UBS see no reason to doubt the continuation of the Euro-supportive German current account surplus.

- Pound to Euro exchange rate: 1.1155

- Euro to Pound exchange rate: 0.8965

- Euro to Dollar exchange rate: 1.0916

A nation's Current Account (CA) describes the difference between the amount of money coming in and out of a country. It is, in essence, the country's bank balance with the rest of the world.

It is therefore the fundemantal underpinning of a currency which is in turn a reflection of the demand and supply of a country's goods and services with foreign partners.

The balance of exports and imports and the balance of other income flows together make up the CA.

If there is a surplus in the CA it means the country exports more goods and services than the it imports and/or that it makes more money from its foreign assets than foreigners make from domestic assets.

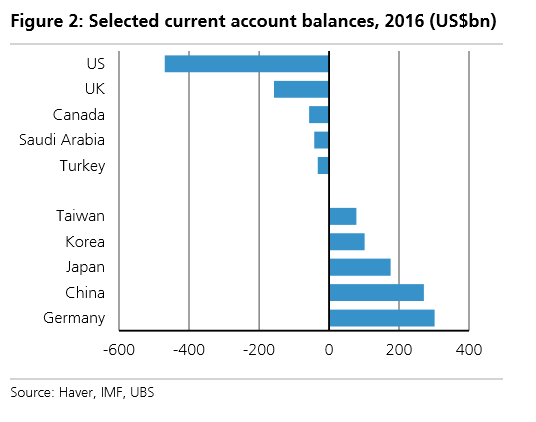

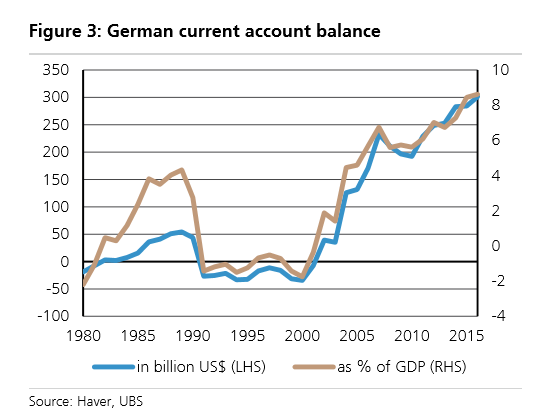

In the case of Germany both of these components of the CA are positive, resulting in the largest CA surplus in the world, at $300bn, or 8.5% of GDP.

But it hasn’t always been the case, back in the not too distant 90’s the CA was negative or in deficit.

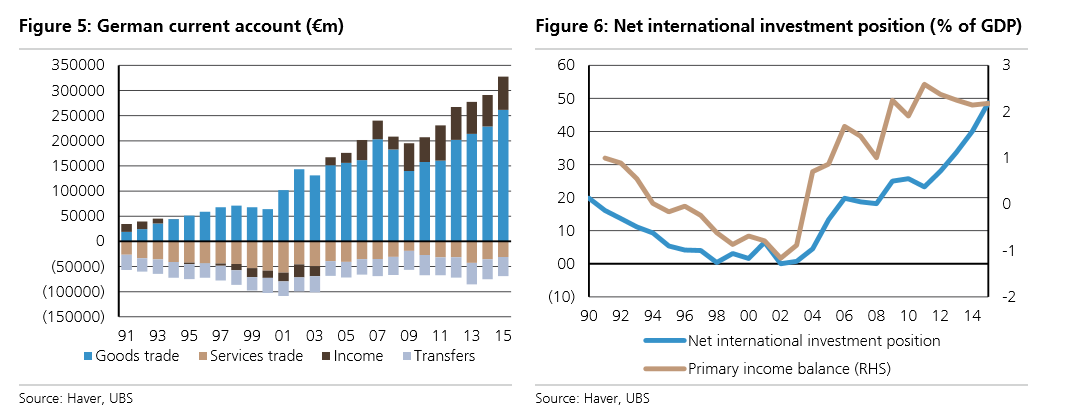

It was only really after the millennium that it started to rise, and the main factor was the income earned by Germans from foreign owned assets.

“Another important factor, accounting for around 20% of the rise since 2000, is rising income flows – basically the return on investment abroad.”

During the 2000s it increased sharply as domestic reforms saw improvements in German competitiveness with the Hartz labour reforms being cited as a key driver.

Also driving the outperformance were the booms in peripheral Eurozone economies, which have since been proven to have been unsustainable.

UBS’s Felix Huefner also describes a self-reinforcing feedback loop which leads surpluses to be reinvested into more foreign assets, which appreciate and return income, which are then reinvested abroad, and so on.

“Income flows have increased from around zero in 2000 to 2% of GDP today, as the stock of German foreign investment has increased substantially, reaching close to 50% of GDP now after years of current account surpluses, and thus foreign asset accumulation,” says Huefner.

And, as these incomes are repatriated the demand for Euros is increased.

Another factor in the accumulation of CA surpluses is more frugal corporates who are reluctant to spend money, particularly domestically.

“A lack of investment in Germany by corporates is the main factor, explaining more than half of the increase in the current account surplus.

“Instead of borrowing to invest (as during the 1990s), German corporates became net savers in the 2000s,” says the UBS Economist.

Indeed, this also goes for the government, which is now a net saver too.

Whilst corporates are beginning to invest more, UBS see it as unlikely that there will be sufficient change in culture for investment to be enough to lower the CA surplus effectively.

Another method of reducing the surplus is to increase domestic consumer spending and demand.

A trend towards more private consumption is already up and running, and has shown consumption increase by 10% since Q1 2008, it is the corporate investment element which is the laggard and is causing the surplus to grow.

“What could induce a more pronounced swing in the CA balance?

“We think a combination of more fiscal spending – notably on infrastructure investment – and structural reforms, such as deregulation of product markets and of employment contracts, could provide the basis for corporates to invest more domestically,” suggests UBS’s Huefner.

The Eurozone CA surplus is a major reason for the Euro exchange rate’s continued resilience, and given no change to the dynamic is likely according to UBS this strengthening ingredient in the single currency’s valuation needs to be respected accordingly.