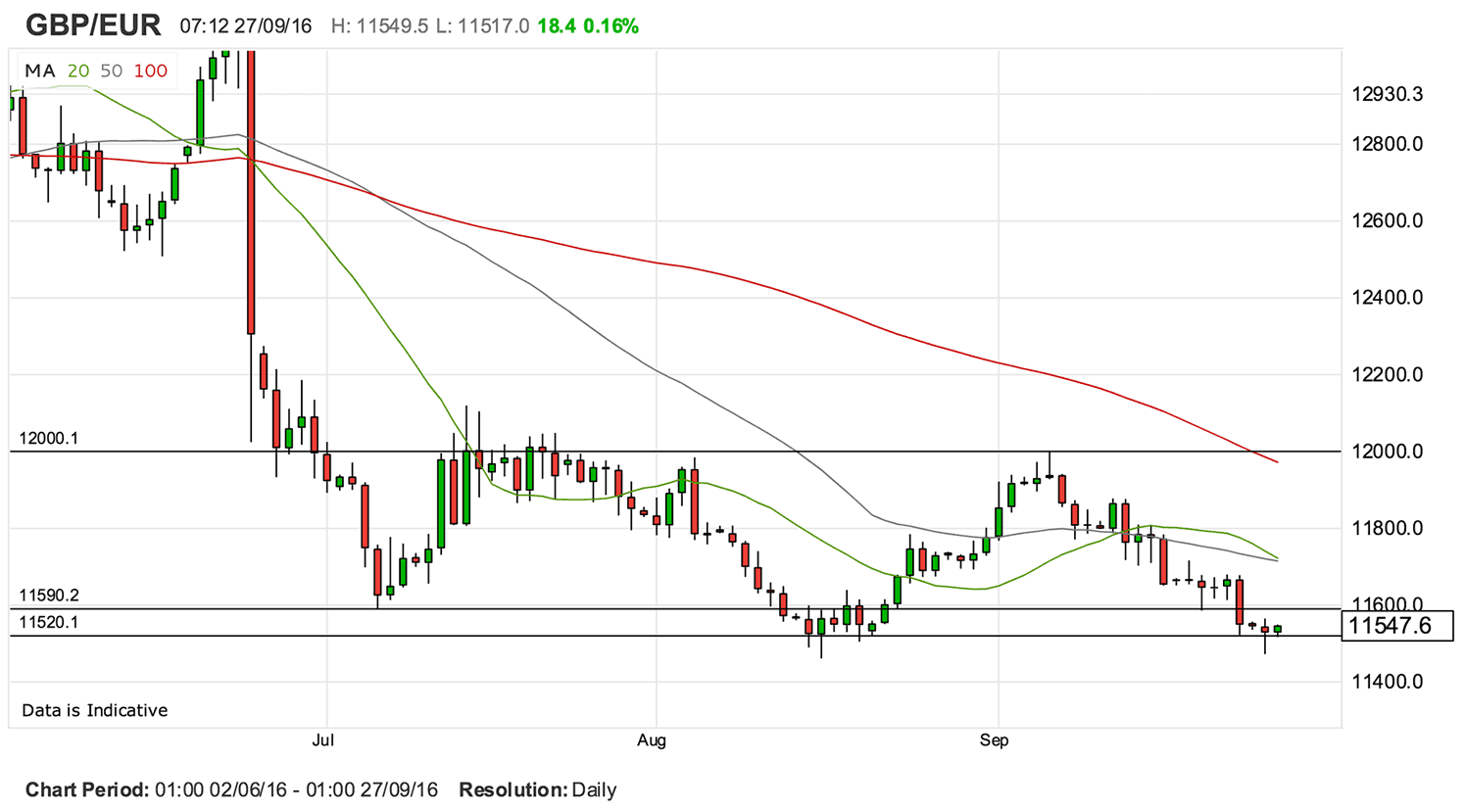

Pound Sterling has managed to avoid closing below a key support level against the Euro again, which leaves us entertaining a potential relief rally that could even take in 1.20.

- Pound to Euro exchange rate today (27-9-16): 1.1559, September's best GBP/EUR rate: 1.1999

- Euro to Pound Sterling exchange rate today: 0.8653, September's best EUR/GBP rate: 0.8699

- Deutsche Bank shares fall to record low, this hits the Pound harder than the Euro

- German Ifo Business Climate data improves markedly in September

Sterling fell to as low as €1.1472 on Monday the 26th of September amidst a fresh bout of British Pound selling pressures.

There were no GBP-specific headlines driving the move, rather traders took their cues from international factors - namely German business confidence and a broad-based risk-off tone that hung over global stock markets.

Crucially however, Sterling failed to close below the key 1.1520 level.

This is important as it reinforces the strength of this support zone - the currency has not closed a single day below this point since the Brexit vote:

There is therefore significant buying pressures here and if we get a repeat of the mid-August period the GBP/EUR could well bounce towards the top of its post-referendum range towards 1.20.

If Sterling can remain above 1.1520 at today's close we would be more confident in calling a bottom to the selling pressure for now.

Any hesitancy here would allow Sterling to be better placed heading into month-end where rebalancing flows could prove supportive. And with October around the corner a few positive data points could also provide the relief required to target 1.20.

