Image © European Central Bank.

- EUR/USD remains stuck in range between 1.12 and 1.15

- Pair will probably continue sideways

- Sentiment data could feature prominently for both currencies

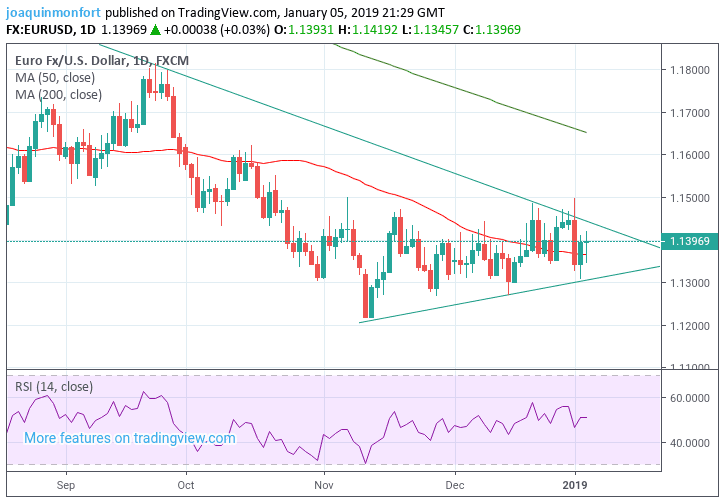

The Euro-to-U.S. Dollar rate starts the new week trading at 1.1397 after a decline of roughly a quarter of a percent from the start of the week.

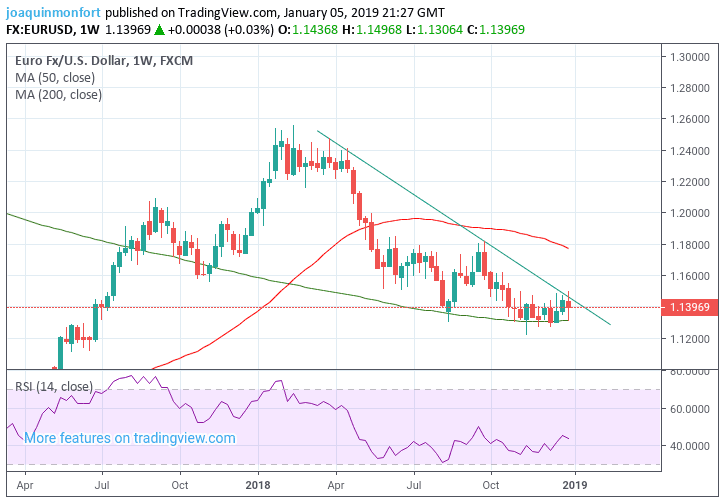

The relatively small change in value reflects the range-bound nature of the market, which has been oscillating between 1.15 and 1.12 ever since early November.

This sideways trend is likely to continue in the week ahead, although there are now also increasing risks that it could breakout more strongly in one direction or another, as the key trendlines delineating the dominant trends on the different time horizons, converge and compress the exchange rate into a narrowing apex.

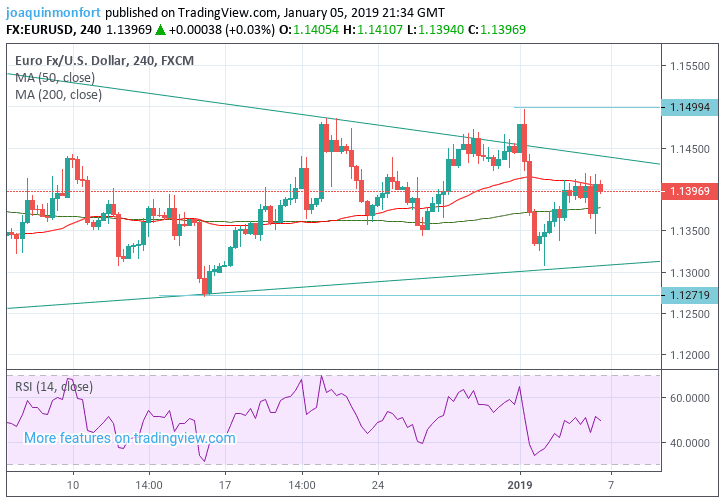

Last Wednesday the pair temporarily broke out of this compressing range above the downsloping trendline and peaked at 1.1496, before pulling back and closing back down below the trendline.

This failed attempt was, nevertheless, a bullish sign for the pair and suggests the possibility of more upside, should the exchange rate be able to break back above the level. The 1.1496 highs represent a key rubicon and a break above them would be a strong reversal sign. Such a move would signal a continuation up to a target at 1.1545 initially, followed by 1.1620.

