U.S. exchange rates to decline further in 2021. The Euro has been one of more popular destinations for fleeing capital, although the resulting increase in EUR/USD now threatens to entrench already-negative inflation pressures. Europe's inflation rates have languished far below the ECB's target of "close to but below 2%" for years despite the bank's efforts aimed at stimulating the economy into producing the price growth expected of it.

"If the ECB is serious about pushing back against EUR strength, and the implications for its domestic inflation target, it’ll look at emphasizing that inflation overshoots will be tolerated over the coming cycle. Its own policy review is expected to be completed at some point this year. If that is the case, then we’ll have to re-examine our strategic USD view to account for this shift. Until then, our bias is still to fade USD strength for this year," says Bipan Rai, North American head of FX strategy at CIBC Capital Markets.

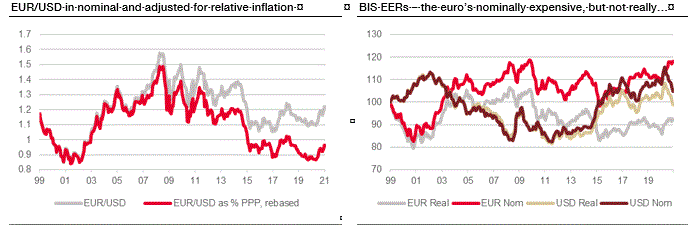

With the Dollar 10% lower than year-ago levels, imports from Europe's largest trade partner have cheapened in what is potentially a further drag on inflation. But with other components of the trade-weighted Euro near decade highs, disinflationary pressure is greater than belied by EUR/USD alone.

"I think the mere fact the ECB is looking at what happened is enough for EUR/JPY shorts, as well as EUR/GBP and EUR/AUD shorts. But away from that, this ought to be a reminder that if you let your currency reach extremes in valuation, it's more likely than not to mean-revert in real terms over time," says Kit Juckes, chief FX strategist at Societe Generale. "Where in nominal terms, EUR/USD is slightly stronger today than it was 22 years ago, in real terms it's 20% cheaper. Rising from the low range it reached when the ECB adopted negative rates and QE. The ECB has had its cake and can't eat it again."

However, and with the ECB already having cut its interest rates as far as it's able to and run down its capacity for quantitative easing by already snapping up around a third of the Eurozone bond market since 2015, the best that Frankfurt might be able to do now is to hope that movements in other exchange rates do the heavy lifting for it by deflating the trade-weighted Euro.

"Keeping a lid on the euro might be relatively easy in the near term as there are few reasons outside of valuation to bid up the single currency on the reflation trade, as fiscal stimulus to stoke a recovery across the EU will prove weaker than elsewhere, and where negative interest rates weigh heavily on the currency. EURJPY is one place to look for further potential euro weakness as the JPY is even less fairly priced in real, inflation adjusted terms," says John Hardy, head of FX strategy at Saxo Bank.

Above: EUR/GBP shown at weekly intervals alongside EUR/CNH (blue).

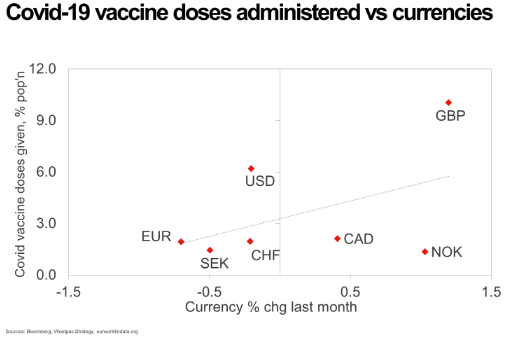

But if hope is to become the ECB's strategy and any other exchange rate is likely to do any heavy lifting at all it might be the Pound-to-Euro rate. Sterling emains beneath its long-term average against the Euro and could soon benefit from a faster vaccine rollout than is seen in Europe this year.

"Meaningful disparities in vaccine doses administered are emerging across the major economies. That might create potentially large growth differentials in coming months. The UK is leaping ahead of its peers, with 10% of the population having received a Covid-19 vaccine. Despite a chaotic rollout and widespread shortages the US has delivered a single dose to 6% of the population, while much of Europe is sitting around 1.5-2.0%," says Richard Franulovich, head of FX strategy at Westpac.

The Euro remained close to its strongest level for five years relative to the Chinese Yuan this week, which accounts for around 17% of the trade-weighted Euro index and has the second highest weighting in the TWI barometer after the U.S. Dollar. In addition, the Euro was still closer to post-referendum highs against Pound Sterling than it was post-referendum lows, and the British currency is a further 15% of the Eurozone TWI.

