- Spot Quotes:

- GBP/EUR exchange rate: 1.0968, -0.25%

- EUR/GBP exchange rate: 0.9116

The Pound to Euro exchange rate enters the new week tucked into the folds of an ongoing downtrend driven primarly by investor fears for the economy in light of the UK’s planned departure from the EU.

These have overshadowed comments from European central bankers which weakened the Euro last week and explains the continuation of the current downtrend.

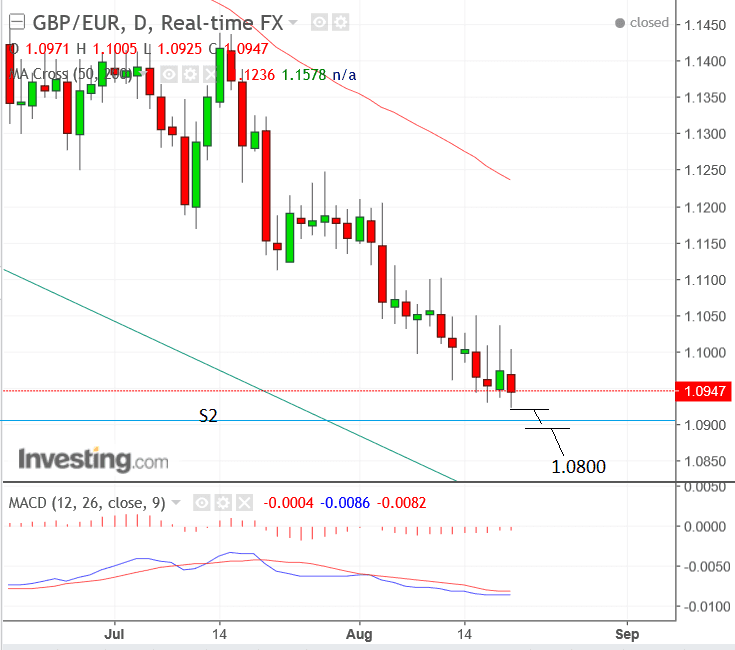

From a technical perspective, our studies note the rate to have reached a new low of 1.0925 on Friday August 18, and whilst the downtrend may have lost impetus over the last two weeks it remains dominant and intact.

We therefore expect it continue, with a break below the lows probably reaching a target at 1.0911 initially, where the S2 monthly pivot level is situated.

Monthly pivots are levels which often act as obstacles to the trend and sometimes even coincide with reversals.

Traders often use them as points at which to enter orders counter to the prevailing trend, and this will probably lead to a period of consolidation at the level of S2.

A break well below the pivot, however, such as would be evinced, for example, if the exchange rate were to fall below 1.0880 could well denote that the pivot had been overcome and the exchange rate was continuing lower.

Such a break would probably move rapidly lower again, to a further target at 1.0800.

Beware Setback for the Euro

Some food for thought.

While the Euro has dominated against Sterling over recent months, there is a suggestion that this strength is actually an impulse within the confines of a longer-term retreat.

“The rally phase for EUR/GBP has been quite resilient over the past several months, but we sense a corrective phase is close,” says a technical note from analysts at J.P. Morgan. "The rally from the April low is still viewed as counter-trend."

Note this analysis from the investment bank covers a longer-term timeframe than the observations made earlier in this piece which cover a short timeframe which is liable to be prone to more volatility.

J.P. Morgan note Sterling-Euro is testing critical support in the 1.0935/1.0776 region.

This level includes the 76.4% retracement of the climb from the 2016 low (October) amid an oversold and bullishly diverging momentum setup.

But, any resistance to a recovery starts at the 1.1099/1.1123 area which represents the August breakdown and 38.2% retracement of the decline from the July high.

J.P. Morgan suggest a break of this resistance should confirm a deeper recovery and a closer test of the 1.1315/1.1436 zone (July high).

Breaks of this area will help define whether a medium-term bullish shift is underway argue analysts.

Get up to 5% more foreign exchange by using a specialist provider by getting closer to the real market rate and avoid the gaping spreads charged by your bank for international payments. Learn more here.

News, Data and Events for the Pound

Brexit debate will dominate in a week that sees second-tier nature being on offer.

The UK is set to release two Brexit position papers this week as it continues to lay out its negotiating stance ahead of the next round of talks, due to start next week. The two new papers are expected to discuss issues surrounding the regulation of goods and data protection.

The data impact from a currency perspective could be minimal but the reactions of European officials might be of note.

"In the coming days we will demonstrate our thinking even further, with five new papers - all part of our work to drive the talks forward, and make sure we can show beyond doubt that we have made sufficient progress on withdrawal issues by October so that we can move on to discuss our future relationship," says David Davis, Secretary of State for Exiting the European Union.

Last week saw the UK publish position papers on the Irish border and proposals for a future customs agreement.

