The tests underline improved financial sector resilience since the dark days of the crisis, but questions over capital requirements remain.

Britain's banks could weather a disorderly departure from the European Union, according the Bank of England, although strategists say the central bank’s plan to review capital requirements in 2018 could hinder the case for further interest rate rises.

All of the UK’s major banks passed the latest round of “stress tests”, which see their balance sheets tested with a hypothetical crisis scenario, according to the Bank of England report.

Included in the stress scenario, which is an extreme hypothetical and horror scenario, was a 2.4% fall in world GDP accompanied by a much sharper, unheard of, 4.7% fall in UK GDP.

The domestic unemployment rate rose to 9.5% under the shock scenario, more than twice its current level, and house prices fell by a staggering 33%.

All of the UK’s systemically important banks subjected to the test emerged at the other end with their capital buffers largely intact, meaning their reserves did not fall below the minimum levels set out in the international “Basel III” rules.

Above: BoE graphs showing details of the stress scenario.

“In the test, banks incur losses of around £50 billion in the first two years of the stress. This scale of loss, relative to their assets, would have wiped out the common equity capital base of the UK banking system ten years ago,” says the Bank of England, in its report.

The successful passing of the tests is something which the BoE says underlines the improved resilience of the financial sector since the dark days of the financial crisis.

"This relatively clean bill of health is particularly significant given that the 2017 stress test scenario provided a harsher set of economic and financial conditions than last year, with some variables falling by more than during the financial crisis," says Paul Hollingsworth, an economist at Capital Economics.

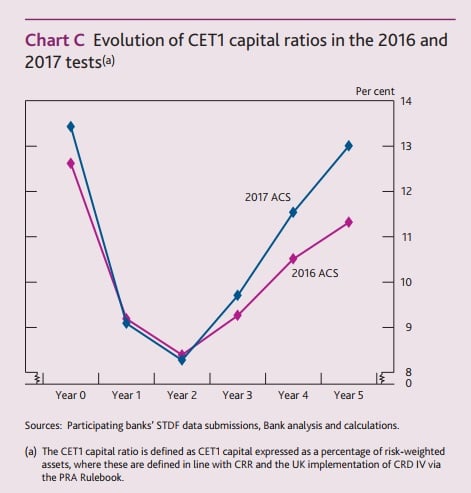

Above: Chart showing 2016/17 improvement in bank CET1 capital buffers.

However, and the rub for markets is, Bank of England policy makers also reiterated plans Tuesday to raise the countercyclical capital buffer from 0.5%of risk-weighted-assets (RWAs) to 1% in November 2018. It is also considering whether to raise the requirement again once into the New Year.

“This buffer is already being increased by 0.5% to 1.0% next November and the BoE seems to be threatening to raise it again depending on the ‘overall risk environment’,” says Chris Turner, head of foreign exchange strategy at ING Group.

The countercyclical buffer is a pile of excess cash that banks keep in reserve in order to support the economy, through lending, in tougher times.

When the going is good, the countercyclical requirement rises, meaning banks have to put aside more cash in time for the bad days.

When the economy hits the rocks, the BoE can cut the countercyclical buffer to zero, like it did in August 2016 following the Brexit referendum.

This frees up up excess cash to fund new lending to households and businesses.

“Tighter regulatory conditions could detract from future tightening prospects and be slightly GBP negative. We’re less bearish on the USD short term, meaning that Cable could correct to 1.3240,” says Turner.

ING’s concern is that an increase in capital requirements could come at a cost to lending to the real economy, which might have a knock-on effect on growth and therefore, the case for interest rate hikes further out into 2018 and beyond.

The banks included in the BoE’s latest stress tests would have to put aside an extra £10 billion in total for every 0.5% increase in the countercyclical buffer, given the banks undergoing the tests had total RWAs of £2 trillion at the end of the third quarter - according to the BoE report.

“The setting of the countercyclical and PRA buffers, as informed by the stress test, will not require banks to strengthen their capital positions,” the BoE says, in its Tuesday presentation. “It will require them to incorporate some of the capital they currently have in excess of their regulatory requirements into their regulatory capital buffers.”

However, a little known piece of information outside of banking sector equity research is that many of the UK’s listed banks have “excess capital”, which is capital over and above the regulatory requirement.

Those banks, such as HSBC and Lloyds, have been using this excess capital to either buy back their own shares, pay dividends or to carry out acquisitions over recent months. Most could probably afford to meet rising capital requirements without compromising lending.

"Given that this has already been signalled, and the strengthening in capital positions that has already taken place, this should not provide a threat to bank lending, or prevent the MPC from tightening monetary policy, over the next few years," says Capital Economics' Hollingsworth.

Get up to 5% more foreign exchange by using a specialist provider by getting closer to the real market rate and avoid the gaping spreads charged by your bank for international payments. Learn more here.