Our technical studies for the short-term timeframe suggest the Pound to Euro exchange rate is likely to maintain a steady downtrend amidst an atmospher of soft sentiment owing the pervasive sense of political risks arising from Brexit uncertainty.

However, warning signs are also flashing with regards to Sterling being oversold, so this could well be an interesting week for those watching this rate.

Most recently the exchange rate has broken below a trendline and this is an important bearish signal adding to expectations the pair will sink further.

Technical studies observe the market's structure through the use of price charts and offer guidelines of potential future direction.

While forecasting short-term movements in a financial asset is notoriously difficult of late we have found our week-ahead forecasts to be accurate.

We note the MACD momentum indicator is following the exchange rate lower, supporting the downtrend.

Ideally, we would wish to see a break below the 1.0783 lows for confirmation of a continuation down to a target at 1.0700.

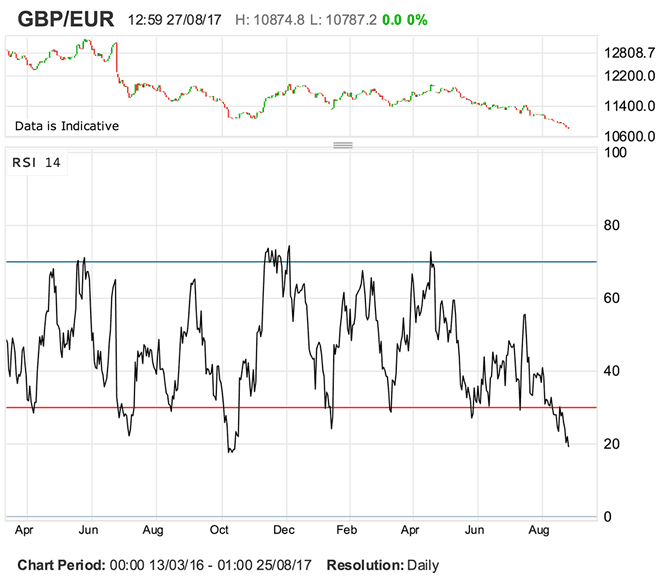

We would warn however that this exchange rate is also oversold. The Relative Strength Index (RSI) on the weekly chart now reads at 29 - a reading below 30 is indicative of oversold conditions.

On the daily charts the RSI reads at 19.3, the last time we saw such a read was back in October 2016. The exchange rate recovered from such oversold conditions and entered a strong recovery that took the market all the way back to 1.20.

Above: The RSI is pointing to oversold conditions.

Could history about to repeat itself?

We would note that the RSI rarely stays below 30, so beware a comeback. The oversold conditions could extend from here, particularly as the market positioning is not yet extreme, as per the latest CTFC data.

But, we would be surprised if a recovery, or at least some consolidation, were not to occur by next week.

Get up to 5% more foreign exchange by using a specialist provider by getting closer to the real market rate and avoid the gaping spreads charged by your bank for international payments. Learn more here.

News and Data for the Pound

It is a thin week for UK data with the only releases of any significance Consumer Confidence on Thursday 31 at 12.05 BST, and Manufacturing PMI, on Friday, September 1 at 9.30, although analysts do not see either as being market moving.

House Price data from Nationwide will also be released at 7.00 on Tuesday, August 29.

But it will be Brexit negotiations that matter for Sterling in the coming week as the EU and UK sit down for their third round of talks.

"The central bank’s ongoing concerns about Brexit, uneven data and the prospect of a stronger U.S. Dollar, kept Sterling under pressure and we believe these same factors will lead to the currency’s continued underperformance this coming week," says BK Asset Management's Kathy Lien.

The U.K. government is sticking to its view that they should not pay a penny more than their legal obligations according to foreign minister Boris Johnson. However, Johnson has also made clear that the UK accepts it has obligations with regards to paying a settlement fee.

So this could be constructive in that the Government is showing some unity of purpose and are notably softer in rhetoric.

"The last we heard, Brexit talks could be delayed until December – 2 months later than planned as disagreements have caused the government to hope for a change in the German government. Germany holds federal elections at the end of September but Angela Merkel is widely expected to win," says Lien.

News that the opposition Labour party appear to be shifting to a much softer version of Brexit, however, could offset the slide in Sterling if it pressures the Government to adopt a similar stance.

Shadow minister for Brexit, Kier Starmer, has set out Labour's revised position in an Observer article this weekend, which has the potential to rattle markets.

Labour's new position is that the UK will keep membership of the Economic and Customs union - but not the political union - during a handover period of 4 years after the official exit date in 2019, with a view to potentially retaining some aspects of membership forever, and negotiating out those which are less desirable.

With markets so negative on Sterling we believe the risks are now to the upside. Specifically, if EU Brexit negotiator Chief Michel Barnier were to say at the conclusion of this week's negotiations that progress has been made, the Pound could pop.

The UK Government's position papers, released over recent weeks, should provide welcome clarity for negotiations. If some good progress can be made over coming days the oversold Sterling might find the fundamental trigger to a recovery.

News and Data for the Euro

The Euro caught a bid late on Friday following European Central Bank Mario Draghi's address to the Federal Reserve Bank of Kansas City's Economic Symposium at Jackson Hole, Wyoming.

Draghi did not mention the Euro's recent strengthening and we warned ahead of the event that failure to do so would be taken by markets as a green-lighting of the strength.

The single-currency popped higher as a result.

"Assuming Jackson Hole doesn't ignite too many fireworks, expect the benign market conditions to extend into next week and the EUR to remain supported," says ING's Chris Turner, who further adds that he does not expect Eurozone inflation data to impact negatively on the Euro even if there is a risk it is soft, because, "the Eurozone macro story - which backs an eventual ECB tapering - remains firm."

As such centre stage in the coming week, is inflation data - CPI - which is out at 10.00 BST on Thursday 31.

Inflation is forecast to show a higher 1.4% rise in August from 1.3% in July, whilst Core Inflation is forecast to rise by 1.2% - the same as previously.

The release is of significance because it could have a major impact on European Central Bank (ECB) policy, as higher inflation will make it easier for the ECB to dismantle its stimulus programme; and a reduction in stimulus would be positive for the Euro, however, a surprisingly high print is probably necessary to change the expected rate of stimulus wind-down, which is unlikely.

The Unemployment Rate is released at the same time as CPI and is forecast to stay at 9.1%.

Manufacturing PMI for August, out at 9.00 on Friday 1, is expected to stay at 57.4.