Ultimately though, the Euro Retains the Advantage

Despite the charts telling us there is the potential for a recovery, we must of course remember that momentum favours the Euro.

The single currency hit a fresh monthly best against the Pound on Monday following the release of stronger-than-forecast German data.

The Ifo Business Climate index rose to its highest reading since May 2014 in September, driven by improving business sentiment, particularly amongst manufacturers.

"We consider the Ifo expectations a useful indicator for future capital spending. The strong increase in expectations in September – if it’s more than just volatility – suggests that capex spending will recover from the weak performance in Q2," says Holger Sandte at Nordea Markets.

Latest Pound/Euro Exchange Rates

| Live: 1.1592▲ + 0.14%12 Month Best:1.1968 |

*Your Bank's Retail Rate

| 1.1198 - 1.1244 |

**Independent Specialist | 1.143 - 1.1476 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

There is another driver of GBP/EUR weakness - and that is Deutsche Bank whose share price has hit a record low. The bank the IMF described as the biggest systemic threat to global finance is in trouble.

You would expect this to be a negative for the Euro; but you would be wrong. We look at why Sterling is under more pressure than it's continental cousin here.

Ahead of the new week we warned that the now ingrained short-term down-trend in the GBP/EUR conversion will probably extend over coming days based on our studies of the pair.

So while longer-term charts point at the prospect of a relief rally, shorter-term charts advocate for further declines.

As can be seen in the four hour chart below, Sterling continues channelling lower and basic trend observations suggest we must favour a continuation of the move:

The MACD momentum indicator has crossed over its signal line providing a strong bearish signal - this is circled in the bottom panel in the graphic above.

A break below 1.1440 would then probably see an extension down to the next target at 1.1400.

Such a move would confirm the expectations held in our recently-published report on Danske Bank forecasting a decline in GBP/EUR towards 1.08.

"The British Pound continues to look bearish and macro capital flows remain negative the Pound at quarterly, monthly and weekly chart level. A breakdown through the recent lows on the daily chart could open the door to further significant declines," says Phil Seaton at LS Trader.

UK GDP Data is Key Economic Release this Week

Friday September 30 sees the release of the most significant data for the pound, this week, in the form of the first revision of second quarter GDP.

The preliminary result already released, surprised to the upside, coming out at 2.2% rather than the 2.0% forecast, but on Friday we shall see if that upbeat result holds.

Although it does not cover much of the period after Brexit, and is therefore not representative of the impact of the referendum, it still reflects the high degree of uncertainty prevalent in the run up to the vote, and so is some sort of barometer for how the economy coped under uncertain conditions.

Second quarter Business Investment is also out on Friday and will also be closely watched by analysts trying to make sense of how well the economy has managed with the uncertainty stemming from the referendum – again in the run up to the vote in this case rather than afterwards.

Common sense dictates that Business Investment would fall in the run up to the referendum as many businesses would have delayed investment decisions on major projects until after the vote, however, Friday’s data will tell for sure.

There is a possibility of a surprise to the upside since data has up until now, more often than not, beaten expectations which were tilted to the downside for the referendum period.

Nationwide house price data is the other major release on Friday, whilst BBA Mortgage Approvals data, out on Monday (September 26) is a major release for the week.

Fundamental Analysis: Euro Forecast to Retain Positive Bias

For the euro the main data releases in the week ahead is CPI data on Friday (September 30).

This will be the preliminary reading for Inflation in September.

Currently analysts expect a 0.4% rise in inflation yoy, from 0.2% previously.

The Eurozone Unemployment rate is also published on Friday, with a fall of a basis point to 10.0% on the nose, forecast.

The euro is still supported by several major fundamental drivers, the first of which is the inability of Eurozone banks to ‘recycle’ funds they generate as a result of the region’s current account surplus.

The Current Account surplus is mainly due to the Trade Surplus which is major component of the Current Account.

The Trade surplus is due to the weak euro increasing exports and reducing imports.

Eurozone banks cannot recycle the surplus as they are more cautious about lending due to the high number of non-performing loans (NLPs) they have on their books.

The super-low interest rates, and negative deposit rates in the Eurozone are another reason for their disinclination to lend as it is not very profitable for them.

This keeps net demand for the euro positive.

The euro is further supported by the back-flow of funds from the money the money which has been leant abroad.

Low interest rates in the Eurozone make the euro a particularly attractive funding currency for investors seeking to borrow cheaply in order to invest in riskier higher yielding debt, such as characterises most emerging market debt.

However, when global uncertainty weighs on the outlook for emerging markets this can be the trigger for an unwinding of those euro sponsored investments, leading to a sudden back-flow of repatriating euros.

This back flow further increases euro demand strengthening the currency.

The next driver for euro strength is the ECB’s decision to pull-back from increasing stimulus and adopt a more data-driven, wait-and-see stance.

The final major factor in support of the euro is the steady growth being shown by the region.

A major negative factor against the euro, however, is the political instability in the region, and the fact there are several major elections in 2017, which could lead to further erosion of the EU.

As far as the pound goes, the main source of strength of weakness will come from negotiations for Brexit and the resulting probable trade deal which will emerge from that, and how well the economy holds up in the atmosphere of uncertainty in the run up to a final deal.