BRC retail sales fell sharply in October while SMMT car sales posted a double digit decline, leaving many eyeing November's budget statement for support.

The Pound strengthened broadly Tuesday after shrugging off a series of data releases that appear to have called into question the wisdom of the Bank of England’s decision to begin withdrawing stimulus from the economy in November.

October’s British Retail Consortium report showed UK consumer spending undergoing its sharpest fall since BRC records began in 2011, with total growth slumping to its lowest since May and now running below the 12 month rolling average.

“The decline was driven by the worst performance of non-food sales since our record began in January 2011, as consumers appear to have opted for outdoor experiences and excursions during half term, over visits to the shops,” says Helen Dickinson, chief executive of the BRC.

Total retail sales grew by just 0.2% on the previous month during October while like-for-like sales slipped 1%, according to the BRC Retail Sales Monitor, which is compiled in partnership with professional services firm KPMG.

“Real consumer spending power has been on a downward trend in the last year as the acceleration in inflation has caused shoppers to become ever more cautious in considering what purchases they can afford,” Dickinson adds.

The Bank of England raised interest rates for the first time in a decade at the beginning of November, adding 25 basis points to the base rate, taking it back up to 0.50%. This reverses the interest rate cut pushed through in August 2016.

“Many now face higher borrowing costs, given the rise in interest rates, which will only serve to heap further pressure onto household finances,” Dickinson says.

The BoE cited a multitude of factors as grounds for its interest rate move although, despite any perceived merits in the rationale, many economists have found the decision to hike incongruous with many of the bank’s statements about Brexit and the outlook for the UK economy.

“Considering the intrinsic link between consumer spending and economic growth, the Chancellor should reflect on this disappointing state of play and deliver a Budget that allays the risks of a further slowdown in consumer spending, by keeping down the cost of living. In other words, a shoppers Budget,” says Dickinson.

BRC Retail Monitor snapshot.

The Chancellor will announce the government’s latest budget on Wednesday, 22 November, which is of even higher importance in light of November's interest rate rise from the BoE.

GDP growth held up better than expected in the third quarter, coming in at +0.4%, up from the anaemic +0.2% seen in the first quarter and the +0.3% seen in the secon quarter.

But given the BoE's recent action and potential Brexit-related headwinds facing the economy, lobby groups have been pushing hard for measures that will make life easier for both consumers as well as retailers - with asks including changes to the personal tax and business rates regimes.

“The survey evidence suggest that retail sales made a weak start to Q4. However, we would caution against putting too much weight on one month of survey data given the surveys’ volatile nature,” says Andrew Wishart, a UK economist at Capital Economics. “And given inflation is close to its peak, and that we expect real wage growth to accelerate somewhat next year, the squeeze on households’ budgets should soon ease.”

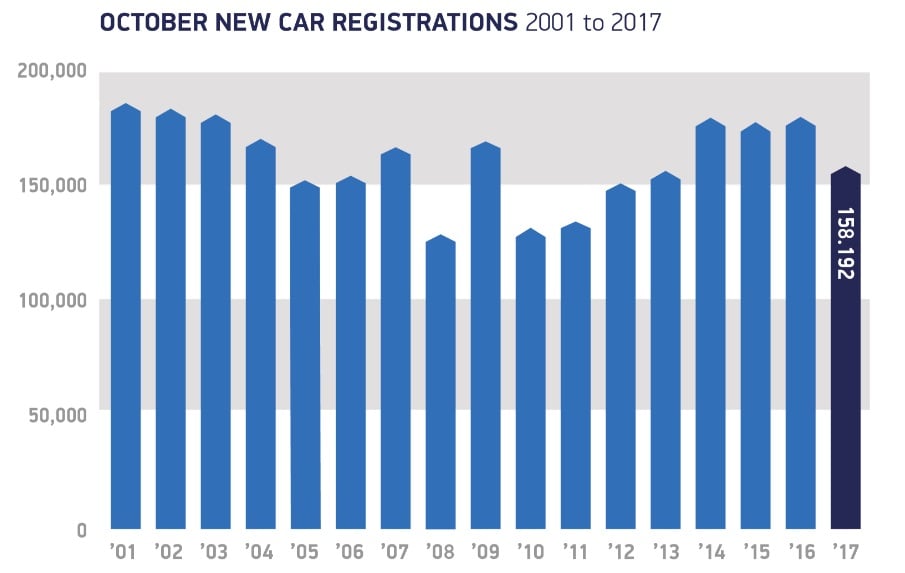

UK Car Sales Fall by Double-digits in October

Tuesday’s BRC report comes ahead of Office for National Statistics retail sales data covering October, which is set for release on Thursday, 16 November.

It also follows October’s monthly survey of the UK car industry, from the Society of Motor Manufacturers & Traders (SMMT), which showed a double-digit decline in UK new-car sales.

“Declining business and consumer confidence is undoubtedly affecting demand in the new car market but this is being compounded by confusion over government policy on diesel,” says Mike Hawes, chief executive of SMMT. “Consumers need urgent reassurance that the latest, low emission diesel cars on sale will not face any bans, charges or other restrictions, anywhere in the UK.”

October's total new-vehicle sales in the UK dating back to 2001. Source: SMMT.

October’s car data marked the second consecutive month of falling car sales in the UK however, it warrants a mention, the decline is believed to have been driven as much by government changes vehicle emissions tax rates as it was any underlying weakness in consumer spending.

“We urge the Government to use the forthcoming Autumn Budget to restore stability to the market, encouraging the purchase of the latest low emission vehicles as fleet renewal is the fastest and most effective way of addressing air quality concerns,” Hawes adds.

The UK government U-turned on its previous support for the adoption of diesel vehicles at the beginning of the current tax year by raising the emissions levy charged on the sale of new diesel cars, adding substantially to the cost of new car purchases.

Diesel car sales rose sharply toward the end of the last tax year as consumers brought forward car purchases to circumvent the tax changes, but since then the fall in demand for diesel vehicles has weighed heavily on total sales.

Registrations of new diesel cars were down 29.9% in October when compared with the same period one year ago while the outlook for broader car sales has now been dampened somewhat by the BoE’s move on interest rates - which is in part aimed at curtailing cheap credit to consumers.

“While expectations for growth next year are weak, the UK’s particularly sluggish supply side points to a further erosion of spare capacity from here,” says Bruce Kasman, chief economist at JPMorgan. “Provided wage growth sustains at least some shift higher, we expect the BoE will hike again next May.”

The Pound was quoted 0.19% lower at 1.3147 against the US Dollar in morning trading Tuesday although the Pound-to-Euro rate was marked 0.19% higher at 1.1366.

Get up to 5% more foreign exchange by using a specialist provider by getting closer to the real market rate and avoid the gaping spreads charged by your bank for international payments. Learn more here.