-UK spending to rise as inflation falls from Brexit-highs say Berenberg.

-Tight labour market, rising wages, support recovery in spending growth.

-Household spending is 60% of GDP so rebound may support economy.

© IRStone, Adobe Stock

The UK could enjoy a pickup in growth over coming years even as developed economies elsewhere in the world slow, according to economists at Berenberg Bank, who argued Wednesday that conditions are ripe for a rebound in household spending and that this will support the economy going forward.

UK economic growth slowed to 1.7% in 2017, down from 1.9% in 2016 and 2.3% in 2015, according to Office for National Statistics data. The 2016 fall in growth was tempered by strong consumer spending, which offset slower activity elsewhere in the economy.

The 2017 fall in growth came after the tables turned, with rising activity in other parts of the economy insufficient in offsetting a 0.8% reduction in the household sector's contribution to the annual expansion.

This gave the impression the UK's pending exit from the EU was belatedly having an effect on households, which may have tightened their belts as a result. But economists, as well as other data, have since shown this was not the case.

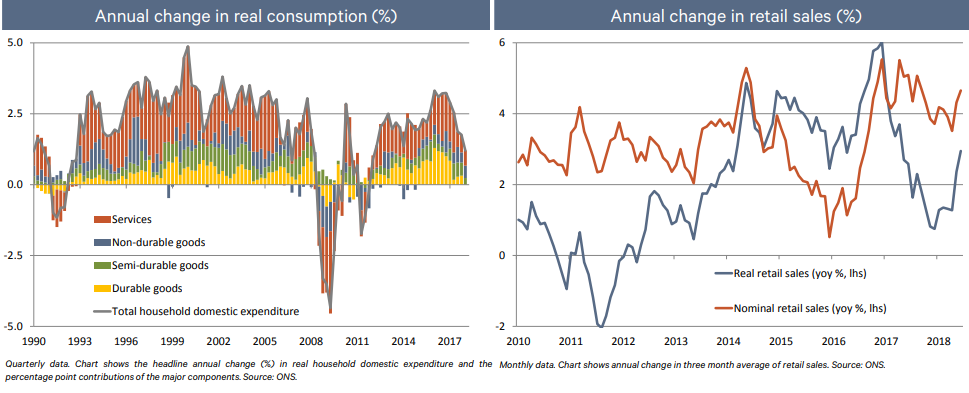

"Partly boosted by cheap oil, real consumer spending growth averaged 2.8% yoy in the 12 months leading up the Brexit vote. But higher import prices from the Brexit-vote related drop in sterling weakened the rate of growth in real consumption to an average of 1.5% yoy in Q4 2017 and Q1 2018," says Kallum Pickering, a senior UK economist at Berenberg.

Much of the post-referendum decline in consumer spending has been the result of an increase in inflation, which has reduced the level of growth reported by the ONS because the official statistics measure changes in spending after inflation has been taken into account.

In other words, they minus a now-higher rate of inflation from the level of actual spending growth in order to get the "real" number. However, this approach masks what how household spending habits have changed before inflation is taken into account.

"The Brexit vote ushered in the end of the consumer boom but nominal demand has remained firm," says Pickering. "Nominal spending growth has increased to a post-Lehman high since the Brexit vote. As prices rose, households simply opened up their wallets more to target the level of real consumption they desired."

Above: Changes in real and nominal retail sales. Source: Berenberg Bank.

As pointed out by Pickering, household spending before inflation is taken into account actually continued to rise following the referendum of 2016.

Similar is true of the broader economy in that, while the rate of "real" GDP growth has slid notably since 2015, growth before inflation is taken into account picked up sharply from 2.8% to 3.9% in 2016, before dropping only to 3.8% in 2017.

This is crucial information for those looking to form a view on the likely trajectory of household spending and economic growth going forward, not least because the rate of UK inflation is now firmly in retreat.

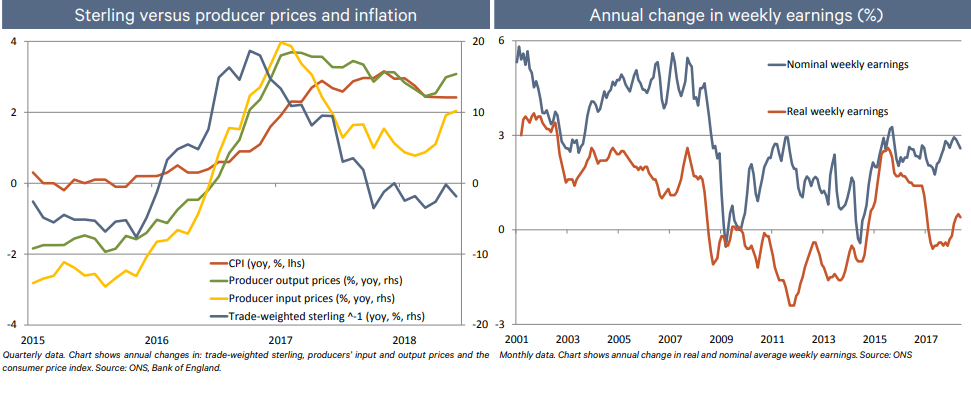

After rising from near-0% at the time of the referendum to 3.1% in November 2017, the UK consumer price index retreated to just 2.4% during the six months to the end of May.

As a result, the "real" rate of household spending growth in the UK should receive an automatic boost over coming quarters, assuming that all other things hold constant. And Berenberg's Pickering sees the household sector receiving an additional boost over coming years too.

Above: Real and nominal income growth in the UK. Source: Berenberg Bank.

"When the UK voted in June 2016 to leave the EU, sterling dropped sharply (by 16% in June-October 2016) as markets priced in higher long-term uncertainty and weaker long-term potential growth for the UK. The lower exchange rate pushed up producer prices and headline inflation. Real wages declined by c1% between June 2016 and February 2018," Pickering writes, in a briefing Wednesday. "The initial shock is fading."

If Pickering is right in what he says next then already high levels of household consumption will be boosted by falling inflation as well as rising wage growth during the quarters ahead, with the latter supported by a labour market that has gone from strength to strength in recent years.

"Nominal wage growth is edging towards 3% – close to a post-Lehman high, but well below the pre-Lehman normal rate," Pickering writes. "Real wage growth is still modest. However, as nominal wage growth continues to pick up, real wages should gradually edge up over time."

There are reasons to think both nominal and real wage growth will continue to tick higher during the quarters ahead too. Not least because the proportion of the population now in employment is at a record high and the unemployment rate is at its lowest since 1973, after having fallen from 5% before the referendum to 4.2% in February 2018.

"If there is still more slack in the labour market, job growth should remain solid. But if slack is limited, firms will begin to offer higher pay to the candidates that are most suited to the firm’s preference of skills, pushing up total wage growth," Pickering writes, after noting how the economy has now created more than 3 million new jobs since 2010.

This bodes well for the UK economic outlook, given that consumer spending is estimated to account for more than half of all economic output.

Above: UK household income as a percentage of GDP. Source: Berenberg Bank.

Advertisement

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here