Forecasts suggest that while the sterling may stage a recovery in the near-term the potential for levels around 1.44 to be reached are limited.

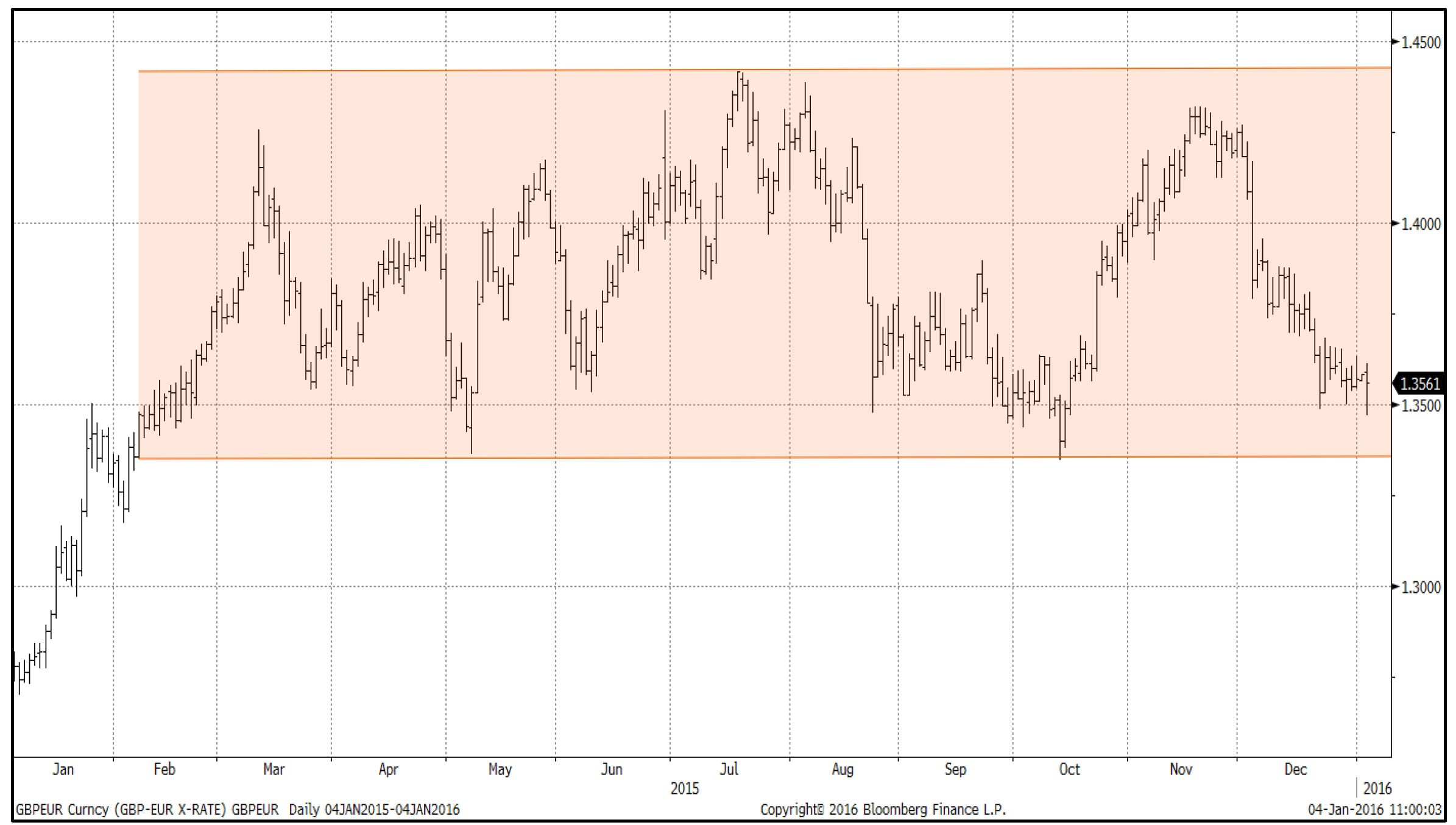

Sterling enters 2016 having advanced against the euro for the second year in a row (+5.3%) while haiving advanced for the sixth year out of the last seven.

Can the long-term trend higher in GBP/EUR continue though?

We see a number of forecasts suggesting that any gains that will be forthcoming are most likely to occur towards the start of 2016 which hints at a multi-year best being achieved within weeks.

It does of course depend who you listen to as some forecasters are turning increasingly bearish on the British pound which could mean the best has already passed us by.

Those with looming international payments will be conscious of the fact that sterling/euro’s best exchange rate for the year was achieved all the way back in July, at 1.4399 and any suggestion that higher rates will come will be welcomed (keep reading!).

The continuing recovery in the Eurozone economy could see the euro make a steady recovery while the pound will unlikely receive much-needed support from the Bank of England in the form of interest rate rises.

Inflation in the UK is simply too low to warrant such a move.

Latest Pound/Euro Exchange Rates

| Live: 1.174▲ + 0.08%12 Month Best:1.1752 |

*Your Bank's Retail Rate

| 1.1341 - 1.1388 |

**Independent Specialist | 1.1576 - 1.1623 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

The major concern for sterling though is the referendum on the UK's continued membership of the European Union, due towards the Autumn.

This is the central risk scenario for sterling in 2016, but expect the lion's share of any weakness to come in much closer to the actual event - as was the case with the Scottish referendum.

Declines are Slowing

The pound has been in decline against the euro since the start of December - where rates above 1.42 were once available now those with outstanding international payments are now having to do so from around 1.35.

That 1.35 figure is key as it appears to be offering support to the conversion - at no point over the course of the past 2 months has the pound fallen below here.

The level coincides with the 0.74 resistance point in the EURGBP - we note that the euro bulls just don't have the stomach to buy the shared currency above this point.

“Given that there is little in the way of consensus as to when the rate-tightening cycle will begin in the UK this period of uncertainty is understandable, although one would expect to see the fundamentals reassert themselves before too long – and that should be enough to keep the pound above its October low, at 1.34 or so,” says Bill McNamara at Charles Stanley.

AFEX: More Gains for GBP-EUR are Possible

Those wanting a stronger sterling will take heart from the first analysis of 2016 offered by currency risk specialist Lucy Lillicrap at AFEX.

“Despite a maturing macro bull trend here the current/recent configuration still looks more obviously corrective than trend-like which suggests GBP prices still retain the potential to test the top of the recent range at 1.4400 in 2016 before an important top can be confirmed,” says Lillicrap.

Note though that any accelerated loss of 1.3250 would argue this awaited reversal has been posted already.

Otherwise, despite risk for an extension to 1.3400 or so first, a subsequent rally back though 1.3700 will probably infer an interim (i.e. early 2016) floor has been put in place suggests the strategist.

Yuan Devaluation Could Aid GBP

News mid-week that the Chinese authorities have devalued their currency could aid sterling it is argued.

ING Bank’s Christopher Turner alludes to this, when accessing the implications for the Euro of Pboc’s recent moves:

“We would also add that CNY has a greater weight in the EUR than USD trade weighted index.

That means the ECB rather than the Fed will have a greater interest in a weaker currency should China devalue further.”

Does this development signal a new, negative, path for the euro in 2016?