Source: Westpac.

But Sterling could turn the tables on the Euro if the UK economy gets a headstart in a recovery later this year after leading the European field on vaccinations, and it's one of the few currencies with a significant enough weighting to offset for the trade-weighted Euro any further upward moves in EUR/USD. The only other currency with enough sway over the index is the Yuan, but with China's unit rising 7% in the last year already, it may have less scope than Sterling to gain further against either of its main rivals.

That was true even before this week's reports suggesting that 2020's appreciation of the Yuan is hampering the comptetiveness of Chinese businesses, which is something that might eventually lead the People's Bank of China to attempt to prevent its exchange rates from rising. This could mean if anything that further declines in EUR/CNH are less likely to be seen than falls in EUR/GBP, which is represented by the blue line on the graph below.

"China is better served by a stronger currency and higher domestic consumption. Yet there are lots of suffering SMEs with lots and lots of jobs on the line, and what looks like a renewed US push to look at China supply chain issues even under Biden," says Michael Every, a global strategist at Rabobank. "If we do see CNY get Cold War ice on its wings, like a Celsius-inverted Icarus, it would be a huge shoe to drop on the head of the great 2021 reflation trade."

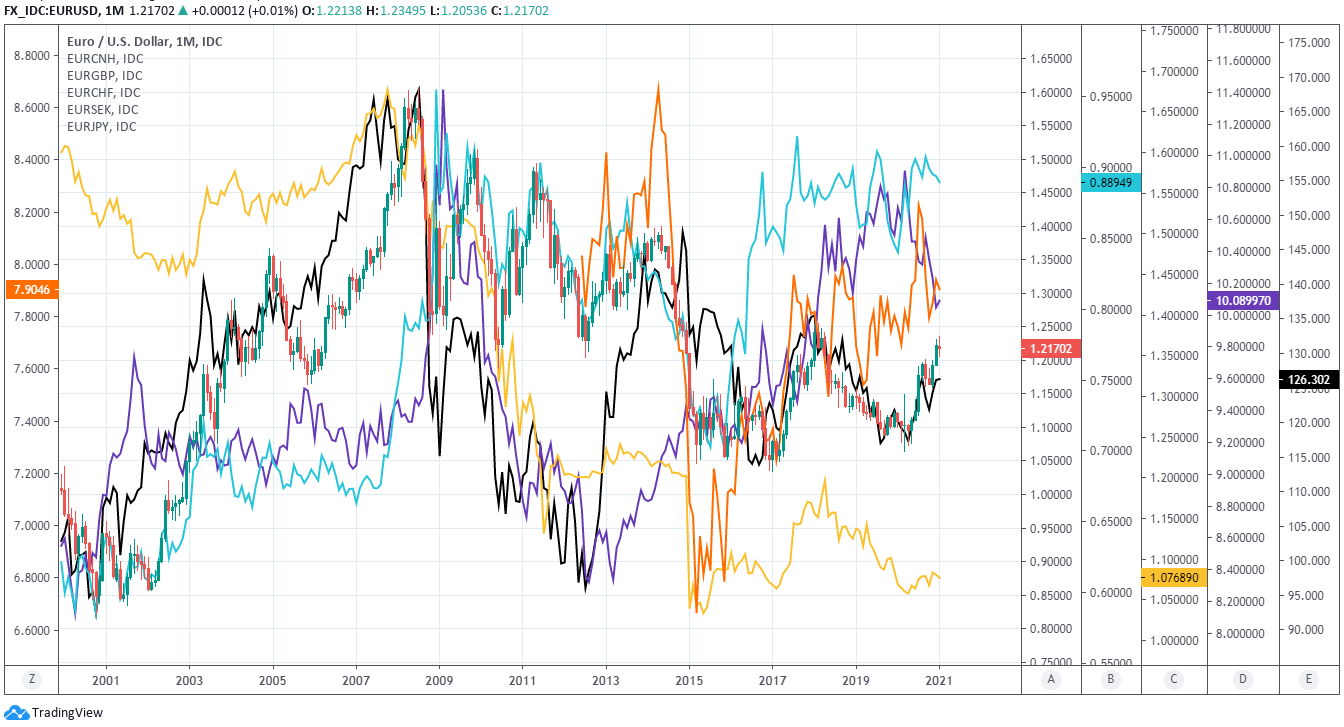

Above: EUR/USD and other major euro exchange rates shown at monthly intervals. Click image for closer inspection.