- GBP/EUR path lower closed off by EUR/USD rally, TWI connundrum.

- EUR rally, USD depreciation lifts EUR TWI, puts GBP & JPY in play.

- JPY weighting unlikely enough to enable further GBP/EUR declines.

- Easing pressure on EUR TWI demands GBP/USD, GBP/EUR gains.

Image © Adobe Images

- GBP/EUR spot rate at time of writing: 1.1080

- Bank transfer rate (indicative guide): 1.0794-1.0872

- FX specialist providers (indicative guide): 1.0916-1.0982

- More information on FX specialist rates here

The Pound-to-Euro rate advanced Friday after being pulled higher by GBP/USD in moves that were necessary to keep the Euro-to-Dollar rate afloat, given a European trade-weighted-index conundrum that may have closed off Sterling's path lower from 1.10 for the time being.

Pound Sterling had been almost listless until mid-morning hours Friday when a 0.25% almost doubled the Pound-to-Dollar rate increase seen over the course of the week, triggering a tentative increase in the Pound-to-Euro exchange rate that is an amalgamation of GBP/USD and EUR/USD.

That pulled the Pound-to-Euro rate out of the red for the week but wasn't enough to afford it annything more than a meagre 0.06% increase for the period, which is symptomatic of price action that has otherwise bestowed other European currencies with handsome returns against the Euro and more so against the greenback.

At the heart of this price action on Friday is a Euro-to-Dollar rampant rally that could easily come to be viewed in hindsight as another folly for European financial markets, and the impact it's having on the trade-weighted version of the Euro. That's to say strength of the single currency relative to the counterparts who matter most economically.

"The EU Recovery Fund is an important step, but not a game-changer, in our view. We remain concerned about the rising debt levels in individual Eurozone economies," says Athanasios Vamvakidis, head of FX strategy at BofA Global Research. "We see balanced USD risks in the short term, with a number of offsetting forces...On Brexit, our base case is no transition extension and a bare-bones free trade agreement by year-end."

Above: Pound-to-Dollar rate shown alongside GBP/EUR (orange line, left axis) and EUR/USD (black line, left axis).

The Euro-to-Dollar rate has exploded higher in the last month, demolishing everything in its path including technical resistance levels and a number of emerging market currencies, but poor old Pound Sterling had barely moved and the safe-haven Japanese Yen had fallen alongside the Kiwi Dollar.

This has lifted the trade-weighted Euro and so far at least, fixed a trade-weighted equivalent of a hangman's noose around the neck of a runaway Euro-to-Dollar rate, but still the single currency retained an upside impetus on Friday even as newswires were awash with worries of a European second wave and amid a strong U.S. retail sales story.

"France vowed 'reciprocal measures' after the UK shut its travel corridor with France due to the spike in new COVID-19 cases. But there are no implications for FX, right? Think again. Quarantines could be an effective tool for devaluing a currency under the auspices of something that is seemingly remote from the sphere of monetary and FX policies," says Stephen Gallo, European head of FX strategy at BMO Capital Markets.

Europe's single curency is among the largest of heavyweights in the currency market boxing ring but during times when the Eurozone trade-weighted currency has risen to extremes over and above those seen in the last big rally back in 2017, brain might be found prevailing over braun.

Above: Pound-to-Dollar rate shown alongside GBP/EUR (orange line, left axis) and EUR/USD (black line, left axis).

Falls in GBP/USD and GBP/EUR might feeel to the above referenced large heavyweight, like big swinging hooks from Mike Tyson in the final minute of a 12-round slugfest. More so if they come alongside increases in USD/JPY, exactly as they often did this week.

"The USD is under pressure, and the bears are in the ascendancy. However, we do not believe this weakness will persist and in these tumultuous times we find little reason to turn bearish on the USD. Many of the "nowcasts" for USD weakness are simply extrapolations of recent trends rather than forecasts. Many of these will wane. We remain positive on the USD's outlook against the EUR and GBP," says Daragh Maher, North American head of FX strategy at HSBC.

Falls in GBP/USD and GBP/EUR would provide an additional lift to the trade-weighted Euro and more so when combined with gains in USD/JPY, which would mean EUR/USD has to burn through more fuel in order to achieve what would then be even less sustainable gains. Burn through more fuel the single currency did on Friday, keeping the upward EUR/USD bias intact after having dragged the British exchange rates higher and weighed heavily on USD/JPY.

Whatever else the continued upside bias in the Euro-to-Dollar rate might mean, it also does mean the Pound-to-Euro rate pathway that leads below the 1.10 level is closed to all would-be visitors for the length of time that trade-weighted concerns are a burden for the Euro. That level was some 75 points away Friday and possibly a bridge too far for the TWI even in the event of a sharp correction in GBP/USD or further gains in EUR/USD.

Above: Pound-to-Dollar rate shown alongside GBP/EUR (orange line, left axis) and EUR/USD (black line, left axis).

This is partly because a GBP/EUR fall back to or below 1.10 would raise the Euro TWI further and at the tailend of week where price action is suggestive of it having become a constraint for the market. This dynamic and the ongoing upside bias in EUR/USD are good odds for GBP/USD gains ahead.

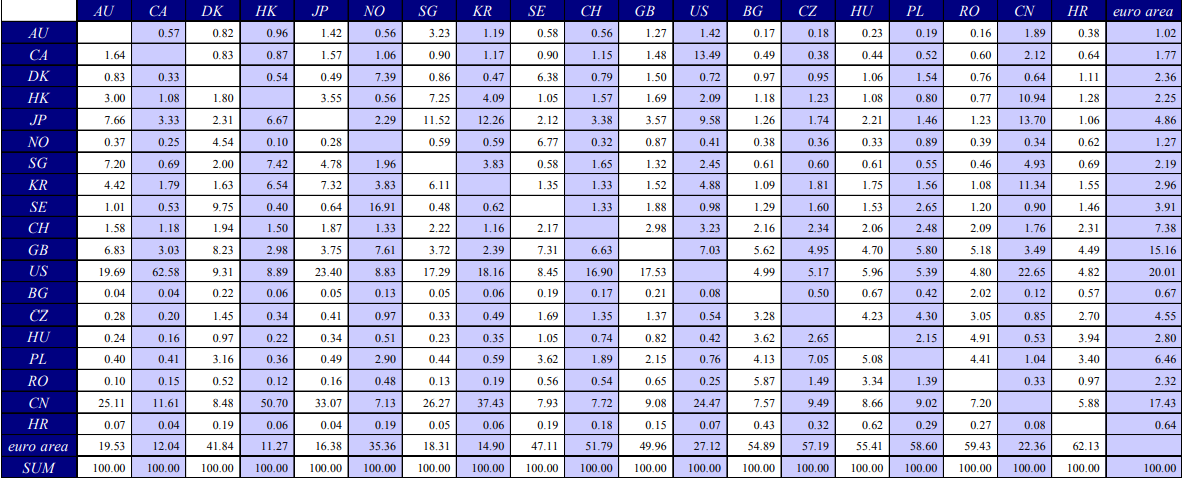

Given the lesser trade-weighting of the Japanese Yen in the Euro TWI, EUR/JPY would need to fall to a much larger extent than GBP/EUR would need to rise in order to constrain the rade-weighted measure of the single currency and simultaneously facilitate further EUR/USD gains. Each of the relevant exchange rates were moving very much in the right direction for this on Friday.

There is another equally as effective but probably much less likely pathway for cultivating a divergence between the trade-weighted Euro and Euro-to-Dollar rate, although it would involve meaningful falls in USD/CNH. That pair turned higher this week and is heavily managed by a Chinese government that might rather have a weaker currency relative to the Dollar than it would the Euro, given the downward spiral in relations between the world's two largest economies. Not to mention Chinese monetary policy.

"To the extent that the RMB is a market-driven variable, the domestic backdrop suggests that any significant moves in USDCNY are likely to be driven by shifts in the 'big dollar', as opposed to in the yuan. The PBoC may also be prevaricating on the issue of its true policy stance," Gallo says.

Above: European Central Bank graph showing respective trade-weightings of the Euro.