Image © European Central Bank

- Established downtrend showing reversal potential

- Breakthrough in China-US relations the catalyst

- Retail sales to drive the Euro; Non-farm payrolls the Dollar

The Euro could see pressure from the U.S. Dollar over coming days suggest our technical studies while headlines concerning U.S.-China trade relations could weigh on the Greenback.

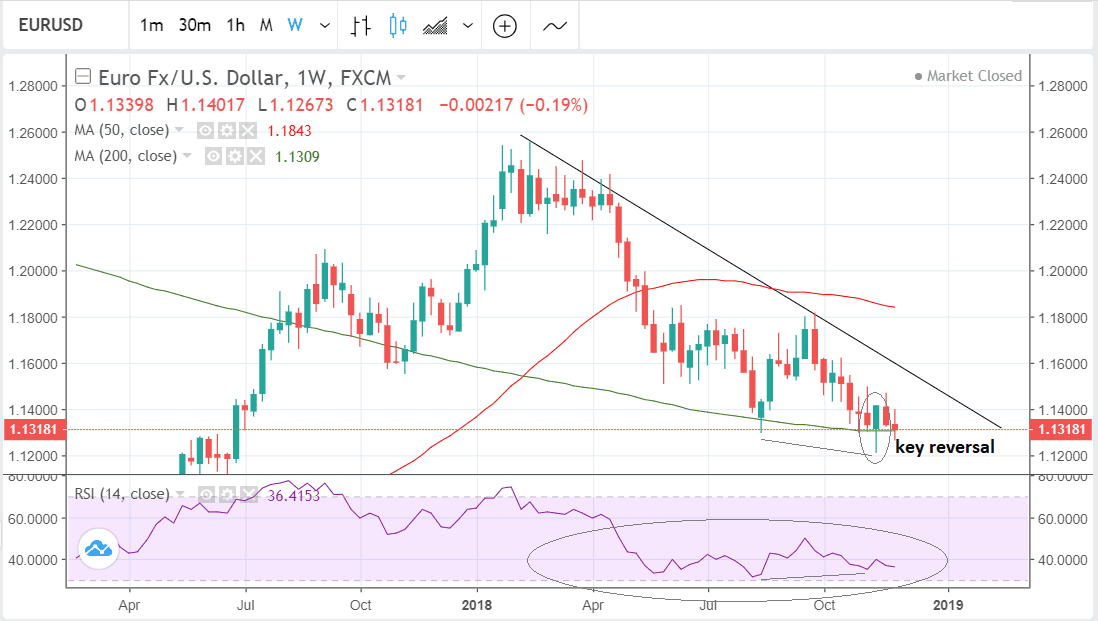

The Euro-to-Dollar rate slid to close back down near the key 1.13 hard floor at 1.1318 in the previous week after the Euro lost ground following the release of Eurozone economic data that points to an ongoing slowdown in Eurozone growth.

The Dollar was broadly softer too - on expectations the Federal Reserve might pull back the throttle on raising of interest rates - it, nevertheless, still outperformed the single currency.

The weekly chart shows how last week’s decline brought the pair down to the 1.1300 floor where the 200-day moving average (MA) is also providing a ‘bower’ of support.

From a technical perspective, the downtrend is dominant and given the saying that the “trend is your friend...” would be expected to continue.

However, there are also signs that hint at a reversal while weekend headlines concerning China-U.S. trade relations could well weigh on the U.S. Dollar in the week ahead.

On the technical front, the pair has formed a reversal signal called a ‘key reversal’ bar two weeks ago and this is a strong sign the broader trend could be about to reverse higher.

The pair has also converged bullishly with the RSI momentum indicator in the bottom panel. This merely means that when price formed a new low the RSI didn’t follow, and this lack of symmetry is considered a bullish indicator.

The fact the 200-week MA is providing underpinning support is a further bullish sign as prices often have a habit of reversing at the level of major MAs.

Easing trade tensions between China and the U.S. are a fundamental bullish catalyst for the pair. An improvement in trade relations is bearish for the U.S. Dollar which trades like a safe-haven in relation to geopolitical trade events, and is, therefore, bullish for EUR/USD.

Over the weekend President’s Trump and Xi met at the G20 summit and agreed to halt the implementation of more trade tariffs. This means the US will delay increasing tariffs on $250bn of Chinese goods previously planned for the 1st of January 2019.

