Image © European Central Bank

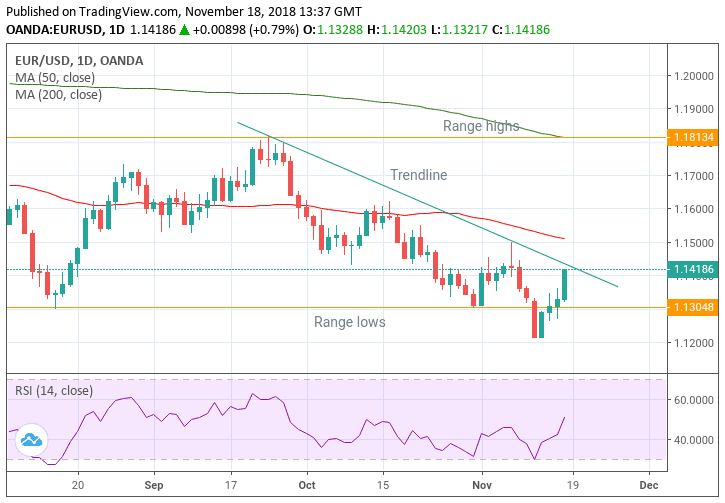

* EUR/USD has rebounded to a major trendline

* A break higher would consolidate the uptrend

* Italian risks are the main driver of the Euro, PMIs for the US Dollar

We are on balance bullish in our outlook for EUR/USD conditional upon the exchange rate successfully breaking above a key trendline.

EUR/USD temporarily fell beneath the 1.1301 August lows last week and reached a new yearly low of 1.1216. It then rebounded back up to close at 1.1418, back above the August lows.

The rebound came on the back of commentary from Federal Reserve (Fed) officials about the economy, which implied US growth might be impacted by a slowdown globally. The main driver for the rise in EUR/USD was the weakening Dollar rather than strengthening Euro.

The pair has now reached the trendline for the move down from the September highs and is likely to encounter tough resistance at that level.

This is a make-or-break moment where EUR/USD could either break clearly higher and begin a more bullish phase or encounter tough resistance from the trendline, leading to a reversal and a resumption of the broader trend lower.

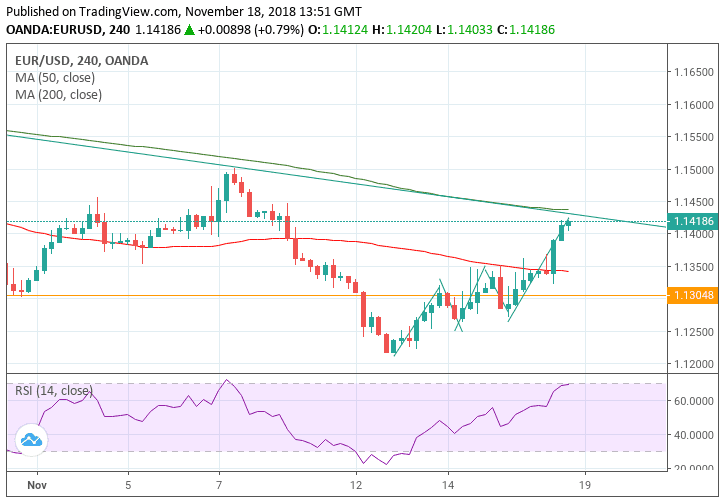

The four hour chart indicates that the short-term trend is probably bullish due to the rising sequence of peaks and troughs, which has now formed more than two higher highs and higher lows. Momentum is also quite strong indicating increased support for the uptrend, and raising the probability of it extending higher.

We are, on balance, bullish in our outlook conditional upon the exchange rate successfully breaking above the trendline which would be confirmed by a move above 1.1460, 1.1475 or for even greater confidence the 1.1501 highs.

This would then probably signal a continuation up to a target situated between 1.1550 and 1.1600.

The target is equivalent to the length of the move (or 61.8% of the length for a conservative estimate) immediately prior to the trendline extrapolated higher from the breakout point.

Advertisement

Bank-beating EUR/USD exchange rates: Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here

The Euro: What to Watch

The main factor impacting on the Euro in the week ahead will probably be news about the Italian budget and talks between Brussels and Rome. As things stand, neither side appears to be willing to stand down so consequently the issue is likely to be a source of volatility for the Euro.

