The GBP continues to be sold across the board as foreign exchange markets remain unconvinced by the improvement witnessed in the UK’s manufacturing sector.

The British pound remains under pressure against its major competitors as the release of Manufacturing PMI data for the month of May fails to excite.

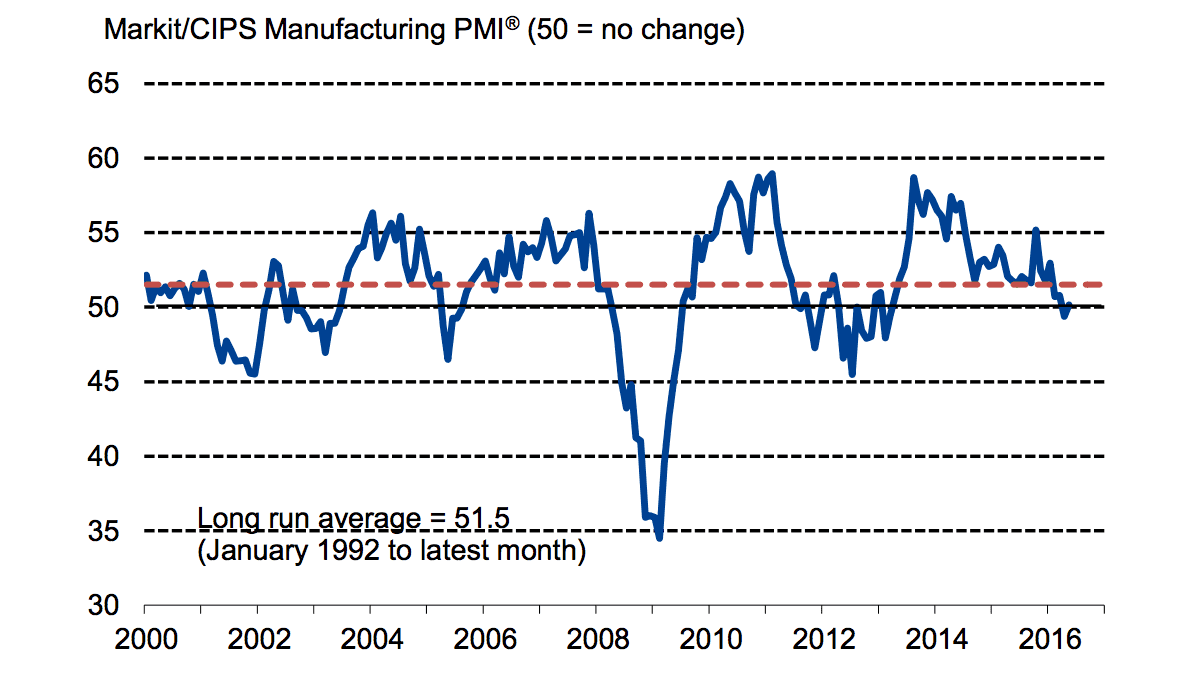

The data should come as a relief - the reading of 50.1 shows that the sector is no longer contracting as has been the case over recent months.

The May release gave a reading of 49.4, this was actually revised higher from an initial 49.2. Consensus forecasts were for a reading of 49.6.

The mild improvement is however not enough to shift the sector back above the long-term average of 51.5.

“As such, it continues to suggest a high hurdle to growth in Q2 in the manufacturing sector, which on official data eked out a 0.3% gain in 2016 Q1, leaving its output 1.5% lower than a year ago,” says a response note to the data issued by Lloyds Commercial Banking.

Of note is that exports remain subdued, suggesting that the 7% decline in the value of the trade weighted pound since November 2015 is not making any notable impact.

One could also argue that the picture would be a lot bleaker were it not for the decline in the pound!

Indeed, this view is shared by Ruth Miller, Economist at Capital Economics who maintains a cheery tone on the sector’s outlook:

“Looking ahead, sterling’s fall since around mid-November should help in time, while we are relatively upbeat about the prospects for the global economy. Accordingly, we still think that things will improve for UK manufacturers later this year.”

Indeed, Miller argues the ongoing weakness in the manufacturing sector is likely to reflect sterling’s previous appreciation and weak overseas demand, she maintains caution against attributing too much of this to uncertainty surrounding the EU referendum.

Manufacturing job losses were registered for the fifth straight month in May. However, the rate of reduction eased to a three-month low and was only modest overall.

Job cuts were focused on the weaker performing investment goods industry. In contrast, new order growth in the consumer and intermediate goods sectors encouraged firms to increase employment.

“The manufacturing sector continued its lacklustre start to 2016. Although key indicators for output, new orders and the headline PMI all ticked higher in May, the latest survey is still consistent with around a 0.8% quarterly decline in the official ONS Manufacturing Production Index. The sector will therefore remain a drag on broader economic growth, adding pressure on the service sector to sustain the upturn in GDP,” says Rob Dobson, Senior Economist at survey compilers Markit.

As the manufacturing sector accounts for only around 10% and therefore Friday’s release of the Services PMI will be keenly anticipated.

“But the modest scale of the recovery in today’s manufacturing PMI still suggests that heightened political uncertainty continues to cast a shadow over UK economic prospects – a pattern that seems likely to be replicated for Friday’s report as well,” warn Lloyds Commercial Banking.