- Budget deficit below 2% of GDP for first time since 2001.

- NHS spending pledge can be covered with no discernible impact to debt reduction programme

- As long as economy is growing, government can afford to run current deficit say PwC

Above: The UK's Chancellor of the Exchequer, Philip Hammond. Image © Foreign & Commonwealth Office, reproduced under CC licensing

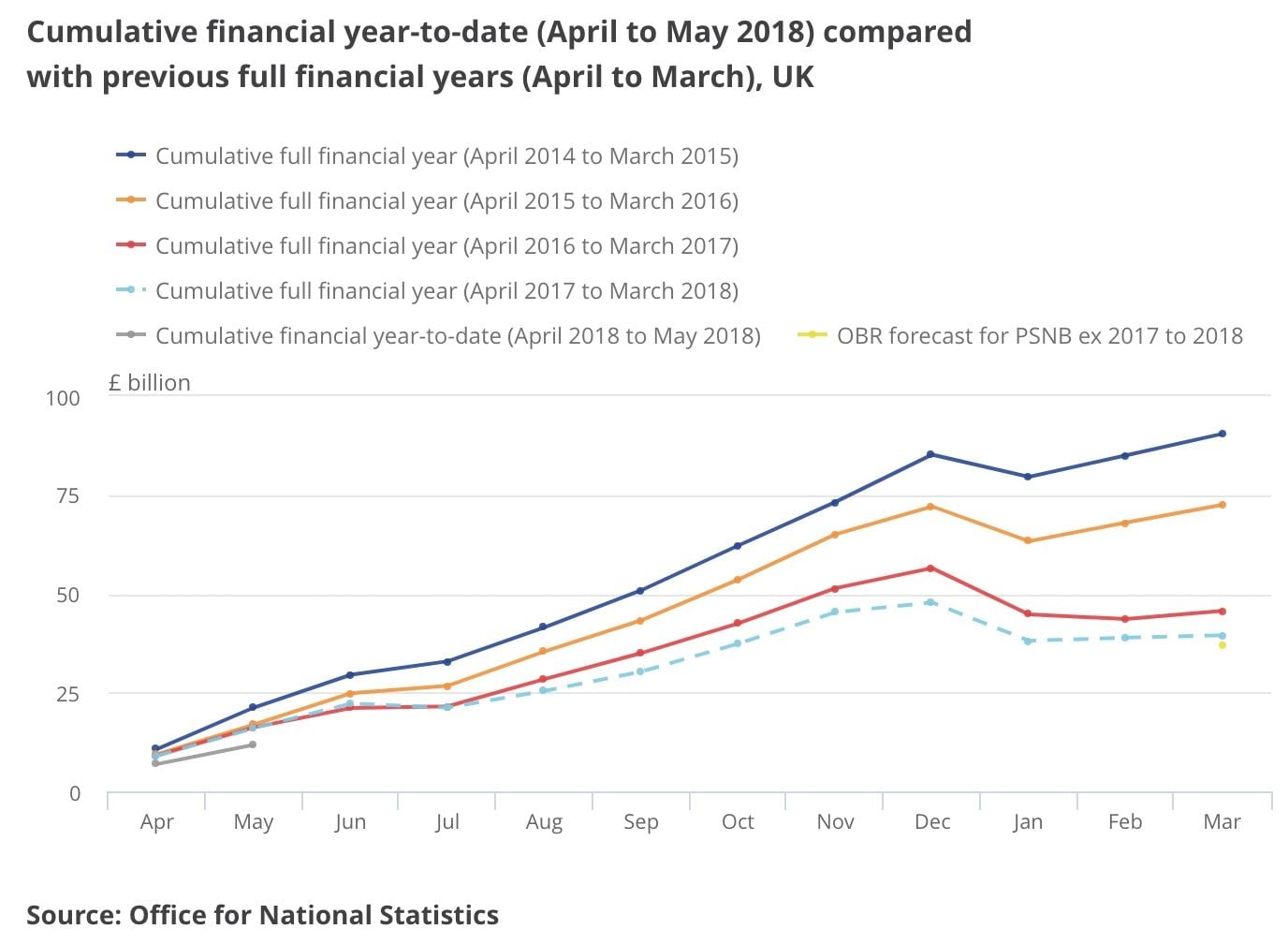

The UK government's estimated public borrowing in 2017/18 has been revised down again to £39.5 billion according to the latest public finance data released by the ONS today.

The figure is £5.7 billion lower than the Office for Budget Responsibility forecast in March.

The first two months of the new financial year have also seen cumulative borrowing down by over £4 billion relative to April and May 2017, with central government receipts up around 3% while central government spending has been broadly flat.

As a share of GDP, public borrowing in 2017/18 is now estimated to be just 1.9%, the first time the budget deficit has been below 2% of GDP since 2001/2.

"The Chancellor faces some tough choices in the November Budget on how to fund the new NHS spending plans, but today's public finance data suggests he is doing so from a stronger fiscal position than might have been expected even a few months ago," says John Hawksworth, chief economist at PwC.

Hawksworth notes that since the OBR estimates that the output gap in 2017/18 was close to zero, the structural budget deficit was probably also just below 2% of GDP in that year, meaning that the Chancellor has already met his medium-term fiscal target set originally for 2020 with further deficit reductions likely over the next couple of years.

Excluding distortions relating to Bank of England transactions, the net public debt to GDP ratio is also now on a clear downward path, falling by around 3% to just over 75% in May 2018.

"So the Chancellor can afford to ease off on austerity without endangering his medium-term fiscal targets," says Hawksworth.

PwC estimate that, of the proposed £25 billion of real NHS spending rises across the UK by 2023/24, around £10 billion is already implicit in current spending plans used in OBR forecasts.

As such, PwC estimate that the Chancellor may only need to raise taxes or increase borrowing relative to previous plans by around £15 billion in 2023/24 to fund these plans, which is equivalent to around 0.6% of GDP in that year.

This week saw Prime Minister Theresa May vow to boost NHS spending by £20BN a year by 2023; a pledge that immediately raised questions as to how such a promise might be funded.

"A net tax rise of around 0.3% of GDP, plus a modest borrowing rise of a similar magnitude would be enough to fund the additional health spending over and above that implicit in current fiscal projections," says Hawksworth.

While the nearer-term developments in UK public finances are constructive, Hawksworth warns it remains much more challenging for the Chancellor to meet his longer term objective of eliminating the budget deficit entirely, but this always looked difficult given the spending pressures of an ageing society and is not, in any event, necessary for long-term fiscal sustainability.

"So long as an economy is growing, it can afford to run a modest budget deficit of around 1-1.5% of GDP while still keeping the debt to GDP ratio on a steady downward path," says Hawksworth.