The British Pound might have creeped higher against most major currencies in the March to April period, but it is far too soon to call this the start of a long-term recovery argue analysts at one of Europe's largest financial services providers.

The team at UniCredit Bank A.G are the latest to visit their models on the British Pound and the view is not one that will necessarily be welcomed by those hoping for a stronger Pound.

“While the biggest adjustment in Sterling is likely behind us, we think it is too early to turn bullish on the GBP,” says Kathrin Goretzki, CFA, FX Strategist at UniCredit Bank A.G. in London.

The UK’s vote to leave the EU was a blow to the British currency that needs no introduction.

Since the referendum, the GBP has depreciated by 12% on a trade-weighted basis, its biggest fall within a year since the financial crisis.

However, since October the currency has stabilised and adopted a more sideways-orientated direction.

But of course, all we and the majority of our readers are interested in is ascertaining where the UK currency is going next - will the currency suffer further Brexit-blows and fall lower or will a long-overdue recovery start soon?

Above: The worst is behind the Pound which is ‘bouncing along the bottom’ against the Euro. But a notable recovery is forecast to remain elusive

The Balance of Payments Data - Improvements to be Short-Lived

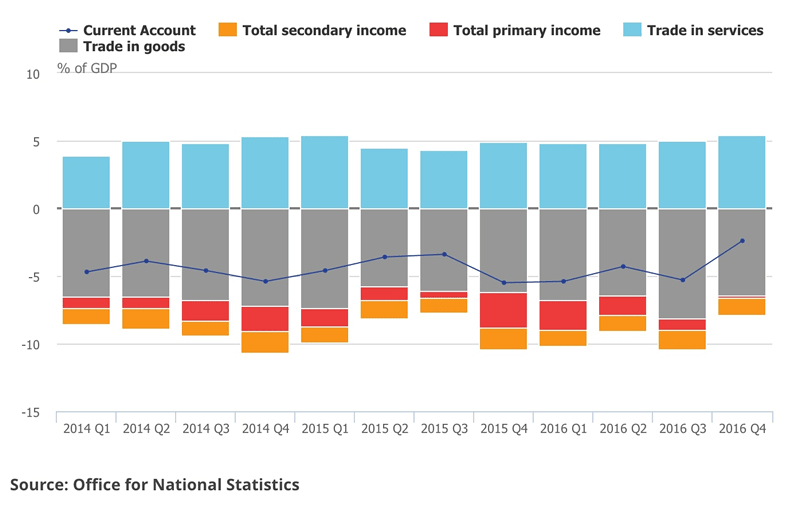

There is one economic concept that is central to foreign exchange - the Balance of Payments.

The UK has long had a large current account deficit as a feature of its Balance of Payments profile owing to the UK importing more than it exports.

If you import more than you export it goes that the currency must fall. But, the UK has also been a destination for foreign investment and these inflows have been a saving grace for Sterling which has historically commanded a higher value than its bank account with the rest of the world implies.

Foreign exchange analysts are in agreement in believing the uncertainty of Brexit will restrict those foreign investment flows and add downward pressure on the currency which must adjust.

Indeed, UniCredit have long forecast the Pound to Euro exchange rate to fall to 1.1111 as a result of reduced investor inflows.

But the Balance of Payments Picture is Improving, or is it?

So - if the UK can reduce its current account deficit it will not be so reliant on foreign inflows and the currency would understandably be more stable. Incidentally this is exactly the kind of adjustment Australia is witnessing at present as it undergoes something of an export boom. The implications are a more stable AUD going forward.

On this front the news for the UK is good - the most recent Balance of Payments data shows the UK has reduced its current account deficit.

UniCredit give the following take-aways from the most recent data:

1. Net direct investment flows into the UK surged, in particular in 4Q16.

2. Total net portfolio flows into the UK remain positive but have weakened since the Brexit vote.

3. Dynamics differ depending on the type of asset class and the investors’ home country (foreign vs. UK investors)

But, looking ahead UniCredit are sceptical that this positive shift in investment inflows will last and therefore see no reason to back a recovery in the Pound.

With regards to the surge in foreign investments, analysts at the Italian bank believe the increase in second half of 2016 reflects nothing more than volatility.

They reckon firms may have accelerated the finalisation of some projects that were already in the pipeline – “it should not be seen as evidence of a more-positive investment climate surrounding the UK on the back of the Brexit vote,” says Goretzki.

Furthermore:

“The long-term investment horizon also implies a long planning phase. It is well possible that Foreign Direct Investment occurring in 2H16 was related to projects that had already been in the pipeline and were maybe accelerated in light of the GBP’s depreciation.”

However, new research published by Market Financial Solutions on April 7 has revealed that investment intentions amongst firms remains robust.

The findings of a survey of 1000 UK investors has revealed that just 9% of UK investors think the onset of Brexit negotiations will derail their investment plans over the next two years while 39% - the equivalent of 11.5 million investors - see the next 24 months as ample opportunity to execture a short-term investment strategy.

However, UniCredit observe that portfolio flows - which have long supported the Pound - indicate that the prospect of Brexit has negatively affected investors’ perceptions with regard to the UK’s attractiveness as a place to invest.

“Inflows continue to exceed outflows but less than they did over the previous year, indicating a turn in the trend of net UK portfolio liabilities,” says Goretzki.

Having pored over the latest data UniCredit conclude that it looks likely that net Foreign Direct Investment and portfolio flows into the UK will deteriorate from 4Q16’s levels.

“Given the long-term correlation between the portfolio balance and GBP, this is generally negative for Sterling,” says Goretzki. “The latest BoP data provide no reason for investors to adopt a positive stance towards Sterling,”

Pound Forecast to Stay Lower for Longer

Based on the fundamentals of the UK economy, expected interest rate levels and Balance of Payment dynamics UniCredit have told clients they are sticking to their guns when it comes to their forecasts for the Pound.

UniCredit forecast the EUR/GBP exchange rate to be at 0.89 by mid-2017 from where it should fade down to 0.88 by end-2017. The exchange rate rises to 0.89 by the end of March 2018 before peaking at 0.90 in mid-2018.

From a Pound to Euro exchange rate perspective this equates to 1.1236, 1.1363, 1.1236 and 1.111.

There is a disclaimer though.

“The uncertainty surrounding our forecasts is unprecedented – since economic prospects will depend crucially on the future of the UK’s relationship with the EU in the long-term,” says Goretzki.

To get a sense of just how uncertain the outlook is for the Pound it is worth reading our report covering research from another Italian bank - Intesa Sanpaolo - who this week warned that the type of deal reached with the European Union will deliver some notable moves.

Should the UK and EU fail to agree terms and the UK finds itself in a ‘no deal’ scenario then Intesa Sanpaolo warn the Pound could go below its post-referendum lows.

However, an amicable and timely deal could well see Sterling recapture a good chunk of the ground it has lost following the EU referendum.

Also seeing little upside prospects against the Euro are the team at Capital Economics who this week released a note that was actually quite optimistic on the Pound’s prospects.

Capital Economics have their sights set on the Bank of England and believe the Bank are likely to raise interest rates as early as the second quarter of 2018 - well before markets are currently expecting.

This is expected to allow the Pound to recover against the Dollar. However, the Euro is also expected to rally in 2018 and this will ultimately neutralise the Pound’s advantage.

Their end-2018 Pound to Euro forecast is at 1.18 which suggests the recovery in Sterling is more or less neutralised by the recovery in the Euro against the Dollar.