Above: Can the "Tusk Bump" extend into early trade in the new week? Image (C) European Commission.

Pound Sterling is seen recovering ground against the Euro over coming days with our technical studies suggesting more upside but Thursday's ECB event is a key event risk for markets to be aware of.

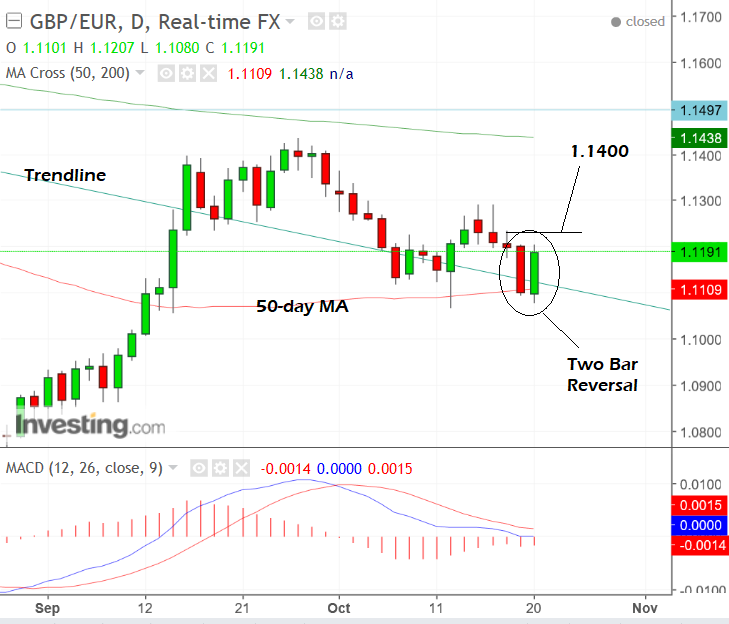

The Pound-to-Euro exchange rate chart confirms near-term direction is likely to be bullish.

Despite short-term selling pressure, the exchange rate has remained above a major trendline, which it initially broke above at the beginning of September.

A clear break above a major trendline is a bullish sign in itself, and to then hold above that trendline despite repeated attempts by sellers to push the exchange rate back under, is a sign the pair will eventually rise further - it is just a matter of time.

Zooming in to the daily chart, we note how the bullish outlook is reinforced by a two-bar reversal pattern that has formed during the last two days (circled below).

These patterns are indicators of a reversal in the short-term trend and, if Monday is an up-day, this will provide further confirmation of the bullish trend.

The daily chart also shows the 50-day moving average positioned just below recent price levels, underpinning support over the last two days, as well as a previous trough-low on October 12.

Moving averages are strong levels of dynamic support and resistance and when combined with the trendline, which is also supporting prices, the 50-day enhances the likelihood of further upside as well.

Overall, we see a break above the October 18 highs at 1.1236 as providing the confirmation necessary to expect more upside to come, with an eventual target at 1.1400.

Get up to 5% more foreign exchange by using a specialist provider by getting closer to the real market rate and avoid the gaping spreads charged by your bank for international payments. Learn more here.

Data, and Events that Could Move the the Pound

Politics will still feature for Sterling in the week ahead.

Whilst the EU decided at their summit last week that not enough progress had been made to move to phase 2 discussions on trade, there was a silver lining in the form of EU Council President Donald Tusk who was optimistic about a deal.

Tusk said he thought descriptions of talks as being at "deadlock" were exaggerated, that the EU would start internal preparations for phase 2 as a concession to the UK, and that he hoped the second phase would begin in December when the EU will have another summit to decide whether to go ahead with phase 2.

The Pound recovered on Tusk's more optimistic comments after having sold off almost all week, and we think there is a chance of a 'Tusk bump' on Monday as the market starts to see a light at the end of the Brexit tunnel.

Tusk’s optimistic tone regarding Brexit was mirrored by the leader of Europe’s largest economy; Germany’s Angela Merkel suggested much of the gloom and angst surrounding Brexit is a function of British media coverage.

Merkel’s view is that talks are certainly not in deadlock.

We agree that media and markets are prone to focussing on the negatives at the expense of the more optimistic elements of talks. A classic example is the fixation with EU lead negotiator Michel Barnier’s use of the word ‘deadlock’ following the fifth round of talks. Barnier did also say he believed a breakthrough was still likely before year-end.

The Pound was sold and newsprint almost focussed purely on the negative, this leaves the Pound relatively oversold and prone to upside corrections when reality dawns.

The main hard data release for the Pound will come in the form of the first release for third quarter GDP, out at 9.30 BST on Wednesday, October 25.

The consensus estimate is for GDP to grow at 0.3%, but the result could make the difference between whether the Bank of England (BOE) hikes rates or not in November.

"PMI data suggest the GDP numbers will show another lacklustre 0.3% expansion in the three months to September, matching the performance seen in the first half of the year. Even such a modest GDP expansion would be unlikely to change the views of the hawks on the Monetary Policy Committee, but a weaker number could lead to rates remaining on hold at the November meeting. A stronger number would be seen by many as sealing the deal on a hike," says Bernard Aw, Principle Economist at IHS Markit.

Data and Events that Could Move the Euro

The main event for the Eurozone in the week ahead is the meeting of the European Central Bank (ECB) to decide monetary policy, on Thursday at 12.45 BST.

Back in June the ECB said it would discuss a gradual reduction of its QE stimulus programme - otherwise known as "tapering" in the "fall".

Given this will be their last opportunity to announce their tapering programme before the onset of winter most analysts are taking them literally and expecting a detailed announcement.

Currently, the ECB buys 60bn of bonds per month as part of its programme, but most see this being reduced to 40bn for a period of 6 months.

Others expect a deeper cut to the monthly amount - from 60bn down to 30 or 25bn but for a longer duration of 9-12 months, such as Société Genérale's, Chief FX Strategist Kit Juckes, and TD Securities' Chief Macro Strategist Jacqui Douglas.

This, they argue, might be to keep the Euro anchored given recent misgivings that its recent rally might upset growth.

"Last month, the ECB suggested that not all decisions will be made at this month's meeting because the euro was a source of uncertainty but the currency is now trading at 1.18 instead of 1.20 so they should not be as worried," says BK Asset Management's Managing Director, Kathy Lien.

Lien thinks the ECB will opt for a 'dovish taper' by which she means, "cutting bond purchases by only 20B and extend it to September or beyond because they can always adjust it later and right now there's too much political uncertainty."

If she is right, she thinks the Euro will fall in line with most analysts; if wrong and the "ECB marries a more aggressive reduction with hawkish comments from Draghi, EUR/USD will hit 1.20 easily."

On the hard data front, the main release for the Euro will be PMI data on Tuesday at 10.00 BST.

Both Manufacturing and Services PMI's are expected to slip in October, with the former expected to come out at 57.8 from 58.1 and the later to come down to 58.7 from 58.8.

Nevertheless, despite expecting them to fall, IHS Markit who compile the data, view PMI's as broadly falling in line with the steady uptrend in regional growth.

"Both the degree to which output is rising and the extent to which price pressures have intensified are consistent with the ECB starting to rein in its stimulus," says Aw.

"The flash October PMI data will, therefore, play an essential role in gauging the health of the economy as we approach the end of the year, and thereby provide further insights on future monetary policy," added the economist.