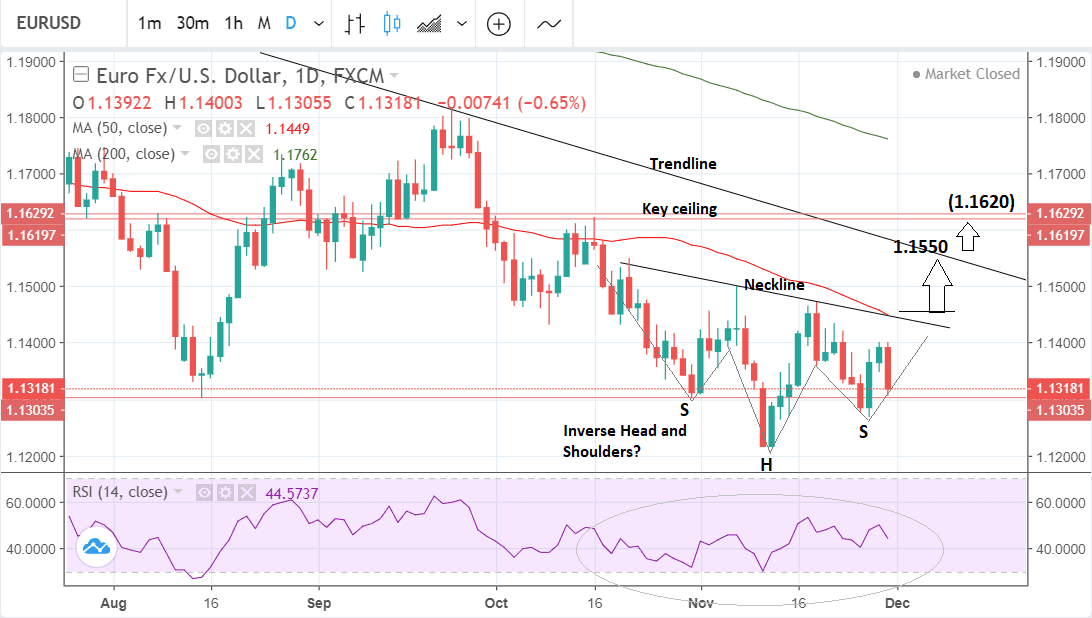

The daily chart is showing a possible bullish pattern called an inverse head and shoulders (H&S) may have formed at the lows. It is composed of three troughs with the central low (the head) lower than the two either side (the shoulders).

The H&S’s neckline is drawn along the intervening peaks separating the three trough lows. If broken it provides confirmation of more upside. The normal length of the upside extension is equivalent to the distance from the lowest trough to the neckline replicated to the upside, or 61.8% of the length.

This indicates an upside target to 1.1620 eventually, although the trendline at 1.1550 is likely to provide an obstacle and offers a more conservative target.

A break above the neckline would be confirmed by a close above on a daily basis or a move above 1.1470.

The EUR/USD will start the week at 1.1318 on the open market however high-street banks will be offering rates in the region of 1.0922-1.10 for international payments, independent specialists are likely to be quoting between 1.12-1.1240.

The Euro: What to Watch this Week

It is a relatively quiet week for the Euro, although there is a risk of continued wrangling over Italy’s budget causing volatility.

Nevertheless, Italian PM Conte and EU Commission president Tusk were said to have made progress at talks at the G20 and the Italian government has now finally made concessions, saying they will consider reducing the deficit by 0.2%. Crucially it has shown ‘willing’ where once there was none and this has soothed markets.

On the 'hard' data front, the main release is probably retail sales for October out on Thursday, which is forecast to show a rise of 0.2% when it is released at 10.00 on Wednesday. If so, this would be an improvement from the 0.0% previous result.

Retail sales is often an early warning of growth so the October rate will be useful in gauging Q4 GDP growth. GDP slowed to only 0.2% in Q3 and if it continues to fall in Q4 it could signal a deeper contraction in the region with more profound implications.

A rebound, on the other hand, would play into the hands of the ECB who have largely underplayed the slowdown in growth the Eurozone has suffered over recent weeks.

The European Central Bank (ECB) president Mario Draghi will be making a speech on Wednesday at 8.30 and this could also generate interest if he mentions the outlook for monetary policy which has dimmed amidst the recent slowdown in growth.

If Draghi makes any hints that the ECB could be reconsidering its current roadmap for normalizing monetary policy, however - unlikely as that still seems - the Euro could plummet.

The other major Eurozone data releases are revisions of flash estimates of manufacturing and services PMIs (on Monday and Wednesday at 9.00 respectively), and the third and final estimate for the Q3 GDP growth rate out on Friday at 10.00.

The Dollar: What to Watch

The main release for the U.S. Dollar in the coming week is Non-farm payrolls, which is expected to show a 200k rise in November when released on Friday at 13.30 GMT.

Any result above 200k would be considered exceptionally strong given how tight the labour market is whilst any result above 150k would be considered robust.

A positive surprise would boost the Dollar as it might suggest upside risks to inflation and higher interest rates, which are a direct bullish driver for. currencies.

Another important release for the US Dollar is ISM Manufacturing PMI, which is forecast to show a slight uptick to 57.8 in November when it is released on Monday at 16.00. Anything above 50 indicates expansion of that sector and 60 is indicative of exceptionally strong growth, thus the forecast is for continued accelerating growth which could also be bullish for USD.

ISM Non-Manufacturing PMI is out on Wednesday and forecast to show a fall to 59.7 from 60.3 previously.

The US trade balance is forecast to show a widening of the trade deficit to -$54.9bn from -$54.0bn when it is released on Thursday at 13.30. The balance has been volatile of late whipsawing from improvement to decline in 2018.

Despite President Trump's efforts to reduce the deficit using tariffs, it's unclear what the overall trend is. If the deficit continues to widen it would be a very negative sign for the US economy.

The country's budget deficit is also expanding which makes the US dependent on outside funding. History tells us this is not a particularly strong position to be in as foreign lenders tend to require higher risk premiums and are more fickle in times of crisis than domestic creditors.

This can also impact negatively on the currency in the long term since the foreign sourced debts which must be repaid are usually denominated in foreign currencies.

Advertisement

Bank-beating EUR/USD exchange rates: Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here