Unhedged demand for Eurozone stocks has been a significant driver of Euro gains during the summer months, but an increase in hedging could soon become a headwind.

Foreign investors piling into Eurozone equities have helped drive the common currency’s surge over recent months, but increasing demand for hedges could soon prove a headwind to further gains.

“The more timely ETF flows which we track revealed that there was significant pick-up in demand for unhedged euro-zone equities in Q2 which reinforced the boost for the euro,” says Lee Hardman, a strategist with MUFG. “However, the latest ETF flows reveal some reversal has been taking place over the summer with outflows from unhedged euro-zone equities.

Major equity benchmarks across Europe have notched up high single-digit gains for the year to date, with the DAX in Germany rising 9.4% and the CAC 40 in France adding 7.75%, with foreign buying a key source of demand.

“The stronger Euro could be acting as more of a dampener now on demand for unhedged euro-zone equities. It has recently coincided with more of a grind higher for the euro,” says Hardman.

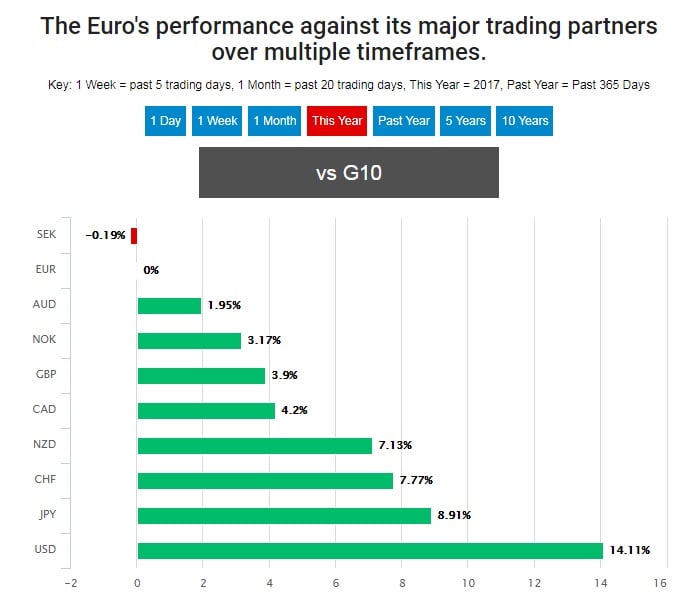

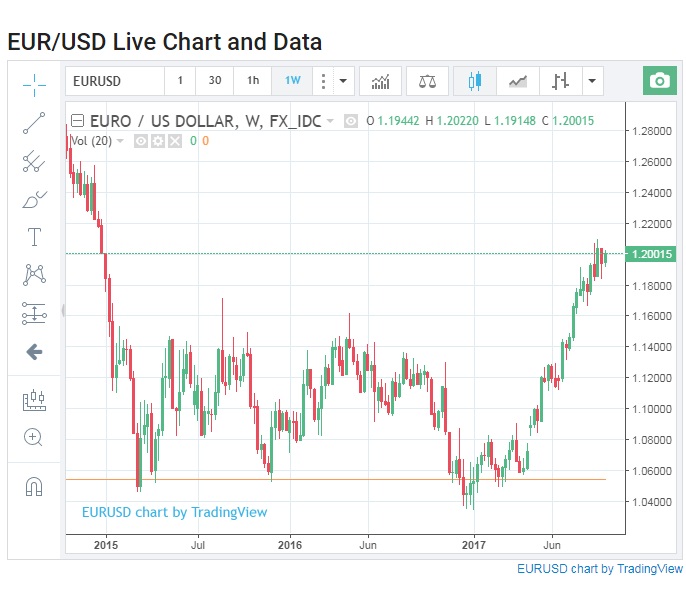

The Euro has gained more than 14% on the US Dollar for the year to date and close to 5% against Sterling. More than half of gains over the Dollar have come since the end of June.

“Investors’ positive reassessment of the euro-zone including improving growth outlook and reduced political risks clearly played a key role in reversing euro undervaluation,” Hardman adds.

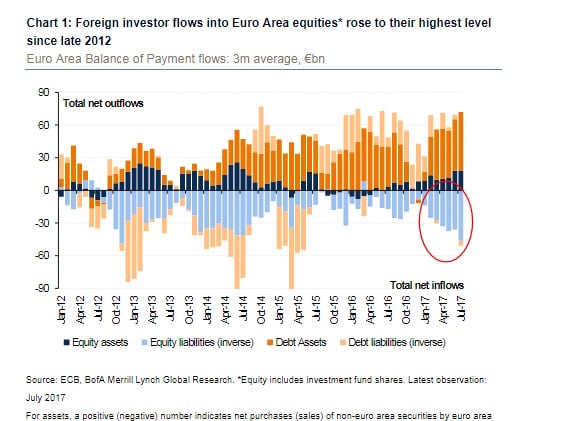

According to the latest Eurozone balance of payments data, referenced in Hardman’s report, foreign investors bought €61.2 billion of Eurozone equities in July.

This took total foreign purchases during the year to the end of July to €338.8 billion, more than double that seen in the previous period, according to Hardman.

“Foreign investor demand for European equities on an unhedged basis has been a consistent theme for much of this year. Indeed, year-to-date and in USD terms, the Euro-Stoxx 50 has outperformed the S&P by a 2-1 ratio,” says Ruairi Hourihane, a rates strategist at Bank of America Merrill Lynch.

Source: Bank of America Merrill Lynch report.

“The size of the equity inflows combined with the surge in the EUR indeed suggests these inflows have increasingly been on an unhedged basis through the summer months,” adds Hourihane.

But with equity-demand a key driver of recent Euro-strength, and that Euro-strength now becoming a driver of increased hedging among investors, the Euro might see some pushback against further strength during the months ahead.

This is because the hedging process for equity investors is equivalent to selling the Euro while buying Euro stocks at the same time.

“Eurozone equity inflows have been a key driver of EUR/USD upside recently but may be fading... Speculators now look increasingly stretched on EUR/USD longs,” says Christin Tuxen, chief analyst at Danske Bank.

However, that said, there is only so much pushback that can come from hedging and not all investors will be expected to hedge their currency exposure as some may also have a favourable view of the Euro in addition to a favourable view of Eurozone stocks.

“In our view, recent price action and flow patterns have confirmed that flows are a key driver in the current ‘normalisation’ environment, which is a key reason we have upped our 12M forecast for the cross to 1.25,” says Tuxen.

Hardman, Tuxen and Hourihane are not alone as other strategists have long been attempting to factor the anticipated impact of this phenomenon into their forecasts for the common currency.

Deutsche Bank recently forecast a significant shift in asset allocation among institutional investors, in favour of Eurozone assets, which could weigh on the Dollar over the coming years. It follows five years or more of investors having held a structurally underweight position in all Eurozone assets.

“Our own flow indicators suggest that central banks were buying EUR through the early weeks of August. We await the August balance of payments data to see if these flows have resulted in any corresponding shift inbond flows,” says Hourihane at BAML.