In equal measure we should also probably give due consideration to the influence of the medium-term dominant downtrend and the fact this could bias the market to sell the pair. As such a break below the 1.1269 December 14 lows would probably confirm a resumption lower to revisit the 1.1215 lows.

The vulnerable look of the RSI momentum indicator on the 4hr chart, as well as the lack of upside strength in the recent recovery from off the 2nd of Jan lows, both predispose the pair to some short-term weakness, perhaps down to the trendline at 1.1300, but a break of the 1.1269 level would be required to cement a more bearish outlook.

Advertisement

Bank-beating exchange rates. Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here

The U.S. Dollar: What to Watch

The U.S. Dollar was buoyed at the end last week by strong U.S. labour market data, which showed the economy employing a further 312k workers in December, well above expectations and the long-run average of around 200k.

The positive employment data continues to suggest underlying strength in the U.S. economy and that fears of a recession are over-egged, yet not all data is equally strong and the overall picture is mixed.

The wide variance in data may well be brought into relief again at the start of the week ahead with the first major release on the calendar, the ISM Non-Manufacturing PMI survey for December, a major sentiment survey for the services sector. It is forecast to dip to 59.1 from 60.7 in the previous month, when it is released on Monday at 16.00 GMT.

The ISM ‘Non-Manufacturing’ survey is the sister survey of the ISM Manufacturing PMI, which has already been released, and showed a considerable decline in December, last week.

The Manufacturing ISM showed growth slowing much more than expected in December to 54.1 from 59.3 in the previous month. This bodes ill for Non-Manufacturing which often follows its lead. A slowdown of a similar degree would be negative for the Dollar.

Another major factor which could move the Dollar is commentary from Federal Reserve (Fed) officials who are responsible for setting interest rates. Fed Chairman Jerome Powell is set to speak on Thursday at 17:00, Bullard at 18.30 and Evans at 19.00.

The trajectory of Federal Reserve interest rates in 2019 is a key focus not just for the Dollar but for the wider markets. Markets have greatly reduced their expectations for further interest rate rises over coming months, based on the observation that economic growth in the U.S. economy is slowing.

The Dollar tends to outperform on the expectations for further rate rises, therefore they dynamic of pricing fewer interest rate rises going forward is, on balance, negative for the currency's outlook.

To what extent will the Fed ease back on raising interest rates? Is the slowing economic activity in the U.S. seen as a mere blip, or a cause for greater concern?

Markets will be seeking answers on the above when the Fed officials speak, and therefore what is said could well prove the highlight for the U.S. Dollar this week.

The Euro: What to Watch

Sentiment often leads hard facts, so Eurozone sentiment data for December, scheduled for release on Tuesday, is probably the most important economic release on the calendar for the Euro in the week head.

Economic sentiment has fallen for 11 months in a row and forecasters expect more of the same in December, when it is estimated to decline from 109.5 to a new 2018 low of 108.4. If they are right, it could weigh heavily on the single currency.

Eurozone business confidence, out at the same time of 11.00 GMT, has been in a step decline for most of the year too, reaching a trough low in October when it fell to 1.01. Although it has since rebounded to 1.09 investors will want to see a more sustained rally in December to regain confidence. The consensus from forecasters, however, is that it will fall even lower to 0.99.

Another major release for the single currency is the minutes of the December meeting of the European Central Bank (ECB) scheduled for release at 13.30, on Thursday, January 10.

The ECB sets monetary policy in the Eurozone which is a major driver of the exchange rate, so what they think about the economic situation, as divulged in the minutes can sometimes impact on Forex, especially if it diverges from currency market thinking.

In December the ECB made the historic decision of ending quantitative easing (QE), whereby the central bank purchases debt instruments from Euro-area financial institutions in an effort to liquify the system and keep lending affordable. This removal of QE was a sign the ECB had more faith in the economy and lent support to the Euro.

Some analysts, however, argued the withdrawal of stimulus was premature as the region still needs QE. If this view is echoed in the minutes it could lead to expectations the ECB may continue with easy monetary policy and weaken the Euro.

The ECB is widely expected to continue to tighten policy in the region in 2019 and even hike interest rates in September, however, a feeling that the economy is still vulnerable as introduced doubts it will be able to go ahead. If the minutes back this view up it could weigh heavily.

Other major releases for the Euro include the unemployment rate which is expected to come out at 8.1%, when it is released at 11.00 on Thursday, and retail sales for November, which is forecast to show a rise of 0.1% in November, when it is released on Monday at 11.00.

Advertisement

Bank-beating exchange rates. Get up to 3-5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here