Regarding data, the week starts off with Public Sector Net Borrowing in July, at 9.30 BST on Monday, which is forecast to show the British government borrowing 0.5bn more than it did in July 2016 when it borrowed 6.28bn less.

The Consortium of British Industry (CBI) Industrial Trends Survey for August is out at 11.00 on Tuesday, August 22, with forecasts of the ‘balance’ – of “yes” to “no” responses – expected to rise to 10, from 8 in the previous month.

Thursday is the main day for Sterling in the week ahead from a data perspective, as the second estimate for GDP in the second quarter, is released.

Q2 GDP rose by 1.7% according to the first estimate, and the second estimate is expected to show no-change from this; the Q1 estimate showed growth of 2.0%.

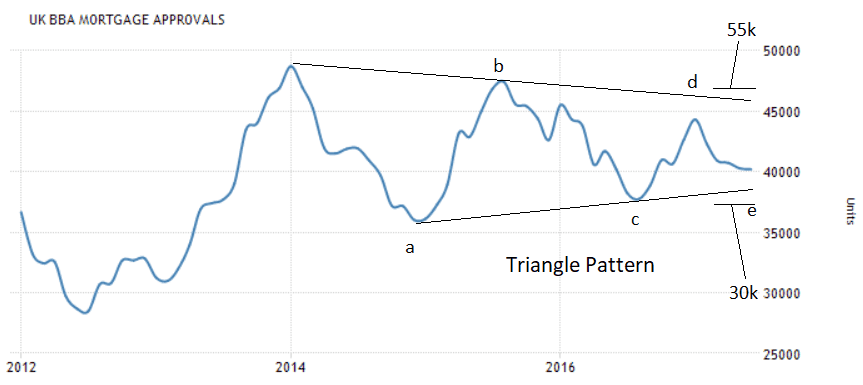

Mortgage Approvals are expected to show 40.2 thousand more approvals in July, according to data from the British Banking Association (BBA) out at 11.00 on Thursday. Some forecasters have stated they will rise to 40.9.

Mortgage approvals have formed a compelling triangle-shaped pattern when seen charted over recent years (see below).

According to research, triangles have a minimum of five component waves, and this pattern has formed fives waves already, labelled a-e, and as such could be complete.

The next move would be expected to be a breakout either higher or lower, however, what is highly probable is a period of high volatility in the not too distance future.

As we noted last month when making the same analysis of mortgage approvals, a reading of above 47,500 would indicate an upside breakout to a target of 55k whilst a reading below 37k would lead to a breakdown to a target at 30k.

Finally, Business Investment is a major release for the Pound, also out on Thursday, at 9.30 BST.

Markets will be following the release closely as Investment has been unexpectedly strong since the referendum when it was one of the things which was expected to be hit hardest, given companies need certainty before making investment commitments.

If investment continues to remain robust that may well help the Pound.

Finally, towards the end of the week the main event for financial markets will be the Jackson Hole symposium in the US, where central bankers will be meeting to discuss monetary policies and the global economy, and where Bank of England governor Carney, may well contribute to the flow of commentary.

Above: Blackstone Futures update on the tight ranges being obeyed by many key FX markets ahead of the Jackson Hole event towards the end of the week. These are the levels to watch.

News, Data and Events for the Euro

The first major release for the Euro in the coming week is the ZEW survey on Tuesday, which asks financial professionals for their views on the economy.

The ZEW index is expected to show a fall from the 35.6 in July to 32.3 according to some analysts in August.

The deputy governor of the European Central Bank (ECB) Vitor Constancio will be making a speech on Tuesday at 13.00, which may yield further insight into the ECB’s thinking around the hot topic of whether the Euro is over-valued, as was suggested by commentary last week.

ECB President Draghi will be making a speech at 8.00 on Wednesday, August 23.

At 9.00 on Wednesday Eurozone PMI’s are released and expected to show a pullback in composite PMI to 55.5 from 55.7.

PMI’s have been strong in the Eurozone so a positive result could push the Euro higher.

Eurozone Consumer Confidence is then to be released at 15.00 on Wednesday.

In the second half of the week, much of the focus will be on what ECB President Draghi says at the central banking symposium in Jackson Hole about monetary policy.

Previously there were expectations that he might use Jackson hole to ‘plant clues’ that the ECB was about to wind down its money-printing stimulus activities, which would be positive for the Euro, however, analysts are less certain now.

Investec's Economist Philip Shaw says:&

“We had thought Kansas City Fed’s Jackson Hole Symposium (Thursday to Saturday) would be a milestone for major monetary policy clues. Mario Draghi was thought to be using the conference as a stage to spell out fresh steps in the outlook for ECB monetary policy.

“But newswire reports suggest that the ECB President prefers instead to entertain a fuller debate on the Governing Council (GC) beforehand. This in itself suggests that the GC remains to be convinced that it should announce its QE tapering plans at the next meeting on 7 September."