© Christian Müller, Adobe Stock

- ZEW survey reveals further economic weakness in early 2019.

- Expectations tick higher although not enough to support EUR.

- Eurozone, Germany may remain at stall-speed for first half 2019.

The Euro was on its back foot in the face of a strong U.S. Dollar and more negative economic reports Thursday, which continue to undermine the market's appetite for the single currency.

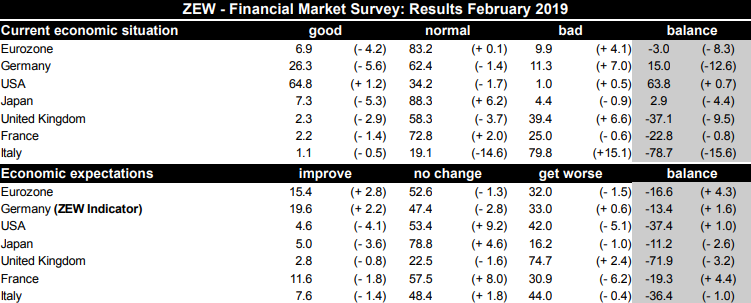

Germany's ZEW economic climate index rose faster than was expected during February, coming in at -13.4 for the current month, up from -15 in January and when markets had looked for an increase to only -14.1.

The survey showed investors becoming less pessimistic about the six month outlook for the economy. However, the rub for the Euro is that those investors are still downright pessimistic in their expectations for the economy over the next six months.

Furthermore, and what the headline numbers don't reveal is, investors became even more downbeat about current levels of activity suggesting the economy have remained at stall speed or possibly even shrank during the January and February months.

"The assessment of the current situation has experienced a considerable decline. For the next six months, the financial market experts in our survey do not expect any improvement,” says Achim Wambach, president of the Leibniz Centre for European Economic Research (ZEW).

The ZEW sentiment index for current activity in the broader Eurozone fell by 4.3 points to -16.6 this month while the index gauging expectations of the next six months also declined, from +5 to -3. That is bad news for the single currency.

Above: ZEW survey results for current and future expectations of economies.

Tuesday's result is a negative for the Euro because both German and Eurozone economic growth has already fallen sharply during the last six months and it's yet to be determined for certain whether or not the German economy fell into recession in late 2018. Final GDP data will be released Friday.

ZEW's February findings suggest there is a risk that both economies remain at their stall-speed for the first half of the current year, which will do little to bring about a recovery of an already-stricken Euro.

"There still is hope but not a lot. A rising ZEW index, combined with a still falling current assessment component, suggest the pessimism will end, eventually," says Carsten Brzeski, an economist at ING Group.

The ZEW survey polls more than 300 institutional investors to assess their view of the economy's current and likely future performance. It covers both Germany and the Eurozone. A number above zero is consistent with rising confidence and economic activity and a number below zero suggests to opposite.

Markets care about the data because changes in business confidence can often act as a leading indicator of changes in overall activity within the corporate sector, enabling economists and investors to get an early steer on the likely pace of GDP growth in a given period.

Above: Euro-to-Dollar rate shown at daily intervals.

The Euro was quoted -0.30% lower at 1.1277 against a stronger U.S. Dollar Thursday while the Euro-to-Pound rate was -0.19% lower at 0.8737. Both exchange rates have fallen thus far in the New Year, and are down -1.61% and -2.88% respectively.

Above: Euro-to-Pound rate shown at daily intervals.

Notably for the single currency, investors polled for the February ZEW survey also said their expectation for short-term European Central Bank (ECB) interest rates deteriorated notably this month. The corresponding indicator fell 5.3 points to just 6.8.

A total of 92.2% of respondents expect no increase in ECB interest rates during the next six months, up 5.3% since the last survey, while just 7.3% of respondents still expect a rate hike. This explains the balance of 6.8 for the short-term rate outlook.

Earlier in the Tuesday session ECB data showed Europe's trade surplus falling and investment flows into continental economies melting away in December, amid an economic slowdown, uncertainty over White House trade policy and the Brexit saga as well as extreme financial market volatility.

The ECB has already acknowledged risks to the economic outlook are now tilted to the downside and hinted strongly in January that it may be 2020 before the bank is able to lift its interest rate from current record low levels.

Its main interest rate is still at 0% and its deposit rate is at -0.4%, meaning it costs banks to deposit money at the ECB rather than paying them. But the ECB ended its multi-year quantitative easing programme in December and previously stopped the targeted-long-term-refinancing-operations (TLTRO) that provided cheap cash to banks.

However, since then the flow of economic data has pointed in an increasingly pronounced manner to a steep economic slowdown that is being driven by multiple factors including the domestic and the international.

The Eurozone economy grew by 1.8% in 2018, down from 2.4% the previous year, while the European Commission recently forecast the economy will grow by just 1.3% in 2019.

Quarterly growth rates in the Germany and the Eurozone fell by more than half throughout the 2018 year, from 0.7% at the end of 2017 to the 0.2% seen in the final three months of last year.

And now, markets are increasingly fearful that President Donald Trump could choose to impose tariffs of up to 25% on Eurozone exports of cars to the U.S., in order to achieve leverage over the European Commission in current and future trade negotiations. That would make things even worse.

Time to move your money? Get 3-5% more currency than your bank would offer by using the services of foreign exchange specialists at RationalFX. A specialist broker can deliver you an exchange rate closer to the real market rate, thereby saving you substantial quantities of currency. Find out more here.

* Advertisement