The Italian government continues to insist on maintaining its original manifesto spending promises which would increase the deficit to 2.4%, arguing increased growth from the spending would offset the higher bill. The EU, as well as the International Monetary Fund, do not agree and say it would simply push up Italy's debt burden which is already the second highest in Europe.

Turbulence is particularly earmarked for Tuesday at 11.00 GMT when the E.U. Commission is scheduled to publish feedback on the the Italian government's latest revised budget proposal, although it is unlikely to differ from previous rejections very much.

A major data release for the Euro in the week ahead is Flash Services PMI for November, which is forecast to show a further reduction in activity to 53.0 from 53.1 reported in October, and is released on Thursday at 10.00.

PMIs are survey based gauges of economic activity and useful future indicators of GDP. The second PMI release in each quarter provides a highly reliable indicator of that quarter's GDP so November's data is even more significant than usual as it will be used to accurately predict Q4 Eurozone GDP.

Consumer confidence is a major release in the week ahead. Economists forecast a fall to -3 in November from -2.7 previously. Given the high impact on GDP from consumer spending, consumer confidence is an important gauge of growth.

The Eurozone current account is another major macroeconomic release in the week ahead which could impact on the single currency. It measures the country's gross balance of payments. Economic theory has it that a surplus is appreciative for a currency and a deficit depreciative. In September the surplus was 20.6bn, the consensus appears to be forecasting a rise in October.

The minutes from the meeting of the European Central Bank (ECB) are out at 14.45 on Wednesday and will reveal the governing council's thinking on the economy and future monetary policy.

The main thing analysts will be looking out for it whether the ECB is set on continuing its autopilot to reducing stimulus at the end of 2018 and increase interest rates after the summer of 2019. Recent lacklustre growth data appears to have brought into question whether the ECB will stick to its roadmap.

Any changes are likely to result in volatility for the Euro given how sensitive it is to changes in monetary policy strategy.

The US Dollar: What to Watch

Sentiment has turned negative against the Dollar after more cautious comments from members of the Federal Reserve (Fed) who suggested a perceived slowdown in global growth may rub off negatively on the US and that short-term interest rates have now risen to 'neutral’ (the rate at which the economy is neither growing nor slowing) which is where the Fed would like them to be, and, therefore, a sign it might pause in it's rate-hiking schedule.

If the Fed were to pause it would weaken the Dollar since there is already an expectation that it will raise rates again in December, and if it changes its mind, the consequent disappointment will probably weigh on the USD.

Higher interest rates, or the expectation of higher interest rates, normally appreciates a currency and vice-versa for lower rates. This is because the former attract greater inflows of foreign capital drawn by the promise of higher returns, whilst the latter act as a disincentive to inflows.

On the hard data front, November flash composite PMI are is probably the main release, out on Friday at 3.45 GMT, as it can provide an early indication of Q4 growth.

Researchers have found that the first two months PMIs in a quarter when averaged can be used to indicate growth for the whole quarter with a relatively high probability of success.

November Composite PMI is forecast to rise from 54.9 to 56.0 and if so this could indicate a rise in GDP growth rate in Q4, though the amount differs from country to country.

Another major release for the Dollar is Existing Home Sales in October, out at 16.00 on Wednesday, November 21. The metric is expected to bounce back to 5.15m from 5.2m in the previous month.

Existing home sales have been in decline ever since peaking in March, showing falls every month without fail. If they rebound in October it will mark a break of the 6 month run of uninterrupted declines and probably be positive for the Dollar since housing, according to the old Wall Street adage ‘leads the economy’.

Another major release for the Dollar in the week ahead is Durable Goods Orders in October, which are forecast to show a -2.5% change month-on-month from 0.8% in the previous month.

Durables is a volatile release, however, and large single orders especially in the transport and aviation sectors can skew the monthly data and render it volatile.

This appears to be what happened in September when durable goods orders rose 0.7%, propelled by defence aircraft orders which more than doubled, up 118.7%.

Advertisement

Bank-beating EUR/USD exchange rates: Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here