Image © Robert Cicchetti, Adobe Stock

- Three more years of 3.75% global growth left in the tank

- Earliest chance of a Fed-led recession is 2020

- BofAML strategists staying long on the FTSE, see Emerging Market weakness as an opportunity

Fears that the world economy is on the brink of slipping into recession purely because the growth cycle is reaching fatigue are misplaced.

Investors should not fear a looming recession, rather they should look at weakness in the market as an opportunity to buy says one of the world's largest investment banks.

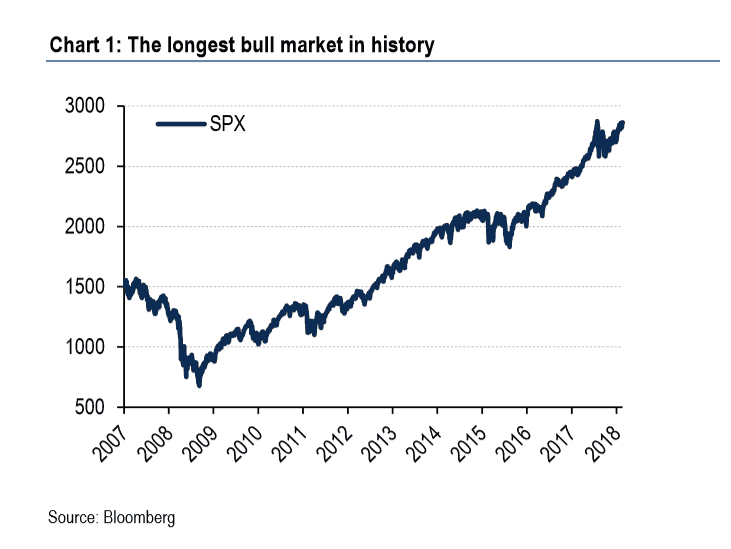

"The big call for investors: how close are we to the end of the cycle?" ask Bank of America Merrill Lynch in their latest cross-asset investment strategy overview, touching on a question being asked by the investment community as they sit atop of the longest bull market in history.

The S&P 500 recently rose to new all-time highs of 2917.50 on Wednesday, August 29, but emerging market stocks continue to exhibit weakness that is now of "recessionary panic levels," note BofAML.

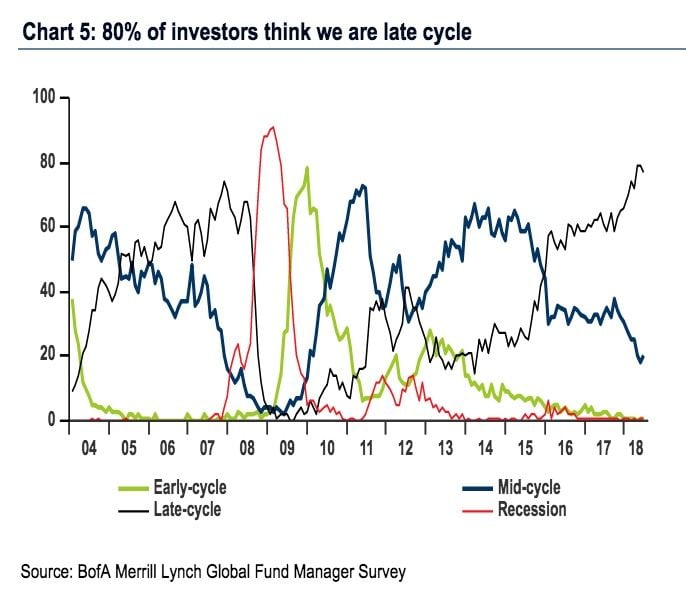

Talk of a 'late cycle' - i.e. that point at which economic expansion ceases - is seen as being particularly pressing for the fund manager community; indeed around 80% of fund managers recently surveyed by BofAML say we are now 'late cycle'.

But, BofAML believe fears of the cycle ending in the near-future are overdone.

Instead, any weakness - emerging markets included - should be considered a pull-back as global equities can achieve new heights before then peaking out in 2020, at the earliest.

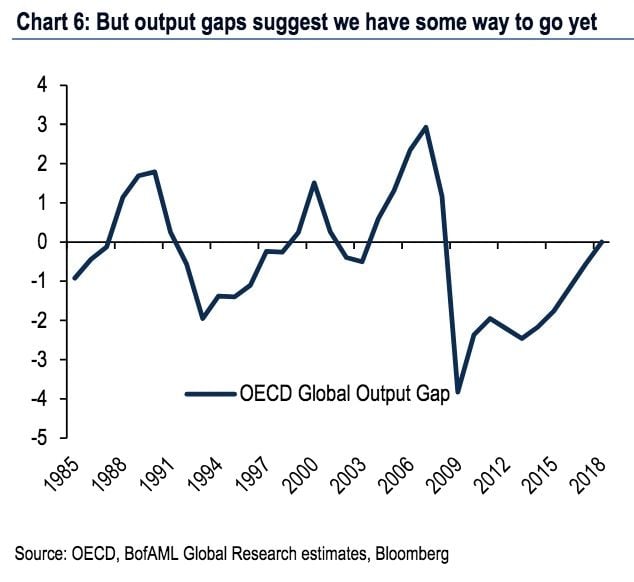

Researchers believe the expansion has further to run having citing OECD data which monitors the global 'output gap', a measures of how much more the global economy needs to grow to fulfil its estimated potential. (What is the output gap?)

Late-cycle recessions normally only occur when the output gap has closed and monetary conditions are tighter, but at the moment the gap is still open and not forecast to close until year end.

"Historically the peak in the cycle is somewhere between 1.5% and 3% positive, as it normally requires some inflation to get central banks to hit the brakes. Even reaching the lower end of that band would require three more years of 3.75% global growth," say BofAML.

Concerning the US economy, BofAML note that while the US expansion is more advanced, the picture is similar, with economists thinking that the US output gap has probably just closed.

"Again, historically it has taken a positive output gap (and hence rising inflation) to get the Fed to tighten enough to send the economy into a recession," say BofAML.

The most recent pull-back in Emerging Market assets is meanwhile seen as being a pullback within the upward trend, rather than a major market turning point.

These accidents are a common occurrence in late-cycle corrections but are not normally the trigger for a major recession, rather they precede resumptions of the uptrend.

"It is also often the case that risk assets recover from those accidents until the Fed finally punctures the cycle, at which point it is game over and all investors have to head for defensive assets," says BofAML.

The Fed's cautious stance on further monetary tightening - which means raising interest rates - is further proof that even the relatively mature US cycle has higher to go.

"Our economists think there is plenty of momentum in the US economy, and, with real short rates only turning positive from late this year, it is unlikely that Fed policy will be sufficiently tight to generate a US downturn before 2020 at the earliest," say BofAML.

And if anything, dips in the market should be seen as buying opportunities.

"Equity markets and risk assets in general tend to peak only six months or so before an economic downturn, which would suggest this pullback in risk assets is one that investors should buy into," say BofAML.

BofAML have also confirmed they are staying long on the FTSE even if the strategy has struggled over recent weeks.

"It's worth noting that UK equities have outperformed other non-US markets (if not the US) in-line with the typical pattern associated with weaker GBP. In the meantime our strategy of rolling up our hedges into strength has kicked in this month with our 7600-7300 put spreads now in the money. We have also rolled our hedge against a bounce in sterling to 1.32-1.40 over a 3 month horizon," add BofAML.

Emerging Market Equities are in a Sweet Spot for Buyers

For those brave enough to invest and savvy enough to join the dots - according to BofAML anyway - now is the perfect time to buy EM equities - since now they are in the 'sweet spot', before the final wave higher.

The fact that the divergence between the US stock market and stock markets in the rest of the world has reached record levels will not be news to anyone following global financial markets.

"Non-US equities are now the most oversold vs the US since the Global Financial Crisis, EM equities are back on sub-11x earnings for the first time since early 2016 and EM FX carry is also back at 2016 levels. Meanwhile, our RiskLove indicator is at panic levels for EM," says BofAML.

Yet this information alone tells us nothing about what will happen next. As with all divergences the more important question is which of the two diverging metrics is the 'lead'.

In this case, a bearish interpretation suggests Emerging Market stocks are leading the US market lower; in the alternative bullish scenario the US stock market is leading EM equities higher, inferring EM is likely to start recovering higher soon.

BofAML argue the latter is the case right now, and as such this is a perfect time to buy EM risk.

In their evidence they cite how the MSCI ACWI, a broad global stock index is, "following the non-recessionary path, which seems sensible to us given both the data and the view of our economists that, ex a shock, we should print close to 4% global growth this year and next," says the investment bank.

If there is a risk, it is from China, which is vulnerable to a major slowdown if Trump imposes the extra 25% tariffs on $200bn more imports, says BofAML.

"Our central scenario is one of ongoing solid growth but the risk is that the US/China trade war escalates and Chinese growth slides, pulling global and in particular non-US growth with it."

Ultimately the opposite is likely to happen in the long run anyway, however, as US-China trade talks are more likely to resolve than worsen - going the way NAFTA talks - and Bofa think a full-blown trade war will be avoided.

"We think progress on trade elsewhere will likely be followed in US/China trade eventually